As a personal finance expert, I always come across spending statistics that surprise me, make me sad, and some that make me worried.

As a personal finance expert, I always come across spending statistics that surprise me, make me sad, and some that make me worried.

The statistics in this blog post are about people’s average money habits, and they may surprise you. But, I want you to be aware of them so that you can be better than “normal.”

Maybe you will find them so shocking that you will think twice before you buy something, or they may even cause you to drastically change how you spend money.

I do also want to mention that even if you are doing better than the average person, there is always room for improvement.

You should always strive to do your best as sometimes “average” is not good enough for you to live a financially successful life. Keep in mind that the average person is not the greatest with money, and many are wrecked with stress and hardship due to their unfortunate financial situation.

I've talked about shocking money statistics before, which you can find below:

- 14 Shocking Statistics About The Things We Spend Money On

- Are You Better Than Average?

- Money Statistics That May Scare You

Today, I want to show you more because I just find them so interesting!

Below are some statistics on money habits that will hopefully get you into better financial shape.

1. The average American household has $132,529 worth of debt.

The average American household, that doesn’t have a mortgage, is $132,529 in debt. But, if you factor in those with a mortgage, that number goes up to $172,806. This debt includes things such as credit cards, mortgages, auto loans, student loans, medical debt, and more. The average credit card balance alone is $16,061.

And, the average household with a car loan has loans of $28,535.

At first, I thought that perhaps the $132,529 wasn't too bad because I thought most of it had to have been a mortgage, but that is only the amount for those without a mortgage. Plus, if you figure how much of it is because of credit card and car loan debt, that average household debt is pretty scary.

Many people take out a car loan that is half their annual salary or even their full yearly salary, and that can be a huge mistake. Working a whole year for a car is something that most people would regret if they really thought about how much that monthly payment is actually costing them.

2. Average percentage of budget categories.

Have you ever wondered what the average person spends in each category?

- 32.9% goes towards housing.

- 17% goes towards transportation.

- 12.5% goes towards food.

- 11.3% goes towards insurance.

- 7.8% towards healthcare.

- 5.1% on entertainment.

- 3.3% on clothing.

- 3.2% on cash contributions.

- 2.3% on education.

That's a lot going towards housing and transportation each month and each year.

3. 30% of American households have a long-term financial plan.

This one really shocked me, but sadly, I guess I'm not really too surprised. Everyone should have a long-term financial plan, especially if they are not retired or financially independent.

Without goals, it's hard to know what you're working on, which could make it difficult to stay focused.

While How To Reach Your 2018 Goals – Setting Goals for 2018 is about reaching your 2018 goals, it all can also be applied towards reaching your long-term goals. I definitely recommend reading that post and applying it towards your life so that you can reach your financial goals.

4. In 2015, the average American donated $5,491.

Now, that is everyone, so if you are thinking about the amount you donate annually, this may sound skewed. However, the average taxpayer making between $50,000 to $100,000 claimed a charitable deduction of $3,244.

5. You're less likely to budget if you earn less than $75,000 per year.

You're also more likely to coupon if you earn more than $75,000 per year!

There are many reasons for budgeting, yet it seems like the majority of people still do not have one. I believe that if more people started making a budget, they could stop living paycheck to paycheck, increase their savings, reduce and/or eliminate their credit card debt, and more.

Budgets are extremely important, and I believe that nearly everyone should have one. Rich, poor, middle-class, no matter where you are financially, a budget can most likely improve your financial situation.

Budgets are great because they keep you mindful of your income and expenses. With a monthly budget, you will know exactly how much you can spend in a category each month, how much you have to work with, and what spending areas need to be evaluated, among other things.

Related reading: Why You Should Spend Like A Millionaire- The Frugal and Smart Money Habits of Millionaires

6. 44,000,000 Americans have student loans.

That's a lot of student loan debt!

I know it can be difficult, but learning how to pay off student loans can lead to many positives, such as:

- You may finally feel less financial stress.

- You may be able to use that money towards something more important, such as saving for retirement.

- Getting rid of your student loans may allow you to pursue other goals in life, such as traveling more or looking for a better job.

I know these things are true because learning how to pay off my student loans is one of the best decisions that I've ever made.

Related reading: How I Paid Off $40,000 In Student Loans in 7 Months

7. 10,000,000 American households don't have a bank account.

That is a lot of people without a bank account. I'm going to assume that many of these same people also don't invest.

Investing is important because it means you are letting your money work for you. If you weren’t investing, your money would just be sitting there and not earning a thing.

This is important to note because $100 today will not be worth $100 in the future if you just let it sit under a mattress. However, if you invest, then you can actually turn your $100 into something more. When you invest, your money is working for you and hopefully earning you income.

For example: If you put $1,000 into a retirement account that has an annual 8% return, 40 years later that would turn into $21,724. If you started with that same $1,000 and put an extra $1,000 in it for the next 40 years at an annual 8% return, that would then turn into $301,505. If you started with $10,000 and put an extra $10,000 in it for the next 40 years at an annual 8% return, that would then turn into $3,015,055.

8. There are 1.9 billion open credit cards in the U.S.

There are 199.8 million cardholders in the U.S, which means that there are almost 10 credit cards per person. This does include both corporate and personal credit cards, but it still seems like a lot!

9. 20,000,000 Americans own their homes.

Yes, this means 20,000,000 Americans don't owe anything on their homes or have a mortgage.

That is actually pretty amazing, and I'm surprised the number is so high. I hope it continues to increase well into the future.

10. Two out of five Americans have committed financial infidelity.

For every five Americans with combined finances, two of them have, at some point, committed financial infidelity. And, the survey found that financial infidelity has increased in just the past two years.

Whether it’s secret credit card debt, a large secret purchase (such as a house or car even!), or something else, some relationships do experience these problems. I have heard of people finding out that their spouses had hundreds of thousands of dollars worth of debt they didn’t know about, a second house they kept without the spouse knowing, and so on.

The problem with financial infidelity is that it can lead to even bigger financial problems, such as debt piling up beyond what’s imaginable, stress, unhappiness. It has the potential to start impacting other areas in a person’s life (such as work), and it may even lead to divorce.

Related reading: Financial Infidelity And The Problems It Can Create

Sources for these statistics on money habits:

- 10 Incredible Financial Statistics That Sum Up the Average American

- Personal Finance Statistics

- 20 Money Stats That Will Blow You Away

- More Than 20 Million Americans Own Their Homes Outright

- Two in Five Americans Confess to Financial Infidelity Against Their Partner

What statistics above shocked you? How are you doing when compared to the average person?

The post 10 Statistics About The Money Habits Of The Average American appeared first on Making Sense Of Cents.

from Making Sense Of Cents

via Finance Xpress

Posted by: John S Kiernan

Americans are born with an entrepreneurial streak. It’s in our DNA. From Manifest Destiny and the Gold Rush to the Industrial Revolution and the Internet Age, intense periods of innovation have molded our economy and sparked important societal advancements.

Today, more than 15 million people in the U.S., or about 10 percent of the labor force, work for themselves. And there is always room in the market for new ideas, products, services and multi-million-dollar success stories — if one knows where to look.

In order to help aspiring entrepreneurs — from restaurant owners to high-tech movers and shakers — maximize their chances for long-term prosperity, WalletHub’s analysts compared the relative startup opportunities that exist in the 150 most populated U.S. cities. We did so using 18 key metrics, ranging from five-year business-survival rate to office-space affordability. Check out our findings, additional expert commentary and a detailed methodology below.

For a breakdown of smaller markets, check out WalletHub’s Best Small Cities to Start a Business ranking.

