How Will New York’s Battle Against Corona Impact Values of NYC-Based Companies?

12:28 AMThe post How Will New York’s Battle Against Corona Impact Values of NYC-Based Companies? appeared first on The Dough Roller.

via Finance Xpress

We speak with a governor, a former C.D.C. director, a pandemic forecaster, a hard-charging pharmacist, and a pair of economists — who say it’s all about the incentives. (Pandemillions, anyone?)

Listen and subscribe to our podcast at Apple Podcasts, Stitcher, or elsewhere. Below is a transcript of the episode, edited for readability. For more information on the people and ideas in the episode, see the links at the bottom of this post.

* * *

Our new podcast is called No Stupid Questions. You can go ahead and subscribe now on Apple Podcasts or Spotify or Stitcher — wherever you get your podcasts. We’ve already posted a preview, and starting May 18th we’ll be putting out a new episode every Sunday evening.

Also: announcement number two. Something the Covid-19 pandemic has us wondering is: What’s college going to look like this fall? Maybe you are wondering that too. If you are a student or parent or college faculty or staff member with a question or concern or maybe an insight, we would like to hear from you for possible inclusion in an upcoming episode. Use the voice memo app on your smartphone and e-mail the file to radio@freakonomics.com. Please include your name and where you live.

* * *

Stephen J. DUBNER: Hello, it’s Stephen. Can you hear me?

Gina RAIMONDO: Yes. Hi. Good morning, Stephen.

DUBNER: Good morning. How are you, Governor Raimondo?

RAIMONDO: I’m hanging in there.

DUBNER: How’s your life these days generally?

RAIMONDO: Pretty calm. Not much going on. Everything’s in order.

Gina Raimondo is the governor of Rhode Island, which had its first Covid-19 diagnosis on March 1st.

RAIMONDO: We were one of the first ten states in the U.S. to have a positive case. We’ve been at this for a while.

More than 7,000 people have since tested positive in Rhode Island, and over 200 have died. I spoke with Raimondo on April 19th, a Sunday morning.

RAIMONDO: So I think that we are probably a couple of weeks away from our peak. We’re still climbing up the curve.

Like the rest of the U.S., Rhode Island has been sheltering in place. Only essential businesses are open and the economy has cratered.

RAIMONDO: There’s a lot of people now who — and maybe I’ll put you and a lot of my friends in this category — their lives have been inconvenienced, surely, but they’re not devastated. They grab their computer and their phone. They work from home. They’re still getting a paycheck. That isn’t the majority of Rhode Island right now. The majority of Rhode Island really is struggling.

