“What are some practical methods startups can use to land those all-important first clients when they don’t have any “case studies” to point prospects to?” One way that startups can land their first clients is for the entrepreneur to use any and all existing business relationships to land new customers. It might be a fellow…

Client Interview is a post from Money Crashers.

from Money Crashers

via Finance Xpress

A Jumbo CD requires a minimum investment of $100,000. In exchange, banks should pay higher interest rates. But do they? Here’s how to find the best Jumbo CD Rates.

Jumbo makes everything better doesn’t it? Jumbo shrimp always taste better than regular shrimp. Jumbo jets took off in the 70’s and exponentially increased the number of annual passengers. The Jumbotron at sporting events allow you to see replays of the game you used to miss. And as luck would have it, Jumbo CD’s can offer you a better interest rate than their regular high-yield counterparts.

A Jumbo CD is just like a regular CD except for the fact that in order to open one, you need at least $100,000. In return for opening this very large CD, banks will typically provide you a better interest rate. You see, when they are able to lock down more of your money for a longer period of time, they can use that money for other things. Lending to small business, investing into other projects–banks can usually get a better return on your money than you can.

Just one problem.

Jumbo CD’s Are Fake News

So now that you know what a Jumbo CD is, you should also know it’s a term that in today’s banking world, almost doesn’t exist. Of all the national banks you’ve come to know and love from reading DoughRoller (Ally, EverBank, Barclays, Synchrony, Marcus, Discover, Chase, Citi. etc), NONE of them offer Jumbo CD’s. CIT happens to be the only bank we’ve written about that offers Jumbo CD rates, and to be quite honest, they’re not all that special.

If you search hard enough online, you will come across a couple of local credit unions that offer strong Jumbo CD rates. M.Y. Safra Bank and Veridian Credit Union can typically match the regular CD’s offered by house hold name brands and they may even beat interest rates by a tick or two. But both banks are restricted to local members and those that open up credit union accounts; so they’re not worthwhile if you live elsewhere.

The Best Jumbo CD Rates

Even though your money won’t work overtime if you deposit $100,000, CD rates today are the strongest they’ve been in a decade. Below you will find the best CD rate for the five most popular lengths. Nine months, one year, two years, three years, and five years. All banks are FDIC insured for $250,000 per depositor so have faith that your money is always protected.

![]() Barclays (Nine Months)–If you can find a nine month CD that offers a little bit more then the best online savings account rates; it’s a good CD. Barclays nine month CD does just that, providing a 1.65% APY for the term.

Barclays (Nine Months)–If you can find a nine month CD that offers a little bit more then the best online savings account rates; it’s a good CD. Barclays nine month CD does just that, providing a 1.65% APY for the term.

To open a Barclays CD, there is no minimum deposit requirement. The CD will auto renew after nine months and you’ll have 14 days to withdraw your funds if you so desire. If you need to withdraw your funds early, the early withdrawal penalty for CD’s up to 24 months is 90 days interest. Considering this is such a short CD length that barely beats out some of the best saving account APY’s; if you’re not 100% certain the money can remain untouched for nine months, consider the 1.50% APY the Barclay’s savings account offers.

- No minimum deposit required

Synchrony Bank (One Year)–This CD is what I consider to be the best CD on the market today. Synchrony is offer a one year CD with an interest rate of 1.95%. You won’t find a one year CD with a better rate and two percent for such a short term is simply fantastic.

Synchrony Bank (One Year)–This CD is what I consider to be the best CD on the market today. Synchrony is offer a one year CD with an interest rate of 1.95%. You won’t find a one year CD with a better rate and two percent for such a short term is simply fantastic.

The only caveat of the Synchrony 12 month CD is that it requires a minimum deposit of $2,000. That’s not nearly the size of a jumbo CD, but it is large enough to scare away a few potential customers. Like Barclays above, the early withdrawal penalty on a one year CD is 90 days simple interest. If one year is too long a term for you, consider the Synchrony savings account which currently offers an APY of 1.45%.

- $2,000 minimum deposit required

EverBank (Two Years)–Working our way up the ladder, EverBank offers a High-Yield Pledge CD for two years at an interest rate of 2.11%. That’s a wee bit better than the 2% on a one year CD above so if you don’t mind locking your money in for twice as long, you can squeeze out a slightly better return with EverBank.

EverBank (Two Years)–Working our way up the ladder, EverBank offers a High-Yield Pledge CD for two years at an interest rate of 2.11%. That’s a wee bit better than the 2% on a one year CD above so if you don’t mind locking your money in for twice as long, you can squeeze out a slightly better return with EverBank.

In order to do so, the minimum deposit to open any High-Yield Pledge CD is $5,000. There are no monthly maintenance fees, no other costs associated. If you have to close the account early an early withdrawal penalty of 25% is applied. That means if you earn $100 in interest; you’ll have to forfeit $25 of it back to EverBank. Also important to note for the high rollers out there, this APY is good for all CD’s up to $1,000,000. If you deposit more than that, check with EverBank to find out what your rate would be.

- $5,000 minimum deposit required

EverBank (Three Years)–EverBank the best again with a three year CD, offering customers a rate of 2.20%. Just like the two year CD above, if you’re willing to lock in your money for an extra 12 months, you can receive an extra small piece of the pie. The same terms apply. Minimum deposit amount is $5,000. Early withdrawal penalty is 25% and this rate is good for balances up to $1,000,000.

Truth be told, if you’re depositing more than the $250,000 FDIC insured amount, you’re taking a risk. While it’s true that your money is still likely protected, should EverBank go under there is no guarantee you’ll recover 100% of your funds. Your best bet would be to break up the CD and either open an account under your spouses and/or children’s names or simply find another bank with a competitive interest rate and park $250,000 in as many different banks as you can.

- $5,000 minimum deposit required

![]() Marcus (by Goldman Sachs) (Five Years)–What a strange name for a bank. Imagine telling people you bank with Jenny or Theodore! Setting aside that oddity the new “Marcus” takes a big swing right away by offering new five year CD members a great 2.50% APY. Also great is that the minimum to open this CD is only $500.

Marcus (by Goldman Sachs) (Five Years)–What a strange name for a bank. Imagine telling people you bank with Jenny or Theodore! Setting aside that oddity the new “Marcus” takes a big swing right away by offering new five year CD members a great 2.50% APY. Also great is that the minimum to open this CD is only $500.

The early withdrawal penalty for closing a five year CD early is 270 days simple interest. That’s actually no too bad so long as you cross the three or four year marker before having to close the CD. With a rate of 2.50%, you’ll still be able to bank a considerable amount of interest, even with the penalty. Marcus also currently offers a very competitive 1.50% APY on their online savings account product. The minimum deposit required to open a savings account is just $1.

- $500 minimum deposit required

It wasn’t too long ago that putting your money into a CD yielded almost the same return as putting it under your mattress. It didn’t matter whether you put $1,000 or $100,000 into a CD, interest rates were under 1% and there weren’t moving. Today however, there’s a real opportunity to park your money into a CD with a very strong APY.

Did we miss something? If you can find a Jumbo CD that competes with the interest rates above, let us know!

