Financial Targets Are Always Moving: Follow Your Own Compass

12:26 AM

To make sure I’m being financially responsible, I always look at the latest economic data to determine whether I’m saving enough, investing enough, and earning enough to take care of my family. I hope you are as well. The last thing you want to do is wake up 10 years from now and realize you didn’t plan properly.

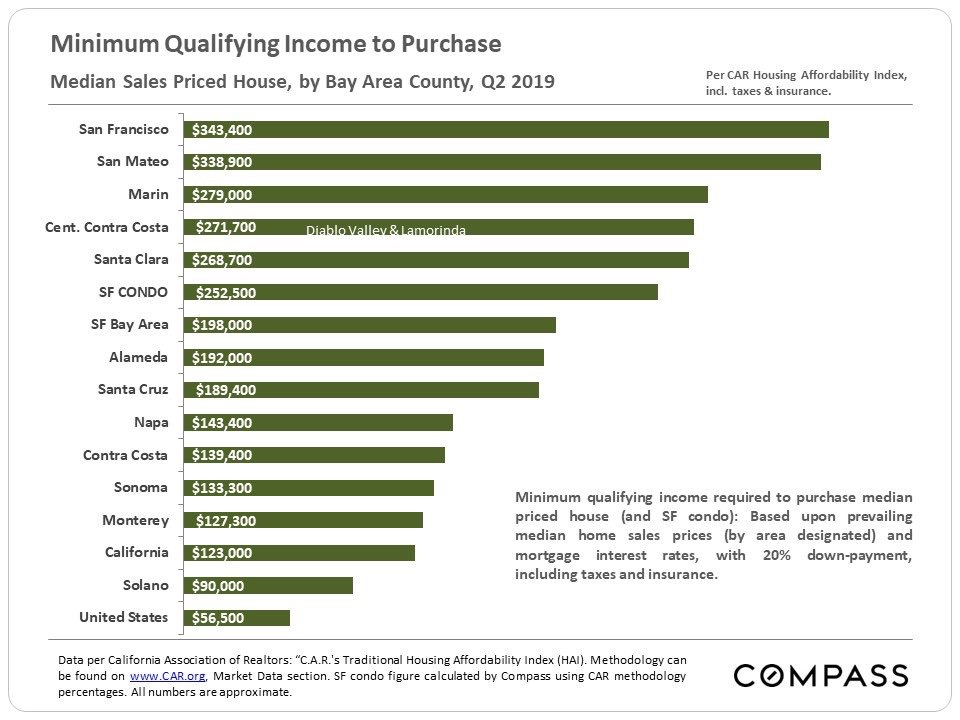

Given housing cost is usually the biggest cost for a family, I’m aways paying attention to the median home price and interest rates.