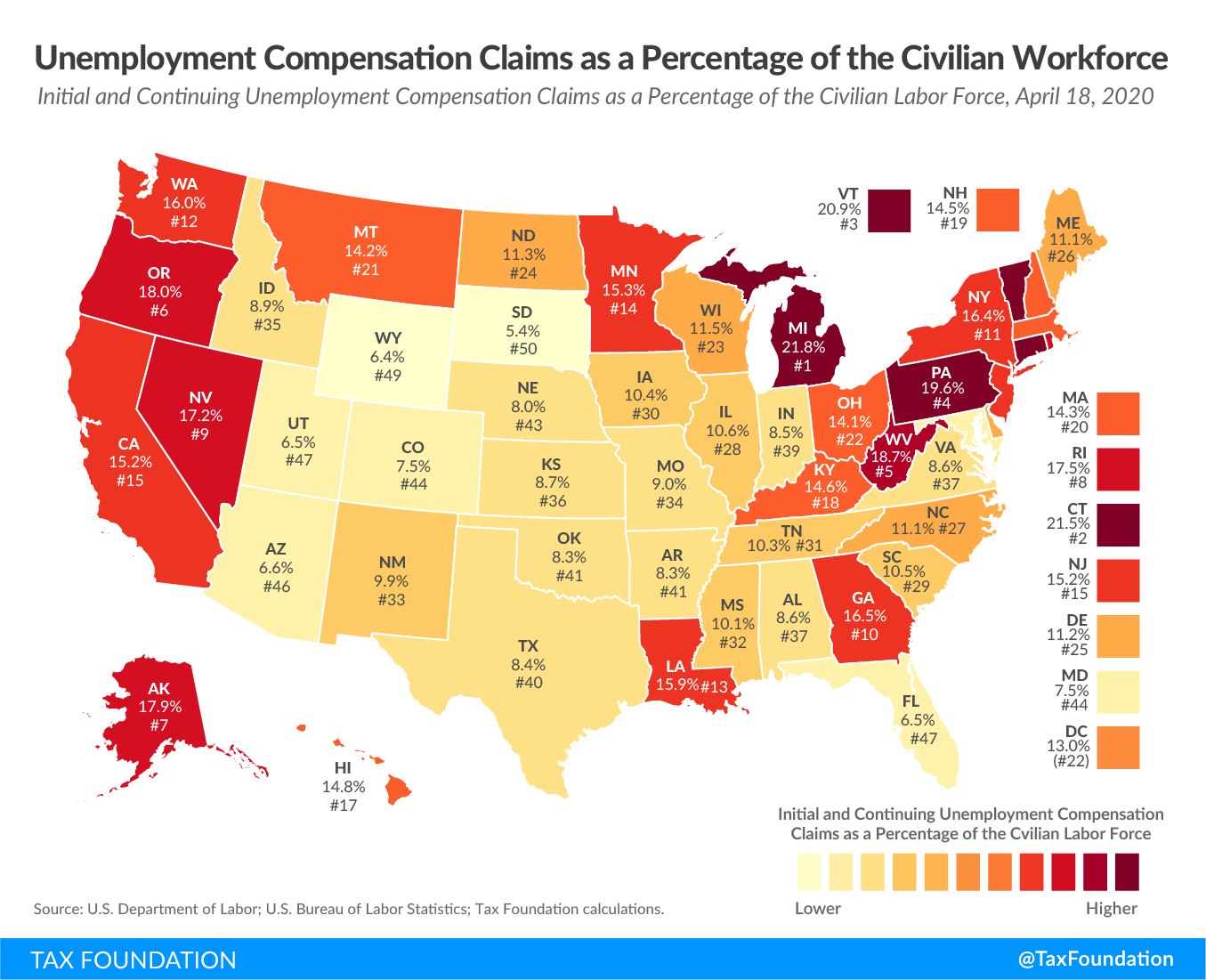

With a population of just around one million, Rhode Island has had 170,000 people file for unemployment. That puts it in the top ten nationally for the largest unemployed share of the civilian workforce.

{kind=link}

RAIMONDO: So I’m obsessed, with every minute of every day thinking, “What’s it going to take to safely reopen the economy? How can I get the most people back to work the fastest, as safely as possible?”

Rhode Island’s current stay-at-home order is set to expire on May 8th, but new infection rates are still high.

RAIMONDO: There’s no good options. I’m choosing between bad option number one and bad option number two. And all of the work that we’re doing is to make this a bit less bad for people: minimize death, minimize the virus, minimize economic hardship.

This dilemma is shared by governors across the country, by elected officials around the world. A few U.S. states have begun at least partial reopenings. Others plan to reopen soon, while some are likely to extend their shutdowns. That will of course only deepen the economic cataclysm.

DUBNER: So there is a chance that restarting the economy, whenever and however it happens, will fail — given inadequate testing and our limited knowledge of the virus to date. What would it take for you to admit failure and return to lockdown if that were the case?

RAIMONDO: That is the worst possible outcome. When I reopen, I’m going to have a set of metrics based on science and fact which will say if your infection rate starts to look like this, if your hospitalizations are doubling this quickly, then you have to hit the brakes again. The whole point of all of what we’ve gone through is that you won’t again have to do a wholesale shutdown.

Consider the 1918 influenza pandemic. It killed roughly five million worldwide, around 675,000 in the U.S. Our population then was about one-third what it is today — so the modern equivalent of around two million people. The 1918 pandemic hit the U.S. in three waves: spring, fall, and winter. The first wave wasn’t that terrible; the third was bad; but it was the second that easily killed the most people. This fact, if you are a governor, weighs heavily on your decision of when and how to reopen the economy.

RAIMONDO: There is risk. There’s no risk-free option here.