Topics: BankingThe post Best Jumbo CD Rates appeared first on The Dough Roller.

via Finance Xpress

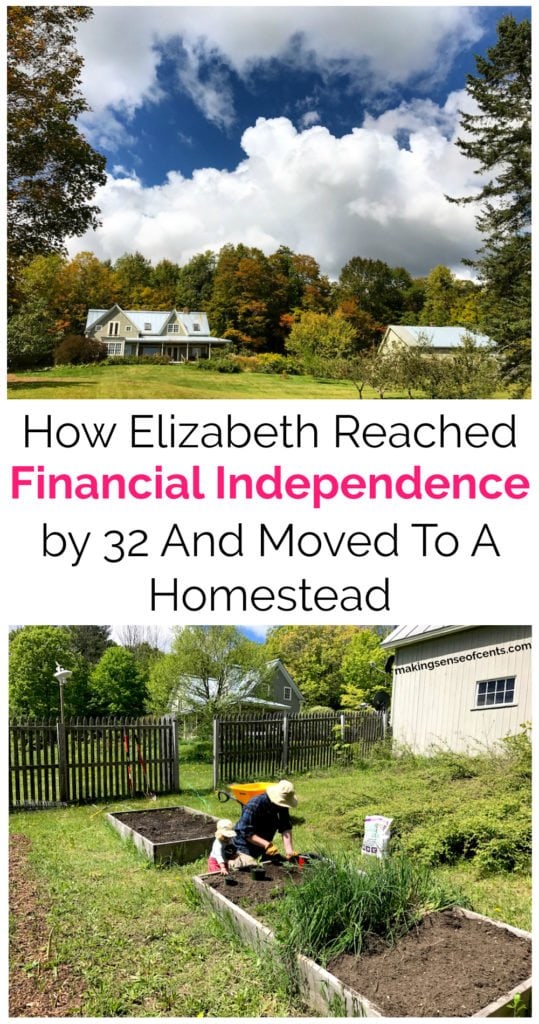

My monthly Extraordinary Lives series is something that I'm really enjoying doing. First up was JP Livingston, who retired with a net worth over $2,000,000 at the age of 28. Today's interview is with Elizabeth, who reached financial independence at the age of 32.

My monthly Extraordinary Lives series is something that I'm really enjoying doing. First up was JP Livingston, who retired with a net worth over $2,000,000 at the age of 28. Today's interview is with Elizabeth, who reached financial independence at the age of 32.

Elizabeth Willard Thames, better known as Mrs. Frugalwoods, is the creator of the award-winning personal finance blog, Frugalwoods.com. At age 32 she “reached financial independence and left a successful career in the city to create a more meaningful, purpose-driven life on a 66-acre homestead in the woods of Vermont” with her husband and young daughter.

Thames is the author of the book, Meet The Frugalwoods: Achieving Financial Independence Through Simple Living. Before becoming a writer and homesteader, she worked for 10 years in the non-profit sector as a fundraiser and communications manager.

In this interview, you'll learn:

- How she reached financial independence.

- The differences between 9-5 and her dream life.

- The sacrifices she made to become financially independent.

- How she saved 70%+ of her income.

- How she still lives quite comfortably despite saving so much money.

- How she plans on making her retirement funds last her whole life.

And more! This interview is jam packed full of great information!

P.S. If you leave a comment below, I'm randomly choosing one lucky reader from the comments to receive a copy of her book.

I asked you, my readers, what questions I should ask her, so below are your questions (and some of mine) about Elizabeth's story and how she has accomplished so much. Make sure you're following me on Facebook so you have the opportunity to submit your own questions for the next interview.

Related content:

- How My Wife and I Paid Off $62,000 in Debt in 7 Months

- How We Paid Off Almost $10,000 in 10 Weeks

- How I Paid Off Over $100,000 in Debt With the Help of eBay and Garage Sales

- How I Paid Off $40,000 In Student Loans in 7 Months

- How This Couple Paid off $204,971.31 in Debt

- How Tina Immigrated To America With Nothing and Now Has a Net Worth of $2,000,000

1) Tell me your story. How did you achieve financial independence?

I'm Liz, although I'm better known as Mrs. Frugalwoods. I write Frugalwoods.com and my first book, Meet The Frugalwoods: Achieving Financial Independence Through Simple Living, will be published by HarperCollins on March 6, 2018.

In May 2016, at age 32, I reached financial independence and left a successful career in the city to create a more meaningful, purpose-driven life on a 66-acre homestead in the woods of Vermont with my husband, Nate, and our young daughter. We're now expecting our second daughter and loving our new life out here in the country! I actually don't refer to myself as “early retired” since I find that to be a bit of a misnomer. Rather, I'm financially independent and don't need to work to earn a living, but choose to work as a writer because I find it personally gratifying. I define financial independence as the point at which our passive assets comfortably cover our expenses and we no longer have to earn paychecks.

In terms of when I began to save money, in truth, I've always been a saver. Throughout childhood, I'd save all of my birthday money and when I began babysitting and earning my own money, I saved up enough to buy my first car by myself at age 16. My husband has a similar relationship with money, and we were able to reinforce this tendency to save in each other. Before enacting our plan to reach financial independence, we were saving around 40%-50% of our take-home pay. After deciding we wanted to retire early, we ramped our savings rate up to over 70%, and sometimes 80%, of our take-home pay.

Our route to financial independence really began during our undergraduate days, which is when we met. Nate and I both attended a relatively inexpensive state school–The University of Kansas–and thanks to scholarships, working during college, and help from our parents, graduated without any debt. After graduating, we were committed to not taking on any debt in our new lives as adults, and we lived frugally from the start. Thanks to this debt-free start in life, we were able to save ever-higher increments of our salaries over the years. And we started very small! My first job out of college was with AmeriCorps in New York City, and I received a stipend of $10,000 for the year. I managed to save $2,000 of it.

From there my salary increased, as did Nate's, and we established a goal of buying a home. With a laser-like focus on saving up a downpayment, we socked away as much as we could every month, even though we both always worked for non-profit/mission-based organizations. Although we also increased our standard of living and experienced lifestyle inflation, we were always focused on saving fairly high percentages of our take-home pay. We didn't always know what we were going to do with this savings–and we certainly didn't have financial independence as a goal initially–but we did know that money provides opportunity. I knew that without debt, and with a substantial savings built up, we'd be able to make unusual choices in our lives and not be beholden to our paychecks forever. I always like to say that no one has ever regretted saving more money. To the contrary, it provides you with options.

Then in March 2014, Nate and I had the startling realization that we were deeply unhappy. We were 29 at the time, living in the Boston area, and both working what we'd assumed would be our “dream jobs”: white-collar, career-track positions we'd worked hard to attain. In 2012, we'd purchased our first home, in Cambridge, MA, and adopted our retired racing greyhound, Gracie. From that point on, we'd thought we had it made and that we'd achieved our long term goals. The problem is that we were both unfulfilled. We realized that working in cubicles under artificial lights all day every week day was a depressing proposition to us both and we couldn't imagine doing it for another 30 or 40 years.

And so, we hatched a plan to radically transform our lives. My husband asked me the simple question: “when are you happiest?” My response: “when we're hiking in the woods together.” His answer was identical and we realized that our lives didn't make sense as we were living them in the middle of urban Cambridge, MA. We made the decision in that moment to reach financial independence and move to a homestead in the woods of Vermont in order to start truly living each day as opposed to wishing time away, working for the weekends.

2) What are the differences between 9-5 and your dream life?

I'm now in control of my time. I'm able to decide what to do and when as opposed to being beholden to an arbitrary nine to five schedule. Additionally, neither my husband nor I have a daily commute, which frees up even more of our time. When we considered how much we were “paying” to work–both financially and with our time–we're grateful every day that we no longer have to trade away our lives for our jobs.

Another major factor in our decision to retire early was our desire to spend as much time as possible with our daughter–who is now two–and her baby sister, who is due in February 2018. Our ability to be stay-at-home parents is transformational for our family and allows us to structure our time, and our daughter's early learning experiences, as we wish. Plus, not having the cost of daycare represents a profound savings in our budget. I consider time and money to be our greatest resources and the two things from which all other priorities stem: family, health, fulfilling work, and more. When I didn't control my time and my money, I felt like I wasn't truly living my life.

3) What sacrifices did you have to make in order to reach this milestone? What did you give up to save 70% of your income?