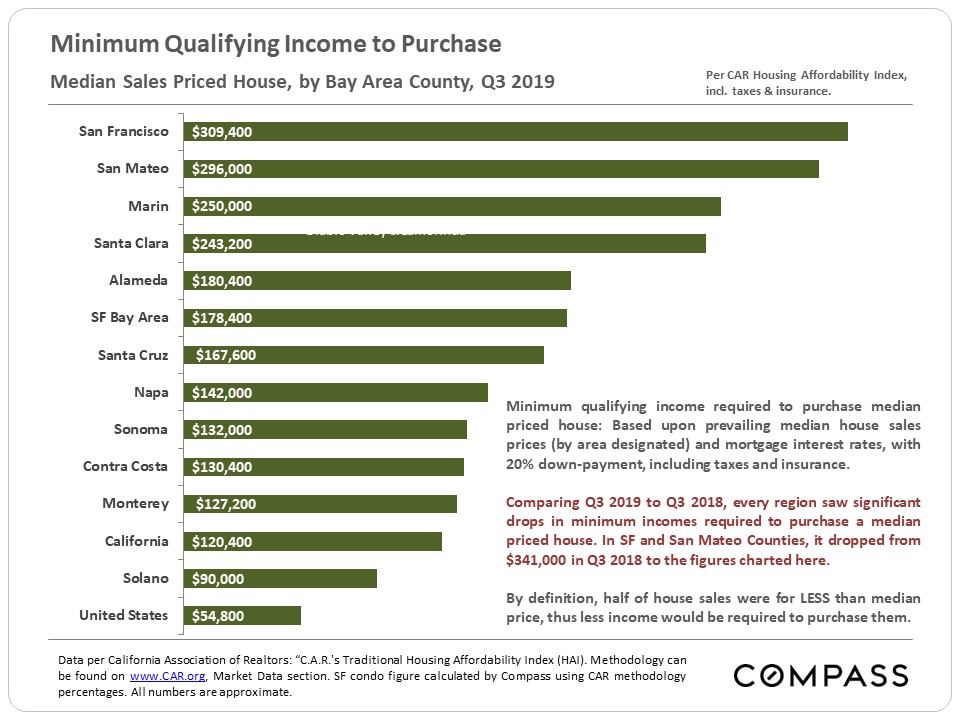

When the Q2 2019 data came out showing that a San Francisco household needs a minimum $343,400 income to buy the median sales priced house, I was floored.

For years, I thought a $250,000 a year household income was enough to live a middle class lifestyle for up to a family of four in San Francisco. After all, I’ve been living in San Francisco since 2001 and intimately know how much I need to lead a comfortable lifestyle through my musings on Financial Samurai.

It disappoints me that after deciding $250,000 was a enough for a family of three to live a happy early retirement lifestyle in 2012, and finally getting there in 2019, Compass Real Estate through data provided by the California Association of Realtors decided to move the goal post!

I was scratching my head at the $343,300 figure because my family lives just fine off less than $200,000 gross a year. It also helps that our investment income is taxed at a more favorable rate than W2 job income.

Instead of complaining, I faced reality that perhaps my income was simply not enough. I got motivated to try and accumulate more money.

Then something funny happened. The numbers changed again.

Financial Targets Are Always Moving

I received a newsletter a couple months later from another real estate agent who had a section on affordability. In my observation, affordability has increased in 2H2019 because mortgage rates have come way down while income and the stock market have gone up.

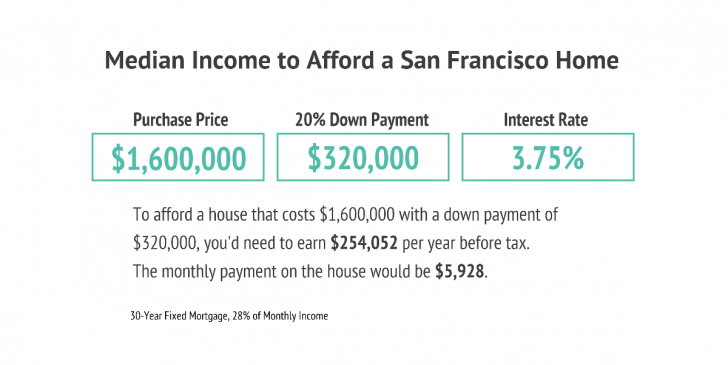

Here’s the graphic that was included in the newsletter.

According to this realtor’s calculations, to afford the median San Francisco home, one must pay $5,928 per month, which shows a $700 fall from the previous month’s median monthly payment.

The newsletter says that instead of needing $343,400 in household income to afford a median-priced home, a household only needs $254,052. Whoo hoo!

$254,052 is $21,171 a month in gross income. The newsletter calculates a home being affordable if the homeowner spends no more than 28% of their monthly gross income on the home, hence $5,928. A 28% limit is a reasonable amount of your gross cash flow to spend on your home.

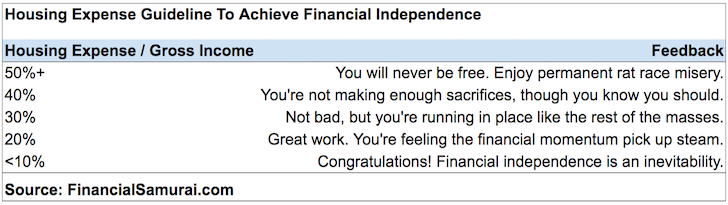

However, if you want to achieve financial independence quicker, I recommend spending no more than 20% of your gross income on your home and ideally just 10% or less.

Here’s the chart from my post, Housing Expense Guideline For Financial Freedom.

Verifying The Large Discrepenacy

There is a huge difference between needing $343,400 to purchase a median-priced home in SF versus $254,052. You need $2.23 million in extra capital generating a 4% rate of return to cover the $89,348 difference.