Today on Freakonomics Radio: how can that risk be mitigated? We discuss Covid-19 exit strategy with a former head of the Centers for Disease Control; a pandemic forecaster; a hard-charging pharmacist; and, of course, a couple of economists, who have economist-type ideas:

Steve LEVITT: So you could imagine we could put something like $1 billion a week into this lottery.

* * *

Covid-19 has so far killed more than 50,000 people in the U.S. I asked Gina Raimondo to describe what it was like when the disease first hit Rhode Island.

RAIMONDO: I cannot describe to you the chaos in the first few weeks of this. We were so poorly prepared for this crisis. The federal government was absolutely not ready. The federal stockpile wasn’t where it should have been. They moved much too slowly to ramp up manufacturing of P.P.E. and testing. So we were just scrambling for too long and we’re behind. We’ve been playing catch up from day one. Because we were one of the first states to have a case, within a week, I had banned large gatherings. I was one of the first states to do that. Closed schools, one of the first states to do that. At the time, I got a lot of pushback. People said, “It’s not necessary. You’re overreacting.”

DUBNER: Pushback internally, externally, from where?

RAIMONDO: Constituents in Rhode Island. I remember the first call I had to have with our bishop, which was a difficult call. And I asked him if he would please consider suspending Sunday mass. And at the time— and he was excellent and cooperative, but reluctant at that time. And, of course, eventually he did do what in hindsight was clearly the right thing. Everybody cooperated. And as a result, now we— it worked. We never had the extreme spikes. Our healthcare system has never been overwhelmed.

Raimondo had two temporary hospitals built, with a third on the way, totaling 1,000 beds; so far they haven’t been needed.

RAIMONDO: I mean, it’s still all horrible. The amount of pain and suffering and economic hardship is so extensive and extreme. But two weeks ago when I was looking at our models, we were looking at a need for six or seven thousand hospital beds. That was a scary place to be.

DUBNER: Those models persuaded a bunch of governors to take extreme action. Do you have any reservations now about having followed those extreme models, or do you think it was ultimately the right move?

RAIMONDO: Ultimately the right move.

DUBNER: In late March, when it was becoming clear that New York was a hotspot, you were sending police officers and National Guard troops to intercept cars with New York license plates to tell people that they had to self-quarantine for two weeks. You sent police to the main airport and the train stations. They went door-to-door in resort towns looking for New York plates. So tell us about that incident, what you did right there, maybe anything you did wrong.

RAIMONDO: Yes. So I would do that again on the basis of all the information we were receiving. As I looked at other communities outside of Rhode Island, the rate of infection was so much higher than what we were seeing and I had Rhode Islanders in coastal towns calling me, saying, “Hey, Governor, when we go to Stop and Shop, it’s all out-of-state cars. Help us.” They were afraid. I had to respond to that.

Her response provoked a response from New York governor Andrew Cuomo:

Andrew CUOMO: If they don’t roll back that policy, I’m going to sue Rhode Island. Because that clearly is unconstitutional.

RAIMONDO: In retrospect, I should have not singled out one state. So if you recall, I did an executive order one day.

DUBNER: And then you later included the other states, right?

RAIMONDO: And then the next day, I included every state. So were I to do it all over again, I would’ve not done the New York executive order, followed by everyone. I would have treated everybody the same. By the way, in all of the hyperbolic headlines — “Rhode Island Governor, Police State, Lockdown” — we never closed our borders, right? We were welcoming to anyone who wanted to come here, you just had to provide us with information so we could keep you safe and the people of Rhode Island safe.

DUBNER: Did you think about closing your borders?

RAIMONDO: No. No, I didn’t.

DUBNER: Is it legal?

RAIMONDO: It’s a good question. It would depend. I’d say probably not. That would be a real interference with interstate commerce.

DUBNER: You’re being asked to come up with a strategy for restarting the economy, but without what I would think is the testing capability that experts say are necessary, without good information about even what behaviors will or won’t spread the disease at this point. So do you feel— I mean, bad and worse is one way of describing it. Impossible, I guess, is another way to describe it.