When Nate and I decided to pursue financial independence, one of our first steps was to comb through every dollar we spent every month. We needed to know where our money was going in order to create a plan to save more of it. Without this crucial base of knowledge, there's no way to set an actionable savings goal.

We decided to eliminate every single expense in our budget that wasn't strictly necessary. Things like restaurant meals, coffees out, new clothes, haircuts–all of it went. In our first month of extreme frugality, we wanted to test ourselves and see just how much we could save. Then, we made conscious and deliberate decisions to add certain expenses back into our budget because we felt they delivered a high return on our investment. For example, my husband and I now go out to dinner together once a month, which is a very special treat for us.

I've found that the rarity of a luxury's occurrence actually serves to increase the level of happiness I derive from it. If we repeatedly expose ourselves to treats, we become deadened to their enjoyment. For example, if we ate dinner out every single night, it would no longer be special and would become a rote chore. By keeping that particular luxury rare, we derive an incredibly high level of satisfaction from our monthly date night out. This is very much in alignment with the concept of hedonic adaptation: repeated exposure to any stimuli or luxury means we'll have to increase the amount or frequency of the luxury/stimuli in order to derive the same level of pleasure. By resetting our hedonic adaptation meters, my husband and I are able to enjoy our lives more while spending less money.

Additionally, we discovered that frugality delivers profound benefits beyond merely saving money. Frugality:

- Is environmentally friendly

- Reduces waste (both food and otherwise)

- Builds community

- Brings you closer to your partner and family

- Helps you identify your priorities and goals

- Gives you options

- Reduces stress by yielding a simpler, more peaceful life

- Saves time!

On that last point, I often hear that people assume a frugal life takes more time, but I find exactly the opposite. Rather, I only do the things I most want to do with both my time and money. I don't let society or other people dictate how I should use those two precious resources, which means I use a lot less of both!

A great example of how frugality saves us time and money are our in-home haircuts. I cut my husband's hair and yes, he cuts mine! I was really nervous before my first home haircut, but was pleasantly surprised at how great it looked. I used to spend $120 per haircut and now, for zero dollars, I have a haircut that looks almost just as good. Plus, I save hours of time! In the past, I had to make an appointment, commute to the salon, get my haircut, and commute back home again. All in all, at least three hours of my time. Now, it takes just 15 minutes! The trade-off for me in a no-brainer.

Additionally, my husband and I have developed our DIY prowess in many different areas: everything from plumbing to cooking to haircuts to working on our homestead. In teaching ourselves how to do all of these tasks on our own, we reduce our dependence on paying people to do things for us, learn new skills, and derive a higher level of satisfaction than if we hired people to do them for us. Researchers have documented this as the “Ikea Effect” whereby people are happier with projects they DIY than with projects they pay others to complete.

Another important thing to remember is that when you eliminate an expense–such as haircuts–you're not just saving that money for one month or one year. You're saving that money every year for the rest of your life. And, if you invest the money you save, which is what I recommend doing, you're then benefiting from compounding returns on that money.

Here's one of my very favorite examples of how eliminating one expense can net you a tremendous amount of money in the long run:

Let’s say you spend $75 every month on cable. Not a huge amount of money on its own. But, multiplied by 12, that’s a whopping $900 per year on television. Let’s say you instead invested that $900 in low-fee index funds, and enjoyed a 7% return (which is considered an average annual market return over the long-term). Imagine you kept that same $900 invested for decades (which is the wisest way to invest) and added $900 to your investments every year instead of paying for cable.

In 30 years, your measly $900 would’ve grown to $91,865.74. This is the compounding power of frugality and investing. If you'd like to try this out with your own numbers, here's the compounding interest calculator I use.

4) Would you say that you live comfortably?

Absolutely! We consider our lifestyle to be luxuriously frugal. We live where we want, as we want, and we use our time as we want. I can't imagine anything more luxurious than that. My husband and I are fortunate to live in a spacious, comfortable home with our children on 66 acres of gorgeous woods, fruit trees, gardens, ponds, creeks, and more. Deprivation isn't part of our equation at all, and we have everything we need. I've found that through living a simple, frugal life, I no longer lust after material goods. I'm not interested in buying new clothes or shoes or purses because I know that those things won't bring me lasting happiness. I'm much more interested in quality experiences and a life that I love living every single day.

I find that the less I buy, the less I perceive I need. The inverse, I think, is also true, such that the more we buy, the more we perceive we need. That's the insidious nature of our consumer culture and the tempting path of treating ourselves everyday with purchases that don't actually get at long term happiness, but that serve to derail our long term goals. By focusing my spending only on my highest and best priorities, I've been able to craft a life that includes everything I need with very little money spent. Frugality mutes the noise of unnecessary consumption and instead focuses us on our true priorities.

5) What career did you have before you retired? Did that career help you to retire earlier?

Prior to achieving financial independence, I worked for ten years as a fundraiser and communications manager for nonprofit organizations. My husband and I both always worked for non-profit/mission-based organizations. Hence, we never made investment banker salaries, but we both did very well. I'm extremely cognizant of the immense role of privilege in my life and in my ability to achieve financial independence at a young age. My husband and I were both tremendously fortunate to be born to families that encouraged us, taught us, and never struggled in a significant way financially. Neither of us comes from wealth–and we certainly didn't inherit any money–but we both come from stable, middle-class families.

I don't think that my success is entirely due to my own good decisions; rather, I see the role of luck and privilege in everything I've achieved. I think it's important for me to acknowledge the many benefits I've enjoyed in my life–from being raised by well-educated parents, to attending quality public schools, to going to college, to securing good jobs. It's a privilege to even consider financial independence and the question of “when are you happiest.” I use this recognition to guide my life and rather than view frugality as a mechanism of deprivation, I see it as the opening to a life filled with abundance and infused with gratitude.

6) What do you have to say to those who may think that they can never earn as much as you can – can they still retire early too?

There are essentially only three factors to achieving financial independence:

- Income

- Expenses

- Time

The more distance you can put between your income and your expenses, the faster you'll reach financial independence. Since my husband and I set an aggressive, fast-paced goal of getting to financial independence in under three years, we needed to save at a very high rate. However, if you're comfortable with a longer time frame, you can save less and earn less. It's all a question of how these three factors relate. It's also true that the less you spend, the less you need to save, the less money you need to live on, and the less money you need overall. Conversely, the more you spend, the more you'll need to save.

I'm an advocate for coming at a goal of financial independence from both the income and the expense angles. If you earn a very high salary, for example, but don't save much, you're no closer to financial independence than someone with a lower salary and low savings rate. So, if you can work to increase income–either by changing jobs or taking on side-hustles–and also reduce your expenses, you'll be able to get at your goal more quickly.

Additionally, it's important to then invest the money you've saved. It's only through solid investments that you'll grow your wealth. It's not enough to just stash your cash in a savings or checking account. I'm an advocate for DIY investing in low-fee index funds and I recommend the brokerages of either Vanguard or Fidelity as they both offer low-fee index funds that you can invest in on your own. My husband and I also own a revenue-generating rental property in Cambridge, MA.

7) What do you do now that you're retired?

Since we live on a 66-acre homestead, my husband and I each split our days between outdoor labor on our land and inside work on projects that we find fulfilling. Living on such a large parcel of land means we're never short on outdoor work that needs to be done. There's planting, tending, harvesting, and preserving vegetables from our garden; pruning our apple and plum trees; making cider from those apples; cultivating garden plots for future planting usage; picking blackberries; maintaining our woods according to our sustainable forestry plan; felling trees for firewood; splitting and stacking firewood; clearing snow in the wintertime… and the list goes on! We don't view the maintenance of our land as “work,” but rather as the joyful pursuit of the life we want to live. We love being outside in nature, and it's a wonderful blessing to have the ability to walk out our front door and hike on any number of trails that we've built through our acres and acres of woods.