Main Findings

Embed on your website<iframe src="//d2e70e9yced57e.cloudfront.net/wallethub/embed/2281/geochart-startbusiness.html" width="556" height="347" frameBorder="0" scrolling="no"></iframe> <div style="width:556px;font-size:12px;color:#888;">Source: <a href="https://ift.tt/2JAKrKw>

Best Places to Start a Business|

Overall Rank |

City |

Total Score |

‘Business Environment’ Rank |

‘Access to Resources’ Rank |

‘Business Costs’ Rank |

|---|---|---|---|---|---|

| 1 | Oklahoma City, OK | 56.85 | 6 | 71 | 21 |

| 2 | Salt Lake City, UT | 55.14 | 101 | 1 | 25 |

| 3 | Charlotte, NC | 54.90 | 14 | 36 | 48 |

| 4 | Tulsa, OK | 54.16 | 53 | 35 | 12 |

| 5 | Grand Rapids, MI | 54.02 | 48 | 55 | 10 |

| 6 | Durham, NC | 53.59 | 69 | 14 | 29 |

| 7 | St. Louis, MO | 53.54 | 68 | 28 | 8 |

| 8 | Austin, TX | 53.37 | 4 | 9 | 127 |

| 9 | Amarillo, TX | 53.31 | 25 | 19 | 82 |

| 10 | Sioux Falls, SD | 52.77 | 50 | 64 | 18 |

| 11 | Springfield, MO | 52.60 | 91 | 63 | 1 |

| 12 | Raleigh, NC | 52.42 | 58 | 16 | 47 |

| 13 | Lubbock, TX | 52.36 | 61 | 5 | 83 |

| 14 | Port St. Lucie, FL | 52.21 | 54 | 26 | 34 |

| 15 | Laredo, TX | 52.11 | 45 | 12 | 74 |

| 16 | Lincoln, NE | 51.95 | 82 | 7 | 58 |

| 17 | Winston-Salem, NC | 51.78 | 76 | 74 | 7 |

| 18 | Houston, TX | 51.76 | 5 | 86 | 102 |

| 19 | Orlando, FL | 51.35 | 46 | 58 | 43 |

| 20 | Fort Worth, TX | 50.87 | 11 | 44 | 116 |

| 21 | Hialeah, FL | 50.67 | 35 | 115 | 37 |

| 22 | San Antonio, TX | 50.58 | 2 | 133 | 96 |

| 23 | Tampa, FL | 50.38 | 55 | 67 | 46 |

| 24 | Fort Lauderdale, FL | 50.31 | 22 | 109 | 76 |

| 25 | Corpus Christi, TX | 50.30 | 15 | 85 | 97 |

| 26 | Birmingham, AL | 50.17 | 138 | 10 | 9 |

| 27 | Boston, MA | 50.05 | 65 | 2 | 128 |

| 28 | Denver, CO | 49.97 | 43 | 32 | 90 |

| 29 | El Paso, TX | 49.86 | 41 | 79 | 77 |

| 30 | Dallas, TX | 49.86 | 21 | 80 | 100 |

| 31 | Rochester, NY | 49.84 | 123 | 33 | 4 |

| 32 | Kansas City, MO | 49.76 | 64 | 111 | 22 |

| 33 | Los Angeles, CA | 49.74 | 9 | 30 | 131 |

| 34 | Buffalo, NY | 49.65 | 106 | 68 | 6 |

| 35 | Miami, FL | 49.42 | 32 | 135 | 64 |

| 36 | Fayetteville, NC | 49.37 | 85 | 114 | 17 |

| 37 | Irving, TX | 49.21 | 12 | 90 | 117 |

| 38 | Atlanta, GA | 49.14 | 90 | 37 | 45 |

| 39 | Aurora, CO | 49.04 | 38 | 113 | 68 |

| 40 | Cape Coral, FL | 49.00 | 40 | 142 | 27 |

| 41 | Shreveport, LA | 48.84 | 94 | 52 | 41 |

| 42 | Jacksonville, FL | 48.84 | 44 | 141 | 42 |

| 43 | Omaha, NE | 48.76 | 75 | 59 | 63 |

| 44 | Oceanside, CA | 48.74 | 3 | 101 | 129 |

| 45 | Fresno, CA | 48.51 | 78 | 53 | 40 |

| 46 | Grand Prairie, TX | 48.38 | 19 | 83 | 120 |

| 47 | Madison, WI | 48.34 | 115 | 4 | 84 |

| 48 | Pembroke Pines, FL | 48.21 | 26 | 102 | 105 |

| 49 | Jackson, MS | 48.21 | 109 | 107 | 5 |

| 50 | Arlington, TX | 48.19 | 24 | 100 | 113 |

| 51 | Reno, NV | 48.18 | 77 | 34 | 79 |

| 52 | Bakersfield, CA | 48.16 | 59 | 31 | 104 |

| 53 | Richmond, VA | 48.00 | 147 | 8 | 13 |

| 54 | Santa Rosa, CA | 47.93 | 42 | 46 | 112 |

| 55 | Worcester, MA | 47.79 | 83 | 29 | 72 |

| 56 | Greensboro, NC | 47.72 | 102 | 104 | 2 |

| 57 | St. Petersburg, FL | 47.71 | 73 | 126 | 39 |

| 58 | Lexington-Fayette, KY | 47.45 | 67 | 39 | 85 |

| 59 | Oakland, CA | 47.34 | 18 | 20 | 140 |

| 60 | Nashville, TN | 47.33 | 93 | 47 | 69 |

| 61 | Columbus, GA | 47.22 | 124 | 96 | 11 |

| 62 | Long Beach, CA | 47.15 | 20 | 84 | 130 |

| 63 | Tallahassee, FL | 47.10 | 140 | 13 | 19 |

| 64 | Brownsville, TX | 47.08 | 104 | 45 | 62 |

| 65 | Chula Vista, CA | 47.06 | 16 | 50 | 137 |

| 66 | Louisville, KY | 46.96 | 100 | 65 | 55 |

| 67 | San Diego, CA | 46.94 | 23 | 25 | 138 |

| 68 | Garland, TX | 46.91 | 29 | 118 | 115 |

| 69 | Stockton, CA | 46.82 | 87 | 66 | 73 |

| 70 | San Jose, CA | 46.68 | 13 | 23 | 143 |

| 71 | Aurora, IL | 46.61 | 62 | 51 | 108 |

| 72 | San Francisco, CA | 46.54 | 8 | 6 | 150 |

| 73 | Knoxville, TN | 46.53 | 141 | 48 | 15 |

| 74 | Colorado Springs, CO | 46.34 | 84 | 128 | 44 |

| 75 | Anchorage, AK | 46.28 | 7 | 94 | 139 |

| 76 | Anaheim, CA | 46.26 | 17 | 95 | 134 |

| 77 | New York, NY | 46.16 | 36 | 41 | 133 |

| 78 | Huntington Beach, CA | 46.13 | 1 | 75 | 144 |

| 79 | New Orleans, LA | 46.12 | 118 | 27 | 60 |

| 80 | Las Vegas, NV | 46.11 | 57 | 119 | 89 |

| 81 | San Bernardino, CA | 46.11 | 79 | 143 | 26 |

| 82 | Henderson, NV | 46.06 | 37 | 123 | 111 |

| 83 | Riverside, CA | 46.04 | 60 | 82 | 94 |

| 84 | Oxnard, CA | 45.86 | 31 | 112 | 122 |

| 85 | North Las Vegas, NV | 45.84 | 51 | 139 | 91 |

| 86 | Minneapolis, MN | 45.82 | 113 | 11 | 98 |

| 87 | Indianapolis, IN | 45.70 | 103 | 116 | 36 |

| 88 | Columbus, OH | 45.69 | 108 | 40 | 75 |

| 89 | Honolulu, HI | 45.66 | 72 | 62 | 114 |

| 90 | Glendale, CA | 45.55 | 30 | 72 | 135 |

| 91 | Baton Rouge, LA | 45.53 | 116 | 49 | 59 |

| 92 | Chattanooga, TN | 45.30 | 139 | 60 | 32 |

| 93 | Tempe, AZ | 45.29 | 110 | 77 | 57 |

| 94 | Virginia Beach, VA | 45.25 | 86 | 121 | 70 |

| 95 | Detroit, MI | 45.21 | 121 | 150 | 3 |

| 96 | Moreno Valley, CA | 45.16 | 74 | 132 | 67 |

| 97 | Norfolk, VA | 45.14 | 117 | 120 | 24 |

| 98 | Modesto, CA | 45.08 | 71 | 127 | 87 |

| 99 | Milwaukee, WI | 45.03 | 127 | 69 | 38 |

| 100 | Santa Ana, CA | 45.00 | 33 | 125 | 125 |

| 101 | Newark, NJ | 44.99 | 81 | 76 | 103 |

| 102 | Boise, ID | 44.94 | 111 | 93 | 52 |

| 103 | Wichita, KS | 44.92 | 122 | 42 | 66 |

| 103 | Irvine, CA | 44.92 | 39 | 3 | 148 |

| 105 | Cincinnati, OH | 44.88 | 126 | 56 | 53 |

| 106 | Mobile, AL | 44.83 | 131 | 131 | 14 |

| 107 | Yonkers, NY | 44.79 | 47 | 110 | 121 |

| 108 | Phoenix, AZ | 44.69 | 88 | 146 | 56 |

| 109 | Garden Grove, CA | 44.68 | 27 | 98 | 136 |

| 110 | Montgomery, AL | 44.46 | 132 | 117 | 20 |

| 111 | Mesa, AZ | 44.43 | 96 | 144 | 50 |

| 112 | Chicago, IL | 44.31 | 107 | 38 | 99 |

| 113 | Plano, TX | 44.27 | 28 | 54 | 142 |

| 114 | Sacramento, CA | 44.23 | 66 | 130 | 101 |

| 115 | Fontana, CA | 44.23 | 49 | 137 | 109 |

| 116 | Scottsdale, AZ | 44.20 | 80 | 70 | 118 |

| 117 | Little Rock, AR | 44.14 | 129 | 21 | 80 |

| 118 | Augusta, GA | 44.12 | 112 | 134 | 16 |

| 119 | Huntsville, AL | 44.10 | 142 | 78 | 33 |

| 120 | Des Moines, IA | 44.05 | 105 | 89 | 81 |

| 121 | Fort Wayne, IN | 43.91 | 137 | 106 | 31 |

| 122 | Overland Park, KS | 43.78 | 95 | 22 | 124 |

| 123 | Baltimore, MD | 43.66 | 114 | 99 | 65 |

| 124 | Memphis, TN | 43.63 | 143 | 108 | 23 |

| 125 | Glendale, AZ | 43.60 | 97 | 149 | 51 |

| 126 | Rancho Cucamonga, CA | 43.38 | 34 | 138 | 132 |

| 127 | Santa Clarita, CA | 43.36 | 10 | 91 | 145 |

| 128 | Newport News, VA | 43.01 | 134 | 140 | 30 |

| 129 | St. Paul, MN | 42.96 | 120 | 61 | 93 |

| 130 | Tucson, AZ | 42.87 | 145 | 103 | 28 |

| 131 | Peoria, AZ | 42.69 | 99 | 129 | 92 |

| 132 | Chandler, AZ | 42.66 | 89 | 124 | 106 |

| 133 | Ontario, CA | 42.39 | 70 | 148 | 95 |

| 134 | Cleveland, OH | 42.28 | 134 | 122 | 49 |

| 135 | Portland, OR | 42.17 | 92 | 88 | 123 |

| 136 | Albuquerque, NM | 41.87 | 144 | 97 | 54 |

| 137 | Jersey City, NJ | 41.55 | 56 | 81 | 141 |

| 138 | Akron, OH | 41.49 | 119 | 147 | 61 |

| 139 | Gilbert, AZ | 41.22 | 98 | 105 | 119 |

| 140 | Toledo, OH | 40.89 | 128 | 145 | 35 |

| 141 | Chesapeake, VA | 40.67 | 136 | 136 | 71 |

| 142 | Spokane, WA | 40.50 | 146 | 57 | 86 |

| 143 | Fremont, CA | 40.31 | 52 | 18 | 149 |

| 144 | Washington, DC | 40.29 | 63 | 17 | 147 |