RAIMONDO: So you’re absolutely right, by the way. The key things are: you have to rely on the data that you can get your hands on. So in my discussions, the loudest voice in the room is my public health advisor. All that matters is that you try your best on a daily basis with the facts before you to make the best decision you can. And, here’s the hard part for politicians: be willing to change. So, as the facts change, as our information about the virus changes, people like me have to be willing to say, “I’m changing. I was wrong.”

DUBNER: So I’m guessing your lockdown exit strategy has different phases of reopening, like most plans. What do you see as the easiest and hardest parts of society to reopen?

RAIMONDO: So it will be a phased plan and we all as a country have to get ready for social distancing for the next year. Now, what that looks like in the beginning will be crowds of fewer than five or ten people. Months from now, it will obviously be bigger crowds.; it could be 50 or 100. But the days of hand-washing, mask-wearing, and social distancing are here to stay until we have a vaccine. I don’t think people really get that, so I say it often. The hard call for me is school. That’s a really tough call for me right now: what to do about school.

DUBNER: I mean, thank God kids are not particularly susceptible. That’s a huge blessing of this weird virus, right?

RAIMONDO: Huge. That’s huge. But a lot of them live with grandma and grandpa, aunts and uncles. Custodians in schools are often over 50 or 60. Lots of teachers are over 50 or 60. None of us has ever gone through this before. It’s hard to call somebody and say, “How would you handle it?” Because none of us has gone through it.

Julie GERBERDING: When I first saw the number of patients being admitted to the hospital in Wuhan, China, I knew that this was going to be a bad outbreak.

And that’s someone who has been through a few pandemics.

GERBERDING: But I think the moment that I really grappled with the transmissibility was watching that cruise ship in Japan and seeing how that disease spread so quickly to involve so many passengers on that boat.

That’s Dr. Julie Gerberding.

GERBERDING: I was the director of the U.S. Centers for Disease Control and Prevention, or C.D.C., from 2002 to 2009.

Gerberding is an infectious-disease expert. These days, she is the chief patient officer for the pharmaceutical firm Merck. And what did she think when she first saw how transmissible Covid-19 was?

GERBERDING: That was not SARS that I knew in 2003. It was SARS that was much more transmissible at a community level.

Gerberding has been through not only SARS, but the H1N1 outbreak in 2009, MERS in 2012, and her career began back in the midst of H.I.V./AIDS. Pandemic management from the public health side, she says, comes in three phases. Number one:

GERBERDING: Phase one is really early detection. And in the case of this new coronavirus, we had fairly early translation of the fact that there was something new and dangerous going on in China. And in Wuhan, I would say they used some of the most draconian methods possible to contain the outbreak, things that would probably be impossible in a number of other more westernized countries. But nevertheless, they made a heroic effort to really slow the spread and try to minimize transmission beyond the original epicenter.

But that, plainly, didn’t happen. Once a contagion spreads to other parts of the world, you’re in phase two:

GERBERDING: Which is the mitigation phase. You can’t stop it, but perhaps you can slow it down. So that’s what has led to all these social-distancing efforts. But sometimes we forget there are two parts to mitigation. One part is really taking the social-distancing measures and all that implies seriously, but the other is making sure that we do it sustaining essential services. So how we think about balancing the need to protect people and slow down the impact on our health system and at the same time maintain our social services — that’s a tough balance to get right.

That balance is what we’re all struggling with these days. And what’s next?

GERBERDING: The final phase is, of course, recovery, and unfortunately we’re not quite there yet in most communities around the world. So we are not really developing the firm policies for how we will try to come out of this, in part because we don’t really know what’s going to happen next. Is this going to resolve as our social-distancing measures really take hold? Or are we going to see a second wave that could be as bad or worse?

Chris MURRAY: So back in the SARS-1 epidemic, all the models suggested there would be a second wave for SARS.

That’s Chris Murray.

MURRAY: I’m the director of the Institute for Health Metrics and Evaluation.

I.H.M.E. is a research group at the University of Washington whose Covid-19 forecasting has driven much of the public-policy response to date, including White House policy.

MURRAY: And of course, the vast majority of the world was susceptible. There wasn’t a second wave. We don’t really know why. And it would be great if that occurs now, but hope is not a strategy. And given what we’ve seen about how much more widely spread Covid is than SARS-1, we should expect that the risk of a second wave is great. The vast majority of the U.S. will be susceptible. And that means that we need to be better prepared in terms of testing, contact tracing, isolation strategies.