We're also stay-at-home parents, so a good deal of our time goes into caring for our two-year-old daughter. Having the ability to structure our days around her schedule makes our lives easier and allows us to spend lots of time doing things together as a family.

In addition to this work on our property, both my husband and I choose to work on other projects that we find fulfilling. I always wanted to be a writer, and it was only through the liberation of frugality that I was able to finally pursue this goal.

8) Do you still earn an income? Does your husband work?

I do! As I mentioned above, I choose to work as a writer because I'm deeply passionate about spreading the message of frugality's transformative power and advancing financial literacy. My husband, for his part, chooses to work from home as a software engineer as he enjoys the intellectual stimulation that stems from this work.

The crucial difference for us is that we don't need to work for money; rather, we choose to work. When you're not required to work in order to earn a paycheck, you can focus your efforts on projects that are meaningful to you and that are in alignment with your values and goals. Having the freedom to only take on projects that I believe in, to fiercely guard my time, and to focus on writing that I think makes a difference is liberating. I love what I do!

9) Can you explain how you will make your retirement funds last your whole life, even though you are only in your 30s?

We plan to keep our expenses in line with a sustainable long term withdrawal from our assets, which will ensure we'll never run out of money. We have a broadly diversified portfolio of assets that we are comfortable drawing from over the long term based on historical modeling.

We have a healthy net income from our rental property, which coupled with a 3.5% or less withdrawal rate from our other assets, would cover our expenses and then some in perpetuity.

10) Lastly, what is your very best tip that you have for someone who wants to reach the same success as you?

I run a free month-long challenge on Frugalwoods, called the Uber Frugal Month Challenge, which is designed to help people follow the path that my husband and I took to achieve financial independence. If you're interested in pursuing a life of joyful (and luxurious) extreme frugality, then I highly recommend you take the Challenge! In brief, the first steps that I recommend–and that the Challenge will guide you through–are as follows:

- Identify your long term goals. Where do you want to be in 10 years? In 20? In 40? What do you hope to do with your life? This is the very first step in identifying what changes you need to make to your finances. Without knowing what you hope to accomplish, any savings or budgeting strategy quickly becomes a pointless slog.

- Track your spending. You must know where your money is going every single month in order to set actionable financial goals.

- Determine how you want to tackle the three elements of the financial independence formula: income, expenses, and time.

Are you interested in reaching financial independence or early retirement? Why or why not?

The post How Elizabeth Reached Financial Independence by 32 And Moved To A Homestead appeared first on Making Sense Of Cents.

from Making Sense Of Cents

via Finance Xpress

A while back, my wife and I spent a couple years in Michigan’s Upper Peninsula, a beautiful but isolated swathe of dense forest, rocky hills, and inland lakes stretching along Lake Superior’s south shore. We were based in a sizable town, but my wife occasionally traveled to a tiny, half-abandoned mining hamlet on the Keweenaw…

Raising Rabbits for Meat – Cost, Legalities & How to Start Farming is a post from Money Crashers.

from Money Crashers

via Finance Xpress

If you’re looking for cheap auto insurance that’s easy to manage on the go, Esurance might be the insurance provider for you. Many insurance companies are still catching up on the technology game. Sure, most of the big names offer websites and apps. But they’re not all created equal.

Esurance was one of the first direct-to-consumer online auto insurance companies, so they stand out on the tech front. But how else does Esurance stack up to the competition? Check out our in-depth review to find out.

History of Esurance

Esurance is an offshoot of Allstate Insurance Company, which is one of the more well-known names in the insurance world. It was one of the very first companies to start selling car insurance to consumers directly online. And that history of online interactions means it still stands out from a technology perspective.

Currently, Esurance offers car insurance policies in 43 states. Yet it has only 17 offices around the country. That’s because customers are meant to have easy online and over-the-phone interactions for buying car insurance, paying their insurance, settling claims, and anything else they need to do. Right now, Esurance insures about 5.2 million vehicles in the U.S.

What They Have to Offer

As we noted above, Esurance is best known for its stand-out mobile and online tools. For instance, you can use the mobile app to put in a claim with a photo of the damage. You can get an estimate almost immediately, and you can often get paid in just one day. You can also get on a video chat with an appraiser, who may be able to approve your payment right then.

If you have a car in the middle of being repaired, you can use RepairView on the app to get updates on your car’s status. Or you can use the app’s What If calculator to see how certain events might raise or lower your rate.

Besides these technical perks, Esurance is known for just having an intuitive interface and an easy-to-operate app. This appeals to those among us, including yours truly, who prefer to handle everything via web rather than over the phone or in person.

Of course, Esurance also offers a variety of insurance products, which are highly customizable. Their CoverageMyWay program lets you personalize your coverage options. Besides the standard liability, comprehensive, and collision service, Esurance offers add-ons like:

- Loan/lease gap coverage

- Emergency roadside assistance coverage

- Rental car coverage

- Uninsured/underinsured motorist liability coverage

- Medical payments coverage

- Personal injury protection coverage

- Custom equipment coverage

- Pay Per Mile insurance (but only for Oregon residents)

Overall, you can probably find the policy you need with Esurance if you’re like most vehicle owners.

Pros and Cons of Esurance

We’ve already discussed a few of the good things about Esurance, chief among them its technology. But here are a few other good points to consider, as well as some potential drawbacks.

Pros

- They offer excellent technology, including great mobile tools that make filing claims quick and easy.

- They offer a variety of discounts, including multi-policy discounts, emergency roadside assistance discounts, online shopper discounts, and claim-free discounts.

- The company generally has good ratings from J.D. Power and Company. They perform especially well in the Pricing and Call Center Representative categories in the 2017 Insurance Shopping Study.

- They’re backed by Allstate, which has excellent financial ratings and overall stability.

Cons

- Esurance gets only mediocre reviews for the claims and payout process on J.D. Power’s 2017 U.S. Auto Claims Satisfaction Study. It scored especially low on the repair process.

- Their prices may be higher than some other budget insurers, such as Progressive and GEICO.

The Dollars and Cents

When we review insurance, we like to include quotes, since price is close to the top of the list of important things people look for when buying car insurance. But keep in mind that your quote can vary considerably. You could pay a lot more or less for insurance, depending on your particular situation, including your state, driving history, and the car you’re insuring.

But, nonetheless, we will walk through the quote process here so you can get an idea of pricing with Esurance. For these purposes, we’ll work with information close to my own. We’ll get pricing for a married female car owner who drives a 2009 Saturn Vue and lives in Indiana.

Here’s what the quote engine came up with:

That seems like a great quote, at first. The quote, however, is only for 50/100/50 liability insurance coverage with no comprehensive or collision coverage. I added those, each with a $500 deductible. Then I decided to add some of the extra features, including roadside service and rental car coverage.

With these additional coverages, the monthly cost jumped up to $77.35, or $455 for six months. That could be quite a bit higher than what you’d find with other companies.

Also, I was surprised during the quoting process that the quote engine didn’t work smoothly at this point. I had to reload it a few times to get it to spit out the new quote once I changed the parameters. That doesn’t bode well for an insurance company whose primary draw is its technology!

Who Is It Best For?

Depending on your current insurance situation, Esurance could be cheaper than what you have now. But you’ll definitely want to get a quote, since it doesn’t consistently rank well for low premiums. But if you’re looking for flexible insurance policies backed by a highly-rated company, Esurance could work for you. This is especially true if you live in Oregon and don’t drive much. In this case, check out the Pay Per Mile insurance, which could save you a bundle.

Topics: Auto InsuranceThe post Esurance Auto Insurance Review appeared first on The Dough Roller.

via Finance Xpress

Posted by: John S Kiernan

Depending on where you live, property taxes can be a small inconvenience or a major burden. The average American household spends $2,197 on property taxes for their homes each year, according to the U.S. Census Bureau, and residents of the 27 states with vehicle property taxes shell out another $436. Considering these figures and the rising amount of debt in America, it should come as no surprise that more than $14 billion in property taxes go unpaid each year, the National Tax Lien Association has found.