| 145 | Tacoma, WA | 40.21 | 133 | 87 | 110 |

| 146 | Providence, RI | 40.05 | 150 | 24 | 78 |

| 147 | Pittsburgh, PA | 39.65 | 149 | 43 | 88 |

| 148 | Vancouver, WA | 38.35 | 130 | 92 | 126 |

| 149 | Philadelphia, PA | 37.83 | 148 | 73 | 107 |

| 150 | Seattle, WA | 37.07 | 125 | 15 | 146 |

As current self-employment figures have shown, an increasing number of Americans aim to become more economically self-reliant by working for themselves. To assist them in that goal, WalletHub asked a panel of entrepreneurship experts to share their thoughts on the following key questions:

- What tips would you offer an aspiring entrepreneur?

- Which are some of the biggest mistakes entrepreneurs make?

- Besides technology, what other sector is ripe for disruption by entrepreneurs? What is the next big thing?

- What are the advantages and disadvantages of starting a business in a big city?

- What is the best source of funding for new companies?

- What is the most effective way state and local authorities can stimulate entrepreneurship and new business development?

Colleen S. Merrill Director of the Small Business Development Center and Executive Director of the Alta Resources Center for Entrepreneurship and Innovation at the University Of Wisconsin Oshkosh

Colleen S. Merrill Director of the Small Business Development Center and Executive Director of the Alta Resources Center for Entrepreneurship and Innovation at the University Of Wisconsin Oshkosh Colette Hoption Associate Professor of Management in the Albers School of Business and Economics at Seattle University

Colette Hoption Associate Professor of Management in the Albers School of Business and Economics at Seattle University Rashmi Menon Entrepreneur in Residence and Lecturer in Entrepreneurial Studies and Business Administration in the Ross School of Business at the University of Michigan

Rashmi Menon Entrepreneur in Residence and Lecturer in Entrepreneurial Studies and Business Administration in the Ross School of Business at the University of Michigan Jintong Tang Associate Professor of Management in the Richard A. Chaifetz School of Business at Saint Louis University

Jintong Tang Associate Professor of Management in the Richard A. Chaifetz School of Business at Saint Louis University Timothy Carr Lecturer in Corporate & Entrepreneurial Finance and Real Estate at the University of Wisconsin Whitewater

Timothy Carr Lecturer in Corporate & Entrepreneurial Finance and Real Estate at the University of Wisconsin Whitewater Priya Kannan-Narasimhan Associate Professor of Management in the School of Business at the University of San Diego

Priya Kannan-Narasimhan Associate Professor of Management in the School of Business at the University of San Diego Jim Arkell Assistant Professor of Business Administration at the University of Alaska Fairbanks

Jim Arkell Assistant Professor of Business Administration at the University of Alaska Fairbanks Simon S. Mak Professor of Practice in Entrepreneurship and Associate Director of the Caruth Institute for Entrepreneurship at Southern Methodist University Cox School of Business

Simon S. Mak Professor of Practice in Entrepreneurship and Associate Director of the Caruth Institute for Entrepreneurship at Southern Methodist University Cox School of Business Judi Eyles Director of the Pappajohn Center for Entrepreneurship at Iowa State University

Judi Eyles Director of the Pappajohn Center for Entrepreneurship at Iowa State University

What tips would you offer an aspiring entrepreneur?

- Asses the why? Why are you embarking on this journey? To help others, for profit, to introduce a new concept/product/process or the freedom of business ownership? Many aspiring entrepreneurs have different end games. Do they want to own a company with hundreds of employees or have a quick exit strategy to move on the next big thing? Your end game determines the path you will take.

- How much mental toughness do you have? Entrepreneurs have grit, determination and the ability to move mountains. Are you ready to do whatever it takes for as long as it takes?

- Information -- go to the source. Who is going to use your product/service, what value do they see in what you are offering and how/when will they use it? Information is key to decision-making -- however, there is a point where you need to take action instead of constantly collecting information.

What are some of the biggest mistakes entrepreneurs make?

In my opinion/experience, two things kill new (and existing) businesses: cash flow and management.

Having a sound understanding of your runway and profit margins is key. Pro-forma statements outlining your first-year revenue along with strategic monthly metrics to gauge your performance.

Management -- know what you don't know and seek strong mentors to support you. So many entrepreneurs want to do this all alone and they make costly mistakes that could have been avoided.

Failure to execute. Sometimes you don't have all the information you would like. Many entrepreneurs become paralyzed and miss opportunities by not moving forward.

Besides technology, what other sector is ripe for disruption by entrepreneurs? What is the next big thing?

- Transportation -- in addition to all the technology advancements.

- Renting: Uber is beginning the program of people renting their personal vehicles. This will continue to flow to boats, UTV or just about anything. We have had a team begin to explore how this market will work.

- Movement of goods: so many rails, semis are bid out one way or not at full capacity. We are seeing the beginning of creative product movement through innovative software and personal collaborations.

- Money -- the war on cash and convenience.

- AI -- this is going to change the way we do everything.

- Renewable energy -- I think the millennials and Gen Z are very interested in the environment, quality and social causes.

What are the advantages and disadvantages of starting a business in a big city?

Advantages: information, people, easy-to-run beta test, supply chain and competition to learn from.

Disadvantages: harder to find people to support you, buy local doesn't mean as much as it does in a smaller community, access to capital might be different as local communities are looking to keep home-grown businesses in their back yard.

What is the best source of funding for new companies?

Their customers -- go out there and hustle. If you have customers, it is a heck of a lot easier to find investors.

What is the most effective way state and local authorities can stimulate entrepreneurship and new business development?

- Work with their local SBDC office -- these offices provide no-cost business consulting, run training programs and are highly connected to resources.

- Seed funding -- it doesn't take much to vet out some ideas, but you do need a few dollars in pot. Seed funding, vested interest and community support bring out entrepreneurs.

- In-kind support sometimes is far greater than financial.

- Strong mentorship network that truly has the success of the entrepreneur at heart.

What tips would you offer an aspiring entrepreneur?

I have three main pieces of advice for an aspiring entrepreneur:

- Don't be afraid to ask questions and ask for help;

- Surround yourself with people that you respect and people that you can count on for support;

- Celebrate the small wins.