These are the measures most people agree are key to any sensible lockdown exit strategy: testing, contact tracing, and isolation strategies. But — much easier said than done. For one thing, even though the death rate has slowed, the disease is still very transmissible and somewhat mysterious. It is, after all, a novel coronavirus. It’s attacking the body in ways that the most expert doctors and scientists are still trying to figure out. One phrase you often hear when you speak with these people: “It’s the fog of war,” they say. For Julie Gerberding, one close equivalent was the AIDS outbreak:

GERBERDING: In some sense, my career is bookended by two pandemics. When I was a very junior clinician and H.I.V. was first emerging in San Francisco, I had a whole roster full of very, very sick patients, mostly young men, with what we now recognize as AIDS, but at the time, we did not have any idea what this disease was. We just had very, very sick and dying people. And they had bizarre, complicating infections and cancers. And it was a nightmare. And all we could really do for our patients was to just care about them, try to help them be comfortable and cope with their illness.

Gerberding’s own research was focused on trying to understand how H.I.V. could be acquired through blood exposure. Some AIDS patients were not receiving treatment because many doctors were fearful of contracting H.I.V.

GERBERDING: Back then, we had no idea how big the risk was. So I can only imagine what it’s like to be on the frontline of this coronavirus and recognize the hazard that health workers are experiencing, but also their frustration with it, by not having the protective equipment they need to feel confident in their safety.

Gerberding sees another parallel between Covid-19 and AIDS:

GERBERDING: Both of these situations started in an environment of complacency. When H.I.V. emerged, it took us a long time to even recognize that it was an infectious disease because we had been lulled into this false sense of security that we had antibiotics and vaccines and we were really enjoying the end of the infectious-disease threat era. And AIDS sobered us up very quickly. That: No, no, no.

We’ve had a number of scary things happen in the last several years with infections emerging from contact with animals, including bats, civets in the case of SARS in 2003, and so forth. So when the coronavirus emerged in China last year, I think a lot of people thought, “Well, it’s over there. It’s not us. We’ve seen this before. Yes, we had a SARS outbreak in 2003 and it was frightening for a while, for eight months or so. And 8,000 people were infected and 800 of them died.”

Those aren’t U.S. numbers; those are global numbers. Again: roughly 8,000 people worldwide contracted SARS, and 800 died. As of this recording, roughly three million people are thought to have contracted Covid-19, with more than 200,000 dead. Different countries have responded differently. Sweden, for instance, has not shut things down; even schools and restaurants remain open. Their goal is to achieve what’s called “herd immunity” by letting the virus work its way through the population. And on the other end of things: Singapore used what you might think of as Orwellian surveillance to identify and isolate people who’d been exposed to the virus.

GERBERDING: Those are two polar extremes of the equation, and I don’t think the jury’s in yet in terms of which ultimately proves to be the best overall approach. Each government has taken a look at its local situation. In Korea, for example, given that the majority of the early cases were all linked to a particular religious group, the country could go in and really concentrate on finding the people who were members of that congregation and getting them evaluated, tested, isolated if they were positive, or quarantined if they were exposed.

MURRAY: If you want a success story right now—

Chris Murray again, from I.H.M.E.

MURRAY: I think it’s New Zealand, which had community-based transmission, had a broad-based shut down, and has got transmission to near zero at this point.

RAIMONDO: In an ideal world, you would want to know where everyone is at all times.

Rhode Island governor Gina Raimondo again:

RAIMONDO: However, in the United States of America, we don’t live, and frankly, I don’t want to live, in that kind of a state. So we have to protect privacy and civil liberties and also, in that context, put in place the most rigorous contact-tracing system we can find.

Contact tracing meaning you inform people who’ve interacted with someone who’s tested positive so that they too can self-quarantine. I asked Raimondo what’s the best middle ground or compromise she’s seen for contact tracing.

RAIMONDO: Well, I can tell you what we’re thinking about: a lot of consumer choice, a lot of opting in, not forcing people for some of the more invasive options, making it easy, providing incentives, and just making the case to people that if they do provide their information, it will be secure. It’s never going to get into the hands of a business; it will be destroyed appropriately.