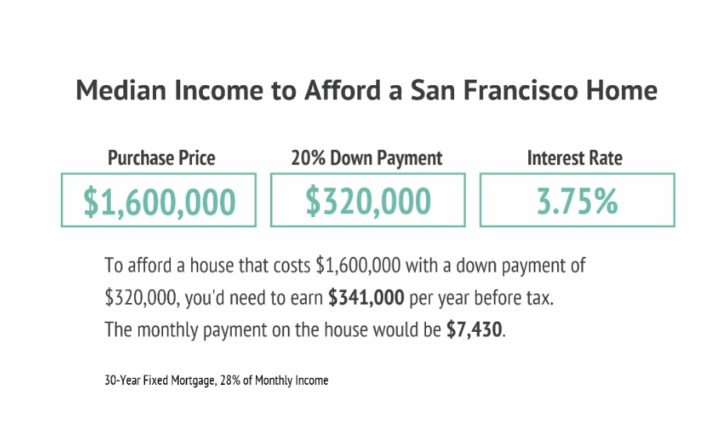

Doing what I always do when something doesn’t look right, I asked the realtor why there was such a huge household income discrepancy compared to the Compass Real Estate group’s numbers taken from the California Association of Realtors.

The realtor got back to me a week later and basically said, “Oops. Our calculations were wrong.”

Here’s the new data he provided. Based on the revised calculations, a household still needs $341,000 in household income to comfortably afford a median-priced home based on $7,430 in monthly payments.

Darn, I wish I wasn’t so thorough.

Don’t Be A Robot

If the real estate brokerage firms were marketing savvy, they’d push for a lower required household income figure to get more people to buy more homes. But clearly they’ve got a muddy message filled with inconsistency.

Only you can decide the household income necessary to live your desired lifestyle. The statistics the government and associations put out there are always moving because they are written by people with different tastes and agendas. Further, the median price of property and interest rates are also always moving too.

Using a 3.75% mortgage rate in the above examples is high when you can now get a 3% mortgage rate or lower. I know because I recently refinanced my primary mortgage at 2.625% for a 7/1 ARM.

At 3%, the monthly mortgage payment declines from $7,430 on a $1,280,000 mortgage to $5,397. Using the same 28% of gross income to spend on a mortgage means you only need a $231,300 annual gross salary to afford the median-priced SF home after putting 20% down.

Major obvious point: Declining interest rates have drastically increased housing affordability.