Much of being entrepreneurial requires us to think on our feet and adapt. So, it's important to remember that you can't know all the answers/all the appropriate moves all the time because some things will take us by surprise. The second piece of advice is to remind aspiring entrepreneurs that their well-being matters. One determinant of their ability to cope with the ups and downs of running a business and managing people is their access to social support networks. Third, I advise aspiring entrepreneurs to track their progress (towards realizing their entrepreneurial vision) by taking the time to acknowledge how even incremental changes/improvements are important milestones.

What are some of the biggest mistakes entrepreneurs make?

Two mistakes that entrepreneurs make is failing to learn from mistakes and not making enough purposeful mistakes. Mistakes are a part of learning. They can keep us humble and grounded. And when used strategically, they can help us avoid common decision-making traps.

Besides technology, what other sector is ripe for disruption by entrepreneurs? What is the next big thing?

Valuing human capital is more important than ever. While a company might be able to outsource their number crunching, they cannot outsource the responsibility of crafting, communicating, and sustaining a vision for an organization, or the duty to promote high-quality relationships among organizational members. Investing in social enterprises that are geared towards retaining and fostering top talent, and supporting bonds within and between communities and other stakeholders should be a priority. I don't know if this is the "next big thing," but I believe it should be. It is (always) fashionable to recognize that there is financial capital to be gained through the unique synergies that employees create at work; they are inimitable and a source of competitive advantage.

Rashmi Menon Entrepreneur in Residence and Lecturer in Entrepreneurial Studies and Business Administration in the Ross School of Business at the University of Michigan

What tips would you offer an aspiring entrepreneur?

Get out and talk to people. Sometimes, entrepreneurs are concerned about discussing their idea with others, as they are afraid their idea may be stolen -- however, if someone who talks to you for 30 minutes could steal and execute your idea better than you, this probably raises some issues about your idea. Others may be afraid to share an idea that isn't fully developed or fear getting negative feedback about it -- however, the earlier you collect feedback, the less expensive it is to make changes or pivot your idea.

Don't ask people if they "like your idea." Start your customer discovery process with very open-ended questions about the pain points and needs of your potential customers -- try to learn more about what solutions they have tried and what works and what doesn't work. This process helps you learn what you don't know and uncover the most important pain points to address, making the sales and marketing process easier when the time comes. Do not ask prospects if they "like" or "would buy" your product -- answers to these questions tend to be much more favorable in a research setting than in a market setting and could set false expectations.

Don't forget the "softer" side of entrepreneurship. Entrepreneurs can become very focused on the strategic and analytic sides of their business, but ultimately, people build products and buy products. Ensure you are working on developing your skills as a manager, hiring a team which complements your strengths, and keeping yourself open to feedback.

What are some of the biggest mistakes entrepreneurs make?

"Build it and they will come" only happens in movies. The biggest surprise for many entrepreneurs is how difficult it is to sell and market your product or service. Many entrepreneurs can successfully develop a concept, build a team, and create a product -- however, they struggle with customer acquisition. While entrepreneurs are passionate about their ideas and believe their products to be indispensable, customers can be reluctant to change or try new products, even when those products may solve a problem better than their current solution. Good customer discovery research can help you ensure that you are solving the most critical problems for customers in a way that is at least ten times better than current alternatives. Starting marketing early and often is also key -- don't wait until your product is built to start marketing.

Besides technology, what other sector is ripe for disruption by entrepreneurs? What is the next big thing?

I believe health care and higher education are both industries which need to change, to make them affordable in the upcoming decades. Health care in particular has a complex value chain, strong government involvement and regulation, and interesting models and alternatives are becoming more available in the market.

What are the advantages and disadvantages of starting a business in a big city?

Advantages:

- Access to talent -- big cities tend to attract the "best and brightest" in a population;

- Existing infrastructure -- office space and supporting businesses (e.g., food service, etc.) are already built out and availability.

Disadvantages:

- Costs -- higher rents, salaries, etc.;

- More competitive labor market -- employees have more choices available.

What is the best source of funding for new companies?

Sadly, very few options exist for early-stage entrepreneurs, and most end up relying on savings, personal/credit card debt, and funds from friends and family. This also tends to deny entrepreneurial opportunities to those who do not have personal connections to funding. The SBA does have an extensive loan program, but these loans (like other bank loans) need to be personally guaranteed in the early stages of a business. Those businesses which can fund through clients -- essentially asking customers to pre-pay for services or products to be delivered later on -- tend to have more options; crowdfunding helps bring this option to more businesses. For equity financing, such as seed or venture funding, businesses have to be in the high-growth category and have to show some progress with product development and market acceptance before funding becomes available.

What is the most effective way state and local authorities can stimulate entrepreneurship and new business development?

Simplify. Make regulations and tax laws easy to follow and consider providing tax breaks and easements to very early-stage companies (e.g., less than one year old).

Support. Enable and encourage funding to startups, especially at the earliest stages when funding options are limited. Tax incentives could be provided for startup investing and governmental funds could be used to support startup capacity building.

Provide infrastructure. Startups rely on an educated workforce, so government funds and programs allocated to building the talent pool help startups grow more quickly. Startups also struggle to provide benefits, such as health insurance -- government programs to support these initiatives allow founders to focus on building their businesses.

Jintong Tang Associate Professor of Management in the Richard A. Chaifetz School of Business at Saint Louis University

What tips would you offer an aspiring entrepreneur?

- Follow your passion;

- Build your networks;

- Take smart actions (e.g., do market and industry research on the feasibility and viability of your business idea; talk to customers/investors/competitors about your business idea).

What are some of the biggest mistakes entrepreneurs make?

- Poor management of the business/people;

- Lack of strategy and strategic leadership;

- Lack of resilience and perseverance.

Besides technology, what other sector is ripe for disruption by entrepreneurs? What is the next big thing?

Service industry, particularly the integration of e-commerce with customized service.

What are the advantages and disadvantages of starting a business in a big city?

- Advantages: bigger markets, more talented labor supply, more funding sources;

- Disadvantages: more intense competition.

What is the best source of funding for new companies?

- Bootstrapping;

- Angel investors;

- Venture capitalist.

What is the most effective way state and local authorities can stimulate entrepreneurship and new business development?

Currently, the majority of incubators/co-working spaces are privately-owned and operated. These incubators play a crucial role in supporting and advocating for entrepreneurial firms. Sponsorship by state and local governments will significantly boost the development and expansion of incubators, which in turn will not only stimulate entrepreneurship, but help decrease failure rate of new firms.

Timothy Carr Lecturer in Corporate & Entrepreneurial Finance and Real Estate at the University of Wisconsin Whitewater

What tips would you offer an aspiring entrepreneur?

- If you believe in your product/service, then don't let anything stand in your way. Keep working towards that goal of making your product or service viable.

- Do a real analysis of the end market for your product/service and be realistic. Then, figure out if there is a big enough market for the time and effort put in to make sense. Part of that analysis is a projection -- put numbers to your idea. Then ask, again, does this make sense long-term? If so, how do we get to long-term without running out of money in the short term. Cash flow is king.

- What "pain point" is your product or service solving? Solving a problem or "pain point" can make a company very successful.

What are some of the biggest mistakes entrepreneurs make?

- Not having enough money to get their product/service to the end. They then have to either give it up or sell most/all of their interest in it to someone else.

- Being conservative with projections.

- Getting too excited about a product/service to the point that you just see stars in the sky -- it has to work, there is no reason it won't.

- Hiring a big name at a big price tag when you don't have the cashflow to support it.

- They don't want to talk to people about their idea because they feel like someone will steal it. You need to talk to people about it to get it off the ground. The work you and your team put in will get it off the ground -- or not.

Besides technology, what other sector is ripe for disruption by entrepreneurs? What is the next big thing?

Auto shops, real estate, doctors' offices. Places we go to a lot, but tend to be very hands-on or relationship-based. Not that the relationships will change, but the companies in those businesses will become a lot more productive through the help of entrepreneurs. I call them "comfort products" -- those products that make our life more comfortable or easier in some way.

What are the advantages and disadvantages of starting a business in a big city?

- The talent pool is deep;

- Some costs are much higher, like rent;

- Resources are deep to help get your company/service off the ground;

- Capital is more prevalent;

- Talent can cost more due to higher demand for their services;

- When you are in a big city, you forget about those that don't live like you -- you overlook many great opportunities geared towards non-city living, and it becomes tough to see why it's a need.

What is the best source of funding for new companies?

Most companies are bootstrapped or started with their own money. Next is family, then friends. Then, look for angel investors, assuming you have no assets to secure for a traditional bank loan. Angel investors are good because they generally invest locally, have expertise in a certain area, have been successful in business, can mentor you, and know other individuals with money to invest -- but be careful: do not judge a book by its cover. A lot of great businesspeople with considerable means do not look like your typical Wall Street person.

What is the most effective way state and local authorities can stimulate entrepreneurship and new business development?