And though property taxes might appear to be a non-issue for the 37 percent of renter households, that couldn’t be further from the truth. We all pay property taxes, whether directly or indirectly, as they impact the rent we pay as well as the finances of state and local governments.

But which states have the largest property tax load, and what should residents keep in mind when it comes to meeting and minimizing their tax obligations? In search of answers, we analyzed the 50 states and the District of Columbia in terms of real-estate and vehicle property taxes. We also asked a panel of property-tax experts for practical and political insight. Read on for our findings and a full description of our methodology.

Real-Estate Tax RankingEmbed on your website<iframe src="//d2e70e9yced57e.cloudfront.net/wallethub/embed/11585/property-geochart1.html" width="556" height="347" frameBorder="0" scrolling="no"></iframe> <div style="width:556px;font-size:12px;color:#888;">Source: <a href="http://ift.tt/2ovKWNC>

Real-Estate Property Taxes by State|

Rank |

State |

Effective Real-Estate Tax Rate |

Annual Taxes on $179K Home* |

State Median Home Value |

Annual Taxes on Home Priced at State Median Value |

|---|---|---|---|---|---|

| 50 | Illinois | 2.30% | $4,105 | $173,800 | $3,995 |

| 51 | New Jersey | 2.35% | $4,189 | $315,900 | $7,410 |

*$178,600 is the median home value in the U.S. as of 2015, the year of the most recent available data.

Changes to Real Estate Tax Rates Over Time

Embed on your website<a href="http://ift.tt/1Tc9EwD"> <img src="//d2e70e9yced57e.cloudfront.net/wallethub/posts/33027/rankings-2010-2015-real-estate-tax_-states.gif" width="" height="" alt="Rankings-2010---2015-Real-Estate-Tax_-States" /> </a> <div style="width:px;font-size:12px;color:#888;">Source: <a href="http://ift.tt/2ovKWNC>

Red vs. Blue States

Vehicle Property Tax Ranking

Embed on your website<iframe src="//d2e70e9yced57e.cloudfront.net/wallethub/embed/11585/property-geochart2.html" width="556" height="347" frameBorder="0" scrolling="no"></iframe> <div style="width:556px;font-size:12px;color:#888;">Source: <a href="http://ift.tt/2ovKWNC>

Vehicle Property Taxes by State|

Rank |

State |

Effective Vehicle Tax Rate |

Annual Taxes on $23K Car* |

|---|---|---|---|

| 50 | Virginia | 4.19% | $966 |

| 51 | Rhode Island | 4.77% | $1,100 |

*$23,070 is the value of a 2016 Toyota Camry LE four-door sedan, the highest-selling car of 2016.

Ask the ExpertsProperty taxes are an extremely important issue since they impact all of our lives. But how should we incorporate them into our financial decision making? And how should policy makers across the U.S. approach them as well? For answers to those questions and more, we consulted a panel of tax and public-policy experts. You can check out their bios and responses to key questions below.

- Do people consider property taxes when deciding where to move? Should they?

- Should nonprofits pay property taxes?

- Should local tax policy be adjusted to rely more or less on property taxes versus other forms of taxation?

- Should more types of property be subject to property taxes? If yes, what types?

- Should certain groups of people be exempt from property taxes or be taxed at a lower rate?

Mark Andrews Chairman and President of KE Andrews & Company

Mark Andrews Chairman and President of KE Andrews & Company Stephen J. Lusch Assistant Professor of Accounting in the Neeley School of Business at Texas Christian University

Stephen J. Lusch Assistant Professor of Accounting in the Neeley School of Business at Texas Christian University Deborah Meyer CEO & CCO of WorthyNest

Deborah Meyer CEO & CCO of WorthyNest Tiffany B. Ballard Wealth Manager at Bergland Wealth Management

Tiffany B. Ballard Wealth Manager at Bergland Wealth Management Todd Minear Financial Advisor and President of Open Road Wealth Management

Todd Minear Financial Advisor and President of Open Road Wealth Management Kathleen Longo President & Founder of Flourish Wealth Management

Kathleen Longo President & Founder of Flourish Wealth Management Kenneth J. Eaton Managing Principal of Stepp & Rothwell

Kenneth J. Eaton Managing Principal of Stepp & Rothwell Jon Ripans Property Tax Attorney, Commercial Real Estate Appraiser, Arbitrator and General Mediator at Valuation Matters LLC and The Ripans Law Firm LLC & Property Tax Affiliate Member of the Institute for Professionals in Taxation

Jon Ripans Property Tax Attorney, Commercial Real Estate Appraiser, Arbitrator and General Mediator at Valuation Matters LLC and The Ripans Law Firm LLC & Property Tax Affiliate Member of the Institute for Professionals in Taxation Tod Buckvar Vice President at Buck Realty

Tod Buckvar Vice President at Buck Realty Joe Pitzl Managing Partner at Pitzl Financial

Joe Pitzl Managing Partner at Pitzl Financial

Do people consider property taxes when deciding where to move? Should they?

Yes, and yes

Should nonprofits pay property taxes?

No.

Should local tax policy be adjusted to rely more or less on property taxes versus other forms of taxation?

No -- any additional types of taxation would provide the opportunity or vehicle to increase taxes.

Should certain groups of people be exempt from property taxes or be taxed at a lower rate?

Yes, servicemen and women should receive certain benefits based on their service. In Texas, handicapped and 65-and-older homeowners are capped, which is good. The problem with these types of opportunities is the potential for abuse and lack of oversight.

Stephen J. Lusch Assistant Professor of Accounting in the Neeley School of Business at Texas Christian University

Do people consider property taxes when deciding where to move? Should they?

Tax is one of many variables that people consider when deciding where to move; however, it is seldom a first-order determinant. Generally, I would expect that individuals consider factors such as job opportunities, crime rates, schools, and commute times, before they typically consider property taxation in their moving decisions. In states where property taxes are high, such as my home state of Texas, the location of your property can make a big difference though. There are areas of the Dallas/Fort Worth metroplex where if you purchase a house a block or two over, you may pay a few thousand dollars less in property taxes per year, because the property falls into a different county/city/school district, etc.

Overall, taxes, including property taxes, are real cost of location decisions, and thus should be considered in these decisions. However, the goal is to maximize the net benefits. There are benefits of certain areas, and costs of certain areas. One such cost is tax, but that needs to be considered as part of the larger puzzle. In most instances, selecting location purely based on tax will very likely not result in the optimal decision.

Should nonprofits pay property taxes?

This is a question that has valid arguments on both sides. First, the general argument for not exempting nonprofits from property taxation is that they use many of the resources that are supported by the revenues of the property tax system (e.g., infrastructure, public safety, etc.). On the other side, the argument for exempting nonprofits from property taxation is that taxes would be an added expense that would decrease the funds available for that nonprofit’s charitable mission. In addition, for nonprofit sectors that have paying “customers,” say a private university, that property tax bill would likely, at least partially, get passed on to students through higher tuition.

It is worth noting that there are nonprofits that make voluntary payments to local governments even though they are exempt from property taxation. For example, in fiscal year 2014, Brown University made over $5 million of voluntary tax payments to the city of Providence. So, there is some recognition by nonprofits that they are using government resources, and if able, should help pay for them.

Overall, I do not think that property taxes for nonprofits is a policy that is off limits. I think it is a policy that legislatures should think about. However, even if a jurisdiction decided to start collecting property taxes from nonprofits, they would likely still provide some preferences to them, relative to other types of landowners. For example, subjecting property held by nonprofits to a lower rate, still exempting certain types or sizes of nonprofits from property tax, etc.