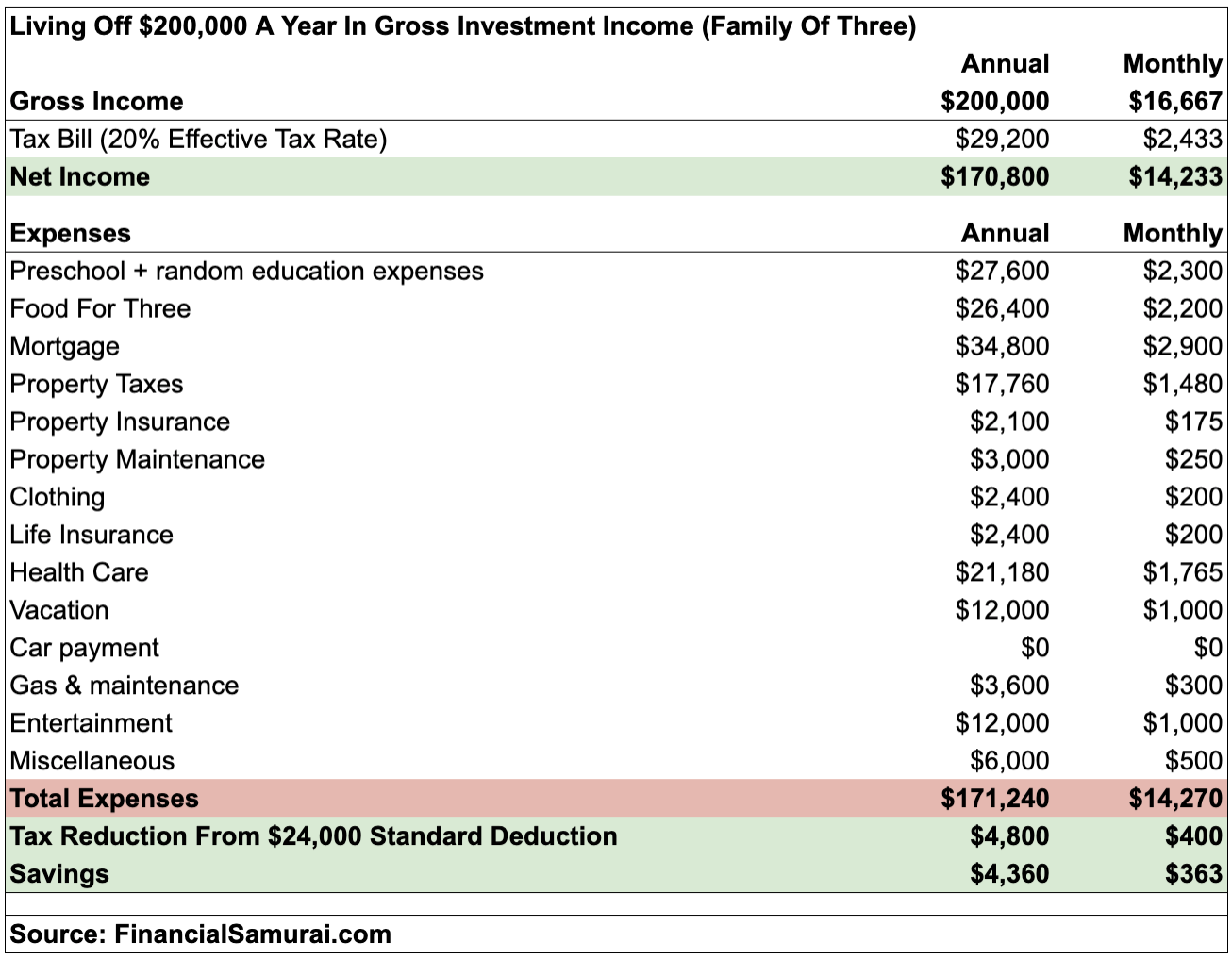

My family is happy living a middle class lifestyle on less than $200,000 a year because that’s what we’ve lived off of for the past three years. I shot for $250,000 in gross passive income given I’ve got to pay taxes.

Here’s a budget for a family of three comfortably living off $200,000 a year in investment income. As you can tell from the budget, it’s a comfortable lifestyle, but nothing extravagant.

If you’re trying to figure out how much money you need to live your ideal lifestyle, pay attention to the economic data on housing, transportation, food, and tuition.

Once you’ve got housing costs down, the other expenses shouldn’t be too much of a problem. Public transportation and ridesharing keeps transportation costs low. Unless you eat like a horse, food costs should be manageable. While nobody needs to send their kid to private grade school.

Crunch The Numbers

For me to generate an extra $100,000 in passive income to live a middle-class life in the Bay Area according to Compass Real Estate Group, I’ve got to come up with another $2,500,000 assuming a 4% rate of return. I’m not sure whether this is worth my time since we’re comfortable living off what we’re generating today.

But something happened again while I was stewing over this post. The Q32019 data came out and the minimum qualifying income to purchase a median-priced property decreased to “only” $309,400 from $343,300 in Q22019. A $33,900 decrease in required income is huge given that is a $845,500 decline in required capital needed at a 4% rate of return.

Finally, the goal post has moved in America’s favor. It used to require a minimum income of $56,500 to buy a median sales priced home in all of America. Now, that figure has dropped to $54,800 while the average income is rising.

Rising affordability is one of the main reasons why I think it’s a good opportunity to buy real estate in 2020+.

Not only should you re-crunch the numbers you see produced by personal finance websites such as mine, economists, realtors, and market pundits, you need to crunch your own numbers.

Don’t let people like me tell you how much you need to be happy. Look at the data with an open mind. Then decide for yourself what’s best.

Readers, have you found yourself trying to catch up to a financial moving target? How do you ensure the data being presented to you is correct? What are some ways in which you decide how much money is enough for you without being delusional?

Related: Latest 401(k) Amounts By Age Versus The Recommended Amounts

The post Financial Targets Are Always Moving: Follow Your Own Compass appeared first on Financial Samurai.

from Financial Samurai

via Finance Xpress

0 comments