- Public/private partnerships;

- Incubators;

- Put a lot of thought into it. Don't just throw cash at the problem -- it will generally fail. They should pick areas of their state they want to stimulate or where they wish to create new businesses, then decide what type of businesses they focus on and why. Then figure out if that area and those businesses make sense together. If so, they should look to local support through leading businesspeople to help mentor the businesses. They should also offer mentoring through the state and economic/business development centers.

What tips would you offer an aspiring entrepreneur?

- Passion -- be passionate about what you do. Being an entrepreneur is a 24/7 job with lots of unexpected setbacks. It is difficult to persevere when things get tough, unless you are passionate about your idea.

- Test and iterate -- always test your ideas, test your product or service, test your market, and keep iterating.

- Network -- find mentors in the field as early as you can. You will learn a lot from them and they can connect you to the right people who can help you with your business.

- Resources -- plan early on about how to acquire resources. Whether it is financial capital, skills, equipment, software or anything else that you might need, it will usually be more expensive than you predict. It will also take longer than you anticipate. Successful entrepreneurs engage in bootstrapping -- that is, using what is easily and freely available in the ecosystem to create something of value. See what is available in your ecosystem that you can leverage for your business.

What are some of the biggest mistakes entrepreneurs make?

- Not testing the market for the product or service and not iterating enough. Assuming that "If you build it, they will come."

- Ignoring warning signs of founding team conflicts, when key team players do not get along. This could escalate at the most inopportune moments and lead to failure.

- Keeping friends and family in the business, even if they are not contributing adequately.

- Not building adequate infrastructure to scale up quickly when the business ramps up. Even visionaries like Elon Musk face this challenge.

- Not delegating enough and trying to do it all.

Besides technology, what other sector is ripe for disruption by entrepreneurs? What is the next big thing?

The disruption in the technology sector has enabled many industries to leverage this disruption to create more value for customers. These include:

- Infrastructure -- specifically, transportation and energy. Both traditional automotive manufacturers and newer, technology-based companies are in the race to make electric, self-driving vehicles with highest levels of automation. Similarly, renewables are becoming increasingly competitive with fossil fuels due the enthusiasm and success of the key players in this sector.

- Health care -- many startups are coming up with sustainable ideas that focus on making health care accessible to all. Interestingly, some of these startups are based in emerging economies. These startups will eventually compete with U.S.-based companies, thereby spurring a global competition in this sector.

- Education -- the education sector is being disrupted not only in how content is delivered (online versus traditional classroom training) but also in how it is being created. This will likely lead to opportunities for entrepreneurs to come up with new models of learning, which challenge traditional pedagogy offered by institutes of learning.

What are the advantages and disadvantages of starting a business in a big city?

The advantage of starting a business in a big city is the obvious access to resources such as talent pools, venture capitalists and angel investors, entrepreneurship centers, networking opportunities, and universities. The disadvantage is that big cities also attract lots of competition, thereby offering less chances for any single entrepreneur to stand out uniquely. Big cities also have higher costs of living, as well as higher costs of doing business, such as leasing office space for the business, and congestion. Where one should start a business depends on where the majority of their customers are likely to be located, rather than just looking at starting a business in a big city versus a small city or town.

What is the best source of funding for new companies?

It is very hard for entrepreneurs who have new, untested ideas to receive funding for new ventures. If you are in a university, many offer pitch competitions to provide some seed money. Otherwise, the best bets for a new entrepreneur are personal financing, loans, friends and family, bootstrapping, and crowdfunding websites. Once entrepreneurs have some initial proof of concept, the next stage is getting angel investors, venture capitalists, or corporate ventures interested in their ideas.

What is the most effective way state and local authorities can stimulate entrepreneurship and new business development?

- Fostering the creation of incubators and co-working space. Many private industry participants as well as universities are engaged this endeavor. Offering partial grants for creating incubators can be one way to stimulate more activity in an innovation ecosystem.

- A program that offers grants to initiatives that are focused on developing entrepreneurship within universities. The success of Silicon Valley is mostly attributed to the continued involvement of local universities. Universities can serve as a hub for a region's innovation ecosystem. For example, I am leading an interdisciplinary innovation initiative that focuses on providing entrepreneurship training to students from liberal arts and other disciplines, where students typically do not get exposure to entrepreneurship. These students will also have an opportunity to be mentored by industry participants. Many promising entrepreneurial ideas die on the vine because students do not have access to such opportunities. Grants for collaborative programs, such as the one mentioned above, and opportunities for university faculty, staff and administrators to network with the industry to build the local innovation ecosystem will be valuable.

- Encouraging and providing financial support, so local SDBCs work in partnership with universities to generate new businesses. We have recently opened a SBDC at our university (University of San Diego) focusing on innovation and entrepreneurship. I am able to refer my students with creative business ideas to this center for additional assistance, which is well-appreciated by our students.

- State and local authorities might also consider a program that offers full or partial matching for sustainable and promising ideas, to match any initial funding obtained by entrepreneurs from other private or public sources.

What tips would you offer an aspiring entrepreneur?

First, make a careful and calculated decision about what type of business entity to create, don't just assume that you are going to go public and jump right into setting up a C Corp. Also, don't be in a hurry, make a realistic five-year plan allowing for slow, sustained growth. Finally, and most importantly, do not compromise your ethics in the name of profits. Short-term gains due to questionable/unethical practices inevitably result in long-term losses.

What are some of the biggest mistakes entrepreneurs make?

Undercapitalization is probably the biggest mistake that entrepreneurs make. Entrepreneurs tend to be in a hurry and lack the patience necessary to wait until they are adequately capitalized before they go to market. Another mistake that is often made is not understanding the economies of scale. I've seen numerous business plans presenting five-year revenue projections, showing growth that would require scaling at rate that is not accounted for financially and is simply not realistic. A final, more subtle mistake is not understanding the realities of intellectual property law. Entrepreneurs need to have an IP plan and account for the costs associated with patent/trademark applications, renewals and enforcement.

Besides technology, what other sector is ripe for disruption by entrepreneurs?

I think that the insurance industry is ripe for disruption. How we view insurance and what is an insurable interest has so much room for expansion. If the current trend toward deregulation continues, money that is finding its way into finance by way of disruption in mortgages and auto loans could start moving into insurance.

What is the next big thing? I am not sure it is a "next big thing" because it is already here, but advances in AI are going to continue at exponential rates and several "next big things" will be derived from those innovations.

What are the advantages and disadvantages of starting a business in a big city?

The most significant advantage of starting a business in a big city is that the infrastructure and most support services are more advanced and readily available. Another advantage is the built-in workforce and the ability to recruit top talent from college to the "Big City." At the same time, being in the big city can be a disadvantage, as more young people are looking for employment away from the stress of big city life; choosing quality of life over income. Another major disadvantage is that most big cities are expensive; rents, salaries, utilities, taxes, etc. tend to be higher.

What is the best source of funding for new companies?

The best source of funding for new companies is still friends and family. That said, there are so many funding options these days that finding funding, while still challenging, is easier than it has ever been.

What is the most effective way state and local authorities can stimulate entrepreneurship and new business development?

One way to stimulate entrepreneurship and business development is for state and local authorities to build an entrepreneurial ecosystem. One way to jump-start an ecosystem is to provide tax breaks and incentives to lure established businesses to a community. Many argue that giving tax breaks and incentives to large companies is a zero-sum game. However, the benefit to the community is not in the jobs created by the company getting the breaks, but the opportunity that arises from the ecosystem that is created. Governments can be more effective by fostering a relational ecosystem where entrepreneurs can build on interdisciplinary relationships which allows for growth across sectors. Think Silicon Valley in the 80s and Austin, Texas in the 1990s.

Simon S. Mak Professor of Practice in Entrepreneurship and Associate Director of the Caruth Institute for Entrepreneurship at Southern Methodist University Cox School of Business

What tips would you offer an aspiring entrepreneur?

This response is based on "effectuation theory" that I teach:

- Do something that has meaning to you, a personal connection -- this can be something directly personal or from someone else, but you have the ability to be empathetic to the situation and/or pain;

- Do something that you know something about -- it can be how to technically build it, but it can also be how to sell it, or you really understand the market/customer need;

- Do something that your network can help you with -- every entrepreneur needs help to do something, and having a ready network is key;

- Calculate your affordable loss -- how much time and money are you willing to risk to achieve the next major milestone? Most entrepreneurs get into financial trouble personally because they bet too much too early.

What are some of the biggest mistakes entrepreneurs make?

- Not understanding how cash flow works, and that you can actually be very successful in your profits but still run out of cash and be pushed into bankruptcy;

- Not comfortable with "hand-to-hand combat" in entrepreneur-land -- you have no money and no brand, and now you’re trying to build a million-dollar business and it appears everyone is against you, so you need to fight back;

- Not understanding the overall window of opportunity to take the leap into entrepreneur-land -- not only must the person/entrepreneur be ready (window open), but the startup concept has to be the right time, and then access to capital must be available. Any one of these three windows being closed will compromise the startup, but once these three windows are aligned, then the entrepreneur must act with speed and passion, as this window is bound to close.