Should local tax policy be adjusted to rely more or less on property taxes versus other forms of taxation?

One thing that is quite unique about tax policy is that a jurisdiction has a lot of autonomy in designing the tax system it believes will work best for it. Thus, we see significant variation across the country in how state and local governments design tax systems. Some states, such as Texas, have high average property tax rates; however, the trade-off is that Texans do not pay state income tax. Then, you see other states, such as Hawaii, that generally have low property tax rates, but have high state income tax rates. At the end of the day, governments need revenue, and they are going to collect that revenue from some sort of taxation.

An advantage of relying more on the property tax system relative to other taxes to collect revenues is that real property is fixed in location. That is, if you own a piece of land with a house on it, then it is very clear what taxing jurisdiction that property will be taxed in. Whereas with income taxes, there is the ability to engage in tax planning strategies to shift income from higher-taxed jurisdictions to lower-taxed jurisdictions. A drawback of relying too heavily on the property tax system is that without sufficient controls, the tax can significantly burden property owners in periods of rising property values.

There is a concept in tax system design known as the wherewithal-to-pay concept. The general premise is that the taxpayer should be paying the tax when he/she has the wherewithal to pay it. In the income tax system, this is fairly straightforward, because the taxpayer receives salary/wages/investment income throughout the year, and then files a tax return and pays the tax. In this case, the taxpayer has already received cash inflows related to the income, and thus should have the cash available to pay the tax. However, property taxes are a function of the assessed fair market value of the property, so taxpayers are being taxed on increased value in a home that they have not received any cash inflows from.

So, there are situations where a taxpayer purchases a home at a monthly payment that he/she can afford, but if that house drastically increases in value over time, then the additional property taxes can really burden them, particularly if their wages/salary have not been increasing as similar rates. However, some ways you see this addressed is that some jurisdictions have a maximum year-over-year increase in assessed value of properties. So, say the home actually increases in value by 10 percent this year, the law may cap that increase at, say, 2.5 percent for the purposes of calculating property taxes. In addition, there are jurisdictions that have property tax freezes for individuals over a certain age (e.g., over 65), so that these retirees do not get forced into the situation of leaving a home that they can no longer afford the property taxes on.

Deborah Meyer CEO & CCO of WorthyNest

Do people consider property taxes when deciding where to move? Should they?

When people move, they are often focused on the main driver behind the move (i.e., job offer, proximity to family or friends, etc.), and less concerned about the property or income tax implications of the move. However, taxes have a substantial long-term impact on a family’s financial situation and should be considered. Many states that offer low income tax rates make up for the lost tax revenue through higher property taxes. For instance, although Illinois offers a relatively low state income tax rate of 3.75%, average Illinois < a href= https://www.usatoday.com/story/money/personalfinance/2017/04/16/comparing-average-property-taxes-all-50-states-and-dc/100314754/>property taxes in 2016 ran $4,845. This represents an effective property tax rate of 2.13%, nearly one percent higher than the national average of 1.15%.

In light of the new Tax Cuts and Jobs Act of 2017, property taxes are an even bigger issue. For families who itemize deductions, state and local property and income tax deductions are now limited to $10,000 annually on individual tax returns for tax years 2018 and beyond. If you take full advantage of a 2017 property tax deduction, you may find a different situation when filing your 2018 tax return; families who previously itemized deductions may find it more advantageous to take the enhanced standard deduction.

Should nonprofits pay property taxes?

By law, a nonprofit that is granted federal tax-exempt status by the Internal Revenue Service will also be exempted from property tax. For nonprofits based in high property tax states, such as New Jersey, New York, and Texas, this exemption is incredibly valuable -- particularly if the nonprofit owns substantial acreage. Unfortunately, this exemption shifts the burden of public benefits, such as police patrol and streetlights to the homeowners and for-profit businesses. Some local municipalities attempt to ease the financial burden facing taxpayers, and therefore, require nonprofits to make payments in lieu of taxes.

In my opinion, nonprofits should have some “skin the game.” I understand nonprofits are serving the public good, but there are also many for-profit Certified B Corps who meet rigorous standards of social and environmental transparency, yet do not enjoy the exemptions provided to tax-exempt entities. States and municipalities need tax revenue to support broader public interests, and leaving nonprofits out of that revenue source means additional taxes for homeowners.

Tiffany B. Ballard Wealth Manager at Bergland Wealth Management

Do people consider property taxes when deciding where to move? Should they?

Occasionally, property taxes are considered prior to relocating to another state. However, the top two reasons for moving tend to be either job-related, or to be closer to family. As one can imagine, taxes take a backseat when competing with a better job or that new grandchild. Yes, property taxes should be taken into consideration if a person is relocating to a state that has significantly higher property taxes. Odds are overwhelming that there is a greater cost of living, which should be accounted for in their overall plan. Failure to account for increased living expenses can have a negative impact on accomplishing one’s long-term goals.

Should more types of property be subject to property taxes? If yes, what types?

No.

Should certain groups of people be exempt from property taxes or be taxed at a lower rate?

No. The United States of America is unfortunately divided today. Segmenting groups of people to give them benefits of tax exemption or a lower tax rate does not provide a path to unity. If anything, segmenting groups of persons feeds discrimination.

Todd Minear Financial Advisor and President of Open Road Wealth Management

Do people consider property taxes when deciding where to move? Should they?

When deciding where to move, all taxes should be considered and that, of course, includes property taxes. Only comparing property taxes could give bias to the region with lower property taxes, as such a region may have other taxes, such as state, local, sales, and earning taxes that are higher than in the higher property tax region. In other words, a property tax to property tax comparison could be the same as comparing apples to oranges. For a true apples-to-apples comparison, all taxes should be included in the analysis.

Another property tax thought is that they have at least two ways to go up -- increased assessed value, and higher property tax rates. While assessed rates may go down, as we saw in some regions during the Great Recession, property tax rates rarely go down. Ever notice on ballots, “no increase in property taxes?” That’s because when one tax levy is expiring, another is proposed to take its place. And still others are added, that increase property taxes.

Kathleen Longo President & Founder of Flourish Wealth Management

Do people consider property taxes when deciding where to move? Should they?

Yes, in my experience, people definitely consider property taxes when deciding where to move. This decision is especially relevant at retirement, as they look to find their “final home” while working to drive down and manage their fixed expenses. When considering a move, they will look at the whole tax package, including property taxes, state income taxes, sales taxes, and some will also consider estate taxes. There are certainly other life factors that come into consideration, like proximity to family and community resources.

It will be interesting to see the impact of the new tax laws in 2018, which limit the state and local tax deduction for property and real estate to a maximum of $10,000, which will be less appealing for higher-tax states. There are also new restrictions on the ability to deduct mortgage interest on the first $750,000 of home debt incurred after December 15, 2017. The combination of these provisions may decrease the appeal of a new home purchase, even in retirement, but increase the need to incorporate tax considerations in the purchase process. Overall, I think people need to look at a number of factors in considering where to move, such as proximity to social support with family and friends, access to quality medical care and other life resources, along with the financial trade-offs for the whole tax package.

Should nonprofits pay property taxes?

I support a number of local nonprofits as a Board Member, Committee Member, Volunteer, and financial donor, so my passion is to help nonprofits accomplish their mission. Every dollar is precious for these organizations, as they strive to accomplish their mission and support the local community. If a new expense for property taxes was added to the budget, many nonprofits would struggle to accomplish their mission statement, and could potentially be in danger of staying financially viable. At the same time, the entire community benefits from the efforts of the various nonprofit entities, and I believe those positive contributions outweigh any potential income from property taxes, so I think the current system, where nonprofits are exempt from paying property taxes, should stay the same.

Should certain groups of people be exempt from property taxes or be taxed at a lower rate?