Besides technology, what other sector is ripe for disruption by entrepreneurs? What is the next big thing?

Any sector that has a lot of intermediaries (middle-men) are ripe for disruption, especially those sectors that are protected by government regulation -- from health care, to banking, to auto dealerships. I'm biased, but blockchain is one of the disruptors. The key is to recognize that the technology behind blockchain is not that radical (and is available under open source) but rather it is the business models that will use this technology that will win the day. It reminds me of my Linux experience -- that's why I am launching a blockchain entrepreneurship class that focuses on business models.

What are the advantages and disadvantages of starting a business in a big city?

Advantages -- infrastructure, educated workforce, supply chain, presence of potential customers (B2B and B2C), access to corporate venture capital.

Disadvantages -- more local support for corporations than for startups, employees have corporate mindset so it is hard to find co-founders, corporate capital only invests in narrow industries, there are more corporate jobs so employees are not open to startups.

What is the best source of funding for new companies?

- The founder's previous company -- if a former employee (with a good track record) can start a company and have it serve the previous employer needs, then this is one of the most successful startup strategies;

- ICO -- even though the laws are still evolving, this is the quickest way to raise lots of money fast;

- Family -- this is the go-to source for startup capital.

What is the most effective way state and local authorities can stimulate entrepreneurship and new business development?

I'm a big fan of public-private partnerships, specifically regarding capital, so I like public funds to support local entrepreneurs, but the investment decision is made by private professionals to minimize the political nature of these funds and to also maximize the success of the startups.

Judi Eyles Director of the Pappajohn Center for Entrepreneurship at Iowa State University

What tips would you offer an aspiring entrepreneur?

My best advice to an aspiring entrepreneur is to seek input from others and listen. Seek the advice of mentors, and process what they are advising, because it is probably based on experience that matters. Seek input from potential customers and listen to what they are telling you about what they want -- make them excited about the product or service you plan to offer them, so they will be lined up and ready to buy. Seek buy-in from your team, because you know you can't do this alone. Utilize all this input to define your competitive advantage, then get passionate about letting others know about your business.

What are some of the biggest mistakes entrepreneurs make?

Entrepreneurs are likely to make many mistakes, but learn from those mistakes to do things better or differently as they pivot or start the next venture. People seem to be at the heart of everything -- the right team can lead a company through even the most challenging of times; the wrong team can destroy a company before it even gets off the ground. Be brave enough to let people who will be toxic to the organization go -- don't wait. Find and recruit people who bring vision, skills, and passion to the business. Recently, I have seen a lot of new entrepreneurs launch on Kickstarter. If they don't raise the money, they give up. A failed Kickstarter campaign does not mean the business is doomed. Find another way to launch.

Besides technology, what other sector is ripe for disruption by entrepreneurs? What is the next big thing?

I work with a number of student entrepreneurs, and I am inspired every day by the students' interest in solving real-world issues. Social entrepreneurship is really big on our campus. With all the negative in the world right now, it's wonderful to know that our young people care about others, about our environment, and are willing to think boldly about creating global and local solutions that are incredibly meaningful.

What are the advantages and disadvantages of starting a business in a big city?

There are mostly advantages to starting a business in a bigger city. Because networks and resources are so important for building a business, there are simply going to be more of those things in a bigger city. Entrepreneurs will be more likely to tap into startup groups, community programs and resources, and find investors and mentors where there are more people. You might think that a disadvantage is that there will be competition, but I'd like to think that competition is good. Having competitors helps build demand for your product or service -- and competitors will keep you innovating to be better.

What is the best source of funding for new companies?

There is no single best source of funding. It depends on your short-term and long-term needs and goals, resources available, and what burden you can and are willing to bear for borrowed or gifted funds. There is no such thing as free money, so choose funding sources wisely. Most entrepreneurs utilize grants, competition winnings, and personal/private money to get started. Debt financing is common for small businesses, and terms are usually reasonable. Giving up equity for investment is something an entrepreneur needs to fully understand before committing too early in the business; however, it is not always a bad thing to bring on equity financing if it makes sense for scaling the business.

What is the most effective way state and local authorities can stimulate entrepreneurship and new business development?

The buzz right now is "building entrepreneurial ecosystems" -- however, there's no mistaking that community support is huge. Funding and incentives are very important, but it's really much more than that. Communities and states that advocate for entrepreneurs and businesses are key in establishing the right culture to foster entrepreneurial development, build and connect people to resources, develop policies that support economic development initiatives, provide mentorship and support, and celebrate and publicize success stories.

Methodology

In order to determine the best cities for launching a business, WalletHub’s analysts compared the 150 most populated U.S. cities across three key dimensions: 1) Business Environment, 2) Access to Resources and 3) Business Costs. Our sample considers only the city proper in each case, excluding cities in the surrounding metro area.

We evaluated the three dimensions using 18 relevant metrics, which are listed below with their corresponding weights. Each metric was graded on a 100-point scale, with a score of 100 representing the most favorable conditions for startups. Data for metrics marked with an asterisk (*) were available at only the state level.

We then calculated the total score for each city based on its weighted average across all metrics and used the resulting scores to construct our final ranking.

Business Environment – Total Points: 50- Length of Average Work Week (in Hours): Full Weight (~7.14 Points)

- Average Growth in Number of Small Businesses: Full Weight (~7.14 Points)

- Startups per Capita: Full Weight (~7.14 Points)

- Average Growth of Business Revenues: Full Weight (~7.14 Points)

- Five-Year Business-Survival Rate*: Full Weight (~7.14 Points)

- Industry Variety: Full Weight (~7.14 Points)

- Entrepreneurship Index*: Full Weight (~7.14 Points)

- Financing Accessibility: Full Weight (~3.57 Points)Note: This metric was calculated as follows: Total Annual Value of Small-Business Loans / Total Number of Small Businesses

- Venture Investment (amount) per Capita: Full Weight (~3.57 Points)

- Prevalence of Investors: Full Weight (~3.57 Points)

- Human-Capital Availability: Full Weight (~3.57 Points)Note: This metric was calculated as follows: Number of Job Openings per Number of Civilians in Labor Force – Unemployment Rate

- Higher-Education Assets: Full Weight (~3.57 Points)Note: This metric measures the average university rank (based on U.S. News & World Report’s Best Colleges Rankings) and number of students enrolled per capita.

- Share of College-Educated Population: Full Weight (~3.57 Points)Note: This metric measures the percentage of the population aged 25 and older holding at least a bachelor’s degree.

- Working-Age Population Growth: Full Weight (~3.57 Points)Note: “Working-Age Population” includes individuals aged 16 to 64.

- Office-Space Affordability: Full Weight (~5.00 Points)Note: This metric measures the per-square-foot cost of commercial office space.

- Labor Costs: Double Weight (~10.00 Points)Note: This metric measures the median annual income of the city.

- Corporate Taxes*: Full Weight (~5.00 Points)

- Cost of Living: Full Weight (~5.00 Points)

Sources: Data used to create this ranking were collected from the U.S. Census Bureau, Bureau of Labor Statistics, Ewing Marion Kauffman Foundation, National Venture Capital Association, Yelp, Indeed.com, U.S. News & World Report, Tax Foundation, AreaVibes, Council for Community and Economic Research, LoopNet and Federal Deposit Insurance Corporation.

from Wallet HubWallet Hub

via Finance Xpress

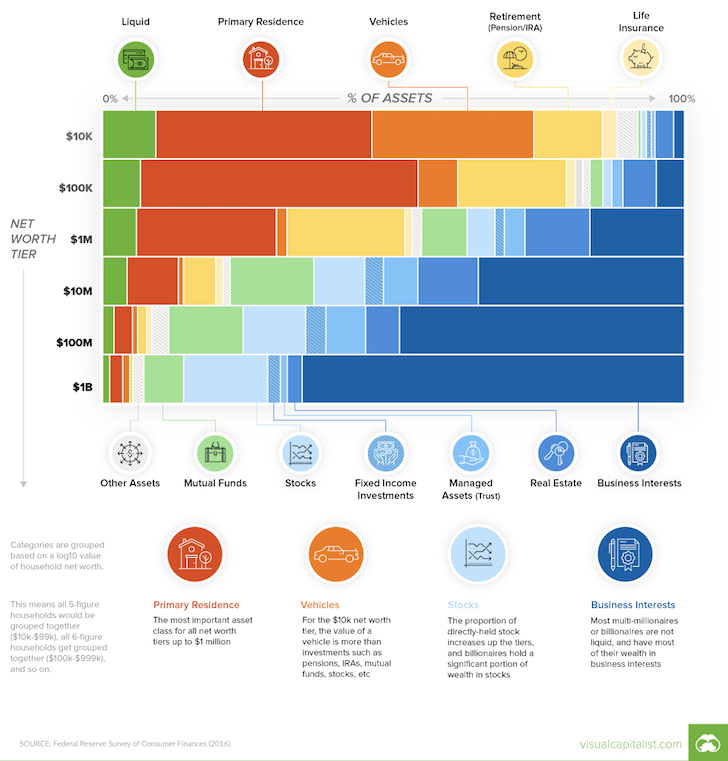

Ever wonder how net worth compositions change the wealthier you get? Look no further as I stumbled across this great chart from VisualCapitalist.com that highlights how much each asset is as a percentage of net worth at various levels. If you want to get rich, it’s good to study how the rich allocate their money.

Notice how red (primary residence) quickly shrinks the wealthier you get while blue (business interests) quickly grows. The key to creating great wealth is to therefore build a business or acquire a significant share of equity in a business.

Net Worth Composition Discussion

Let’s discuss each asset class in a little more detail. I think most Financial Samurai readers or people looking to achieve financial independence are targeting net worth amounts between $500,000 – $10,000,000. Therefore, my commentary is tilted towards this net worth range.

Liquid: As your net worth grows, you don’t need to maintain the same percentage of liquidity to survive through difficult times because the absolute amount of your liquidity increases. The only reason you would need a large percentage of your net worth in liquid assets is if you are highly leveraged. Shoot for 5% – 10% of your net worth in Liquid assets.

Related: The Need For Liquidity Is Overrated

Primary Residence: Notice how there is no asset category for Rent because Rent is a net worth drag. Everybody needs to figure out the right time to own their Primary Residence to at least stay neutral inflation. I’m surprised the Primary Residence category doesn’t take up an even greater percentage of net worth in the $100,000 and $10,000 net worth levels. During the financial crisis, so many Americans got obliterated because their Primary Residence was such a dominant portion of their net worth. I’d get your Primary Residence down to 10% – 30% of your net worth.

Related: Why Real Estate Will Always Be More Desirable Than Stocks

Vehicles: Like Primary Residence, the Vehicle percentage also declines rapidly as one’s net worth grows. Vehicles are the most common net worth killer in my opinion. For some reason, Americans have a love affair with cars and trucks. With the median price of a new car at about $36,000 after tax, the typical American is spending the majority of their ~$59,000 gross household income on a car. Please don’t spend more than 1% – 5% of your net worth or 1/10th of your gross income on a car.

Retirement (Pension/IRA/401k): Only a minority of Americans are now eligible for a pension. But for those who do have a pension, its value is much greater than you might realize. Given the contribution limits to a IRA and 401k, it’s hard for Retirement to grow into a significant portion of one’s net worth.

What’s interesting about the data in the chart is that those with a $1,000,000 net worth have the largest percentage of their net worth in Retirement. Therefore, if you’re amenable to finishing work as a “run of the mill millionaire,” you should strive to max out their pre-tax retirement plans for as long as they work and treat it as bonus money once you are eligible to withdraw funds penalty free.

Related: How Much Should I Have In My 401(k) By Age?

Life Insurance: The fact that Life Insurance is one of the designated asset classes in the chart shows its importance in financial security. Many employees get Life Insurance as a default benefit from work. But often the amount is not enough to fully cover all liabilities. Term Life insurance is cheap before the age of 35 if you are healthy. I highly encourage readers to lock in a long-term policy before a health issue occurs that jacks up your rates.

Related: How Much Life Insurance Do I Really Need?

Mutual Funds: I’m surprised Mutual Funds has the largest weighting for those in the $10,000,000 net worth level. If Mutual Funds are defined as actively run funds with high fees, then digital wealth advisors should channel their efforts towards these high net worth individuals.

Stocks: It’s also interesting to see how Stocks increase as a percentage of net worth the wealthier one gets. Perhaps there’s a higher level of knowledge or conviction as wealth grows. But I suspect the real answer is that wealthier individuals have a greater percentage of net worth in their company stock.

Related: The Benefits Of Stocks Over Real Estate

Fixed Income: Despite the Fixed Income Market being much larger than the Stock Market, it’s surprising to see how little the Fixed Income weighting is across all wealth tiers. One can make the assumption that Fixed Income is an uninspiring tool to stabilize wealth, and can be considered a Liquidity+ investment.

Related: The Case For Bonds: Living For Free And Other Benefits

Managed Assets (Trust): It makes sense that the $10 million and $100 million levels have the highest percentage attributable to Managed Assets. It used to be that you could pass down all your assets estate tax free up to $11 million. But due to tax reform, that number has doubled to $22 million.

Real Estate (rentals/vacation properties): Notice how Real Estate has the largest weighting for those in the $1,000,000 net worth group, but drops off with higher wealth levels. In other words, Real Estate is one of the easiest ways to boost wealth to $1,000,000, but becomes less desirable as time goes on due to maintenance, hassle, and ongoing property taxes. I used to think Real Estate was the best asset class on Earth until I discovered web properties.

Related: A Guide To Buying And Managing Rental Property

Business Interests: Finally, we arrive at the key to building a fortune.

The new CEO of Uber reportedly got a compensation package of around $200 million. He didn’t have to come up with the idea, raise funds, and grind away for years for that type of money. All he has to do is be a good ambassador until he can sell all his stock after the company goes public. The current CEO of Google just sold stock worth $131 million and is getting another $340 million package.

Or, you can go the hard, but extremely satisfying route of creating your own business. The business doesn’t have to be based around a revolutionary new product. Instead, you can simply build a business around a lifestyle like Financial Samurai.

In 2010, I asked myself whether I’d rather own a lifestyle business that one day pumped out $250,000 a year in free cash flow with only 3 hours of work a day and minimal stress or shoot for a 20% chance of getting a $25 million payout by working 14 hour days and experiencing maximum stress for three years. I decided the lifestyle business was the way to go because money doesn’t buy happiness once you make more than $250,000 a year in an expensive ity back then.

When you own a business, not only do you collect its profits, you can also sell the business for a multiple of its profits. This is where the illiquid portion of Business Interests comes in. I’ve been approached a number of times since 2014 to sell, and each time I pass because I want something to do, especially now that I’m a stay at home dad.

Related: Top 10 Reasons For Starting An Online Business

A Different Mindset

I was speaking to a very wealthy entrepreneur the other day, and he said the greatest skill one can have is figuring out a way to hire talented people willing to dedicate their lives to making YOU rich. Of course you will have to properly compensate them, but it is these people who have confidence in themselves, but not enough confidence to make themselves rich through entrepreneurship who you want working for you.

Know your worth. If you are starting to get frustrated with the lack of efficiency at the office or you beginning to tell yourself that you can do it better, then give it a go. Make a better mousetrap.

When I started Financial Samurai in 2009 I found ZERO personal finance blogs written by people who worked in finance. They were all written by people trying to get out of debt or by engineers trying to optimize their content for credit card sign ups. What an opportunity to fill a void!

The people who get really rich are those who ask themselves, “Why not me too?” They believe they deserve to be rich and take action to make it happen.

Related: Sorry Bankers, Techies, And Doctors, You’ll Never Get Rich Working For Someone Else

Readers, how has your net composition changed the wealthier you’ve become? Why don’t more people build a business online given it’s so cheap and easy to start nowadays? Why do some of the most decorated resumes settle for making someone else rich rather than spending all their time making themselves rich?

The post Net Worth Composition By Levels Of Wealth: Build A Business Already appeared first on Financial Samurai.

from Financial Samurai

via Finance Xpress

Posted by: Alina Comoreanu

Traveling abroad can be taxing, especially on our wallets. We spend more than $245 billion on international travel each year. And that works out to roughly $3,390 for each of the 72 million Americans in on the action.

Traveling abroad can be taxing, especially on our wallets. We spend more than $245 billion on international travel each year. And that works out to roughly $3,390 for each of the 72 million Americans in on the action.

Whether you travel by plane, train, bus, car or boat, having the right plastic in your pocket can make life a whole lot easier. The best travel rewards credit cards offer people with good or excellent credit hundreds of dollars in savings per year. And the best international credit cards provide a range of travel benefits. They include insurance for lost luggage, free overnight replacement cards and worldwide acceptance, just to name a few.

To help travelers make the right choice, WalletHub compared 49 of the most popular credit cards on the market in terms of their international-travel friendliness. We used 13 metrics, ranging from the cost of foreign transaction fees to travel insurance coverage and travel notification policies. And that process led to our final rankings of the best and worst credit cards for international travelers. You can find the results below, followed by our full methodology.