I have seen many situations where older, retired people are forced to leave their long-term homes due to the rising costs of property taxes. To address this unfortunate situation, I would be in favor of reducing or exempting long-term homeowners based on age. Some states are already offering property tax exemptions to the elderly, including South Dakota, Washington, and Texas. Each state has its own way to apply these exemptions and they are subject to change, but it is an important consideration for our retired clients who are looking to relocate and will most likely live in their new home for over 15 years. I would support broader adoption of property tax exemptions for homeowners over age 65 to help this segment of our population, which is also becoming larger every year, as the baby boomer generation ages.

Kenneth J. Eaton Managing Principal of Stepp & Rothwell

Do people consider property taxes when deciding where to move? Should they?

Most of my clients are relatively affluent and they are located in low-cost and high-cost states. From the conversations that I have had with them, as well as with other friends and acquaintances, I think that most people in their socio-economic category perceive property taxes as the price of doing business. When they move into an area, they are much more focused on safety, accessibility, proximity to work, and quality of education, and they are willing to pay more in property tax for those benefits, especially if the surrounding areas have similar tax regimes. I also think that most people feel better about paying tax to their locality than to a state or federal government, because they perceive a tangible benefit in the form of cleaner streets, police presence, better schools and the like.

Jon Ripans Property Tax Attorney, Commercial Real Estate Appraiser, Arbitrator and General Mediator at Valuation Matters LLC and The Ripans Law Firm LLC & Property Tax Affiliate Member of the Institute for Professionals in Taxation

Do people consider property taxes when deciding where to move? Should they?

Property taxes often play a role in where people live, even if indirectly. Property taxes show up in the rents people pay for apartments or homes, as well as in monthly mortgage payments. This can affect loan approval in which the affordability of housing in the mortgage underwriting process considers the overall principle, interest, taxes, and insurance (PITI) payments of a proposed loan as a percentage of household income.

Whether people directly pay attention to property taxes in deciding where to move often depends upon geography, commuting times, and proximity to shopping, desirable schools, and other amenities. “Tax flight” is easiest when just a small change in location, commuting times, and amenities results in a big difference in affordability caused by the property tax component of monthly rent or mortgage payments.

In the larger states (geographically) in the Western United States, with larger counties (geographically), “tax flight” or “tax hopping” is fairly difficult. But, back East, particularly in New England and the “tri-state” areas of New York, Philadelphia, and Washington, D.C., tax avoidance is easier. It is even possible in Georgia and Virginia, which have the second most and third most county-equivalents in the United States, at 159 and 133, respectively.

Of course, businesses often consider the overall tax climate when deciding where to locate or where to incorporate. Sadly, Connecticut is still smarting from the defection to Massachusetts of long-time corporate resident General Electric.

Should nonprofits pay property taxes?

In most U.S. jurisdictions, nonprofits do pay property taxes unless they meet all of the following criteria: they are non-profits, they are engaged in educational, charitable, religious, or other activities that are “in the public good,” and the property at issue is not only owned by the nonprofit, but is actually being used for one or more of those purposes.

So, for example, there is a Georgia Court of Appeals case in which a church owned a second building that was undergoing extensive renovations which took more than one year. The court held that the property was not exempt from taxation during the time that it was not being used for activities consistent with the mission of the church. But, of course, the condition of the building and the fact that it was unusable affected the value for property tax purposes.

If nonprofits use property to make money, for example, by renting out a banquet hall for weddings or other receptions, they are often subject to property taxes. The effects of this can be mitigated by splitting the property into two tax parcels -- one for the exempt parish/sanctuary and another for the taxable portion of the property. This has also appeared in a Georgia Court of Appeals case.

Ultimately, the more exceptions and “carveouts” there are from the tax base or tax digest, then the higher the property tax rate (millage rate) needs to be to meet the revenue targets of local governments and school boards (unless they can make up the difference with sales and income taxes or user fees). Most tax jurisdictions readily allow nonprofits to avoid taxation, so long as the exempt property is being used exclusively for the purposes discussed above.

Should local tax policy be adjusted to rely more or less on property taxes versus other forms of taxation?

This is a very interesting question that is within the discretion of each state. Every state taxes at least some property, whether it is business property, apartments, or automobiles, even if private residences are virtually exempt. And, some states tax commercial real estate at a different rate than single-family residences.

When it comes to owner-occupied houses, Hawaii, Alabama, Louisiana, Delaware, D.C., South Carolina, West Virginia, Wyoming, Colorado, and Arkansas have the lowest statewide average rates. But, this can be misleading. Arkansas is reported to have a statewide average of about 0.62 percent of fair market value. Some city/county combinations in Arkansas are higher. In the meantime, there are very nice lake homes in unincorporated Putnam County, Georgia, with effective tax rates of about 0.69 percent of fair market value, while some houses inside the City of Atlanta portion of Fulton County, Georgia have effective tax rates approaching two percent.

Ultimately, state and local governments are overwhelmingly funded by three forms of taxation: income taxes, sales taxes, and property taxes. In the United States, there are approximately 3,143 counties, parishes, or boroughs. The average size is about 100,000 people, but half of Americans live in just 150 counties. Los Angeles County has 10 million people and could generate quite a bit of revenue just from income and sales taxes. But, there are counties throughout the country with surprisingly low populations. Delaware is broken into three counties, but one of them has only 170,000 residents, which is not a very large population when it comes to raising revenue through sales and income taxes. Georgia has twenty-five counties with 10,000 or fewer residents, including one with only 2,000 residents. In Loving County, Texas, which boasts 113 hardy souls, everybody really is somebody. New York City subway cars can hold over 100 persons seated and standing.

With a dependence upon state-wide income taxes instead of local property taxes, revenue flows to the state capital, where it is reallocated based upon statewide politics, as opposed to local priorities. You can hear the protest: “Why is the neighboring county getting a new high school when ours is older?” And, depending upon geography, a lot of sales taxes can be avoided. This isn’t just a “case” of liquor runs from one New England state to another, where alcohol taxes are lower. With 10 million people, Georgia has passed New Jersey as the tenth most populous state in the United States. Yet, when you see how close downtime Atlanta is to the Alabama line (55 miles) and its various exurbs are to the Tennessee and South Carolina lines, one can easily imagine large purchases and other shopping sprees taking place outside the state if Georgia sales taxes were to rise substantially.

Columbus, Georgia has a huge population thanks to Fort Benning, and Alabama is right next door. Ditto Augusta, with Fort Gordon with South Carolina right next door. Savannah has Fort Stewart and South Carolina is right next door, and Jacksonville just a zip down I-95. So, loss of sales tax revenue is a real possibility, and even income taxes for those who commute from nearby states. Is a one-hour commute from northern Jacksonville to southern Savannah worth it to save on income taxes? Some people vote with their gas pedal.

This is a big problem in New England and the tri-state areas of New York City and Philadelphia, but it can even show up in Georgia, which is the largest state by land mass east of the Mississippi River (no fair, Michigan and Florida, we don’t want to hear about how much coastal water is within your boundaries, at least not when it comes to property taxes).

The solution is generally to have individual and business taxes that are a mix of moderate property taxes, moderate income taxes, and moderate sales taxes. It lessens the incentives for sales tax and income tax avoidance.

Should more types of property be subject to property taxes? If yes, what types?

The more property that is exempt from taxation, the higher the tax rate must be on remaining properties in order to meet the revenue needs of local government, unless a jurisdiction can capture the necessary revenue through sales or income taxes or from user fees.

Property taxes usually start with each state’s constitution, and those constitutions start off by saying that all (tangible) property shall be subject to property taxes (ad valorem taxes).

What happens next is a matter of politics and of voter choice over time, resulting in lots of carveouts in various states. Even though a constitution trumps a statute, some states allow this to happen merely by the supermajority passage of a statute that is signed into law by the governor. Other states require that a referendum or constitutional amendment be approved by the voters. This is usually something voted out of the legislature in the spring and placed on the ballot in the fall election.