Best Credit Cards for International Travel| Rank | Card Name | WalletHub Score |

|---|---|---|

| 1 | Bank of America Premium Rewards | 95.52% |

| 2 | Bank of America Travel Rewards | 91.52% |

| 3 | Barclays Arrival Premier World Elite Mastercard | 88.00% |

| 4 | USAA Visa Signature Cards(e.g., USAA Preferred Cash Rewards Visa Signature) | |

| T-5 | Citi Prestige Card and Citi ThankYou Premier | 85.00% |

| T-7 | Chase Sapphire Preferred and Chase Sapphire Reserve | 80.52% |

| 9 | Capital One Visa Signature Cards | 20.00% |

| T-10 | Capital One Savor Cash Rewards and Capital One Platinum Mastercard Cards(e.g., QuicksilverOne Cash Rewards) | 78.02% |

Barclays, USAA and Capital One are the best credit card companies for international travelers.

4 of the 10 largest issuers do not charge foreign transaction fees on any of their cards.

*U.S. Bank charges 2% of each foreign transaction in U.S. Dollars and 3% of each foreign transaction in a Foreign Currency. **Wells Fargo is not represented in the chart as all their credit cards charge a foreign-transaction fee. Percentages less than 100 imply that only certain cards from the issuer offer the benefit.American Express and Capital One are the only issuers that automatically detect when you travel and do not require a notification.

70% of issuers offer financial assistance for travel emergencies with all of their cards.

*The following issuers are not represented in the chart, as they do not have any cards offering the benefit: Discover and Chase. Percentages less than 100 imply that only certain cards from the issuer offer the benefit.4 of the top 10 issuers will send a free replacement for a lost or stolen card to customers who are traveling abroad.

Replacement Card International Delivery Fees

| Issuer | Expedited International Delivery Fee | Contact Info (international calls) |

|---|---|---|

| Free | 1 -336-393-1111 | |

| $15* | 1-757-677-4701 | |

| $15 | 1-302-255-8888 | |

| Does not ship to international addresses** | 1-804-934–2001 | |

| Free | 1-302-594-8200 | |

| $6 | 1-605-335-2222 | |

| Does not ship to international addresses** | 1-801-902-3100 | |

| Does not ship to international addresses** | 1-503-401-9991 | |

| $14 | Varies by country | |

| $50 | 1-925-825-7600 |

96% of credit cards offer rental car insurance, while 86% offer travel accident insurance and 37% offer a form of luggage insurance.

Detailed Scores| Overall Rank | Card Name | Overall Score | Fees | Secondary Benefits | Convenience Services |

|---|---|---|---|---|---|

| 100% max. | 20% max. | 30% max. | 50% max. | ||

| 1 | Bank of America Premium Rewards | 20.00% | 29.00% | 46.52% | 95.52% |

| 2 | Bank of America Travel Rewards | 20.00% | 25.00% | 46.52% | 91.52% |

| 3 | Barclays Arrival Premier World Elite Mastercard | 20.00% | 24.00% | 44.00% | 88.00% |

| 4 | USAA Visa Signature Cards | 20.00% | 24.00% | 41.52% | 85.52% |

| T - 5 | Citi ThankYou Premier | 20.00% | 30.00% | 35.00% | 85.00% |

| T - 5 | Citi Prestige | 20.00% | 30.00% | 35.00% | 85.00% |

| T - 7 | Chase Sapphire Preferred | 20.00% | 30.00% | 30.52% | 80.52% |

| T - 7 | Chase Sapphire Reserve | 20.00% | 30.00% | 30.52% | 80.52% |

| 9 | Capital One Visa Signature Cards | 20.00% | 25.00% | 33.02% | 78.02% |

| T - 10 | Capital One Platinum Mastercard Cards | 20.00% | 19.00% | 37.50% | 76.50% |

| T - 10 | Savor Cash Rewards | 20.00% | 19.00% | 37.50% | 76.50% |

| 12 | Other USAA American Express Cards | 20.00% | 24.00% | 32.19% | 76.19% |

| 13 | U.S. Bank FlexPerks Travel Rewards | 20.00% | 25.00% | 30.02% | 75.02% |

| 14 | Barclaycard Ring Card | 20.00% | 11.00% | 44.00% | 75.00% |

| T - 15 | American Express Premier Rewards Gold Card | 20.00% | 24.00% | 30.19% | 74.19% |

| T - 15 | American Express Platinum Card | 20.00% | 24.00% | 30.19% | 74.19% |

| 17 | U.S. Bank FlexPerks Gold | 20.00% | 25.00% | 26.69% | 71.69% |

| 18 | USAA Rate Advantage Visa Card | 20.00% | 13.00% | 35.52% | 68.52% |

| 19 | Wells Fargo Visa Signature Cards | 0.00% | 25.00% | 38.52% | 63.52% |

| 20 | Wells Fargo Visa Cards | 0.00% | 19.00% | 38.52% | 57.52% |

| T - 21 | Bank of America Cash Rewards | 0.00% | 9.00% | 47.00% | 56.00% |

| T - 21 | Bank of America Mastercard Cards | 0.00% | 9.00% | 47.00% | 56.00% |

| 23 | Other Citi Cards | 0.00% | 20.00% | 35.00% | 55.00% |

| T - 24 | American Express Green Card | 0.00% | 24.00% | 30.19% | 54.19% |

| T - 24 | American Express Everday Preferred | 0.00% | 24.00% | 30.19% | 54.19% |

| 26 | U.S. Bank Cash+ | 0.00% | 25.00% | 25.02% | 50.02% |

| 27 | Other American Express Cards | 0.00% | 18.00% | 30.19% | 48.19% |

| 29 | All Discover Cards | 20.00% | 0.00% | 24.31% | 44.31% |

| 28 | U.S. Bank FlexPerks Select+ | 0.00% | 19.00% | 26.69% | 45.69% |

| 30 | U.S. Bank Cash 365 | 0.00% | 19.00% | 21.69% | 40.69% |

| T - 31 | Chase Freedom Unlimited | 0.00% | 12.00% | 24.52% | 36.52% |

| T - 31 | Chase Freedom Visa | 0.00% | 12.00% | 24.52% | 36.52% |

| 33 | U.S. Bank Platinum Visa | 0.00% | 11.00% | 25.02% | 36.02% |

| 34 | Chase Slate | 0.00% | 2.00% | 24.52% | 26.52% |

WalletHub analyzed the foreign travel benefits offered by personal credit cards from the top 10 issuers, excluding student and co-branded cards. We collected information from issuer websites for all 49 cards and scored each card’s benefits in three overall categories: Fees (20 %); Secondary Benefits (30 %); Convenience Services (50%). These categories are comprised of 13 individual metrics, described below.

Where policies were incomplete or unclear, we contacted the issuers directly and requested clarification. Four of them – namely, Barclay, Capital One, Chase and Citi - either did not meet our deadline for input or did not provide any feedback.

The scoring framework used to evaluate each card can be found below. Card data is accurate as of April 25, 2018.The maximum score attainable for a card in this report is 100%.

1. No foreign fee (weight: 20%)

- If the card does not charge a foreign transaction fee = 20%

- If the card charges a foreign transaction fee of 0.5% - 1% = 10%

- If the card charges a foreign transaction fee of 1.1% - 2% = 5%

- If the card charges a foreign transaction fee of more than 2% = 0%

2. Secondary Benefits (weight: 30%)a. Travel emergency assistance (weight: 10%)

- If the card offers travel emergency assistance benefit = 10%

- If the card does not offer travel emergency assistance benefit = 0%

b. Travel accident insurance (weight: 8%)

- If the card offers travel accident insurance benefit = 8%

- If the card does not offer travel accident insurance benefit = 0%

c. Lost luggage insurance (weight: 6%)

- If the card offers lost luggage insurance benefit = 6%

- If the card does not offer lost luggage insurance benefit = 0%

d. Delayed luggage insurance (weight: 4%)

- If the card offers delayed luggage insurance benefit = 4%

- If the card does not offer delayed luggage insurance benefit = 0%

Information about what these types of coverage entail can be found in WalletHub’s report on the Credit Cards with the Best Travel Insurance.

e. Rental car insurance (weight: 2%) We identified if the card offers complimentary coverage for rental cars and assigned scores based on its destination coverage as described below:

- If none of the 10 most popular international destinations are excluded from coverage = 2%

- If 2 of the top 10 international destinations are excluded = 1%

- If more than 2 of the top 10 international destinations are excluded = 0%

{kind=link}

Information about what these types of coverage entail can be found in WalletHub’s report on the Rental Car Insurance.

3.Convenience Services (weight: 50%)a. Travel PIN available? (weight: 10%)

- If the issuer automatically provides a PIN with the card = 10%

- If the issuer provides a PIN by request for travel transactions with the card = 8%

- If the issuer does not provide a PIN for travel transactions with the card = 0%