Common exemptions or partial exemptions in many states include:

- Homestead exemptions for primary residences (usually with evidence of voter registration and at least one motor vehicle being domiciled there);

- Sheltering retirees from the public-school portion of the property tax bill (which is often 60 percent);

- Property placed in conservation easements;

- Historic preservation properties;

- Brownfield properties undergoing environmental remediation;

- Certain pollution control equipment;

- Timber or other multi-year crops, until the year in which they are cut/harvested, at which point they are subject to a severance tax -- otherwise, they would get taxed every year (even if at a very low rate), despite the possibility of eventual crop failure due to weather, fire, disease, etc.;

- Various agricultural lands or equipment.

Of course, not all these exemptions have the same impact in different jurisdictions. For example, Savannah, Georgia, and Charleston, South Carolina, have numerous historic preservation properties in prime locations, but they are also small jurisdictions where the removal of these properties from the tax rolls has a much bigger impact than it would, say, in Philadelphia or Boston.

Also, there are state and federalism issues. Property owned by the state or the federal government is often exempt from taxation by counties, cities, and school boards. This has a huge impact in Washington, D.C., which is only 68 square miles, but loses a lot of land to everything from the National Mall and Rock Creek Park to the U.S. Capitol Building and grounds, the Supreme Court, and the White House. It can also have a huge impact in counties with large military installations or colleges/universities. Madison, Wisconsin, Tallahassee, Florida, and Austin, Texas, each have a large university and a state capital with lots of government buildings. Columbia, South Carolina, in Richland County, has a trifecta, with the University of South Carolina, the state capital, and Fort Jackson.

Should certain groups of people be exempt from property taxes or be taxed at a lower rate?

The most common exemption is a homestead exemption for a person’s primary residence. This reduces, but does not eliminate, property taxes, but enables a person to pay a little less in property taxes on the property that they occupy as a primary residence than they would on the exact same house that they also happen to own across the street, but rent out to a tenant.

Other common exemptions are for retirees, especially for the public-school portion of the tax bill, exemptions for veterans, and surviving spouses of military, first-responder, and public safety personnel.

Ultimately, exemptions or a difference in tax rates is a matter of voter or legislative choice, which pits notions of fairness and decency against the mathematical reality that the more people or properties are exempt or partially sheltered from taxation, the higher the overall tax rate must be for property taxes, unless the difference can be gained back through sales and income taxes or other user fees.

It is up to each taxpayer, perhaps with the assistance of a family member, neighbor, or a professional, to check out the laws of the jurisdiction to find out what exemptions might apply to him or her, or to his or her property. These exemptions, as well as instructions and deadlines, can usually be found by visiting the web page for the county department of revenue or board of tax assessors, or sometimes on the web page for the state department of revenue. Many deadlines are December 31/January 1 or March 31/April 1.

There are even steps that can sometimes be taken to mitigated taxes for a long time. For example, in Georgia, a person with a house on a large rural tract might want to sever the house and a couple acres of land from the larger tract, and put the latter into a state (not federal) conservation easement for ten years. There are limitations and restrictions that come with this, but the tax savings might be worth the time and effort of commissioning a survey and a quit claim deed. A federal conservation easement contains severe limitations and is almost always in perpetuity.

People need to remember that property taxes are unique. Unlike all other forms of taxation, in property taxes, the government tells you what the value is going to be and how much you owe. And this is based upon subjective determinations, because real estate valuation is not an exact science. Other forms of taxation, such a sales taxes, income taxes, capital gains taxes, etc., are overwhelmingly self-reporting and objective. You pay $500 for a big screen TV, the sales tax is $35, end of story. Not so with real estate. In other forms of taxation, it is the taxing authority that initiates the appeals process. In ad valorem taxation, it is up to the taxpayer to determine whether an appeal is justified. The good news is that for most properties and tax years, a tax appeal is not justified. But, the best way to find out is to do some research or to consult a professional. Or both.

Tod Buckvar Vice President at Buck Realty

Do people consider property taxes when deciding where to move? Should they?

Yes, and they should as well. Property taxes are a constant expense, and one that generally doesn’t decrease but only increases. Additionally, most homes with high property taxes are located in better school districts as the community pays more into the school budget, which enables more programs for the students. When buying a home, the quality of the school district is a major factor in determining which home you purchase.

Should local tax policy be adjusted to rely more or less on property taxes versus other forms of taxation?

It should be adjusted to rely less upon property taxes, as eventually, this system will not be sustainable. People will no longer be able to live in those areas as they will no longer be able to pay the taxes, which will result in the bankrupting of the municipalities. Peoples’ wages and compensation cannot keep up with the tax increases.

Should certain groups of people be exempt from property taxes or be taxed at a lower rate?

Yes -- families starting out, people paying student loans, and low-income and senior citizens. Right now, these are the people who should be buying homes, but they cannot, because they cannot afford the taxes. Perhaps implementing programs for first-time homebuyers where there is a tax abatement will include additional incentives for recent graduates who have a lot of student loan debt. Provide a program with a reduced initial tax amount, gradually increasing each year.

Joe Pitzl Managing Partner at Pitzl Financial

Do people consider property taxes when deciding where to move? Should they?

For most people, I believe they primarily consider property taxes in the context of their monthly PITI payments. They absolutely should consider them, but they should look into the financial strength of the taxing county and city, as well. Property taxes tend to increase far more rapidly in areas that are struggling financially. In addition, these taxes support a lot of vital local services, so that same assessment of financial health can shed light into how likely it is their property taxes will be used for services they care about.

Should nonprofits pay property taxes?

I believe they should. Property taxes support local governments, which are responsible for law enforcement and fire, road and park maintenance, water and sewer, waste disposal and recycling, etc. These are all services that nonprofits rely on to operate effectively, and they expect them to respond and treat them in the same manner as they would for any for-profit entity, renter, or homeowner. I completely agree with exemptions from state and Federal income taxes, as many nonprofits offer services that would otherwise require Federal or state funding. However, they are heavy participants in local government services and usually do not replace those services.

Should local tax policy be adjusted to rely more or less on property taxes versus other forms of taxation?

I think property taxes are a very effective way to handle local taxes, as the beneficiaries of local governments are overwhelmingly the residents and businesses that are located there.

Should certain groups of people be exempt from property taxes or be taxed at a lower rate?

I think this is done fairly effectively via the income tax system. Everyone benefits from local government services and are consumers of those services, to a certain degree. Many local governments are already stretched thin, so adding additional layers of complexity to a reasonable system is likely to end up counterproductive.

MethodologyIn order to determine the states with the highest and lowest property taxes, WalletHub compared the 50 states and the District of Columbia by using U.S. Census Bureau data to determine real-estate property tax rates and applying assumptions based on national auto-sales data to determine vehicle property tax rates.

For real-estate property tax rates, we divided the “median real-estate tax payment” by the “median home price” in each state. We then used the resulting rates to obtain the dollar amount paid as real-estate tax on a house worth $184,700, the median value for a home in the U.S. as of 2016 according to the Census Bureau.

For vehicle property tax rates, we examined data for cities and counties making up at least 50 percent of a given state’s population and extrapolated this to the state level using weighted averages based on population size. For each state, we assumed all residents own the same vehicle: a Toyota Camry LE four-door sedan — 2017’s highest-selling car — valued at $24,000, as of February 2018. Please note that Georgia formerly imposed vehicle property tax but replaced it in 2013 with a one-time tax imposed on a vehicle’s fair market value (FMV).

Sources: Data used to create this ranking were collected from the U.S. Census Bureau and each state’s Department of Motor Vehicles.

from Wallet HubWallet Hub

via Finance Xpress