But Rhode Island isn’t there yet; they are not ready to lift the lockdown. Some states are — Oklahoma, Georgia, and South Carolina began the process last week — and that should provide some useful epidemiological data. Meanwhile, in states where political leaders aren’t ready to reopen, there have been protests.

RAIMONDO: People are angry, tired, anxious, sick of being cooped up. And, by the way, they should be. How could you not be, after being locked in your house for a month? But the test of leadership for people like me is whether we can lead people through that anxiety to a place of realizing that it’s in their best interest too, to follow the rules.

DUBNER: So how do you do that if I, let’s say, run a small restaurant and I’ve had zero dollars for the past five, six, seven weeks? And I know that there is a federal plan that’s not working very well. It’s already tapped out. It was hard to get. Let’s say I didn’t get any of that. And I get you on the phone and I say, “Governor Raimondo, I understand. I want to do my part. But you’re killing me here. You’re killing me.” What do you say to me there?

RAIMONDO: I know, and I’m sorry. There’s no other option. If I let you open right now, nobody would show up anyway because they’re afraid, and it would just make the problem worse. Because if you open now, everybody gets sick, we start flying back up the curve, we’ll be in this mess longer. So although it stinks, hang in there with me for a couple more weeks, because I want to get you back in business as fast as I possibly can. But unfortunately, until there’s a cure for this disease, we’ve got to take it slow.

A “cure” meaning a therapeutic treatment, which has remained elusive, and/or a vaccine. Scientists around the world have more than 70 different vaccine candidates in progress, with a handful already in clinical trials. Julie Gerberding again:

GERBERDING: This should be a virus for which we can create a vaccine. Merck has an animal-health business, and because coronaviruses are common across many, many animal species, we actually do have some vaccines that have to do with other coronaviruses and other animal species. So I feel very confident that we will end up with a vaccine. The question is, how fast?

Typically, a new vaccine can take about ten years.

GERBERDING: With vaccines you have to be concerned about two things. One is the length of protection, if any, and second, the safety, because if you’re going to deliver a product to someone who’s really healthy, you want to be absolutely sure that it is as safe as possible. So the testing for vaccines has to occur over a much longer arc of time, long enough to tell whether or not protective immunity occurs and lasts long enough to be practical from a public-health perspective. And studies have to be long enough so that the full spectrum of safety concerns can be observed and addressed in the process of the clinical development.

But with a public-health threat of this scope, the norms may be adjusted to accelerate things. The Trump administration said we can expect a vaccine in 16 or 18 months. How realistic is that?

GERBERDING: I’m optimistic we’ll have a coronavirus vaccine, but I’m respectful of the timeline and then the scale. It’s not going to be helpful to have a vaccine to protect some people in one country or a few countries. We’re going to need the capability of producing the vaccine so that we have equitable access among all the people who need it. And that is an order of magnitude that we have never achieved in the history of the world.

No one knows how the search for a Covid-19 vaccine or treatment will play out. History does provide a lesson or two. After four decades, there is still no H.I.V. vaccine — but there are therapeutics that have rendered AIDS no longer a fatal disease. Polio, meanwhile, has a vaccine — which is wonderful, because scientists weren’t able to come up with a viable treatment. How does this inform our thinking on Covid-19? In the absence of a vaccine (for now) or a therapeutic solution (so far), the main weapon is reducing the spread of the virus. And that is hard to do without more testing.

RAIMONDO: Yeah. Testing is the key.

Governor Raimondo again.

RAIMONDO: In a magical world— imagine if I had enough tests where every day everyone, before they walked into work, could be tested and have a result within five or ten minutes. I mean, in that world we could reopen tomorrow. Now, obviously that is not the world in which we live, but my point is testing is really a key piece of the puzzle. We’re doing more than 2,000 tests a day. So more than 2,000 per million puts us on the high end of testing. I think, however— I know we need to be doing multiples of that per day before we can start reopening the economy.

So why isn’t there more testing?

* * *

I recently called up Steve Levitt, my Freakonomics friend and co-author. He’s an economist at the University of Chicago — which, like all schools, has moved to remote teaching.

DUBNER: So, Levitt, how’s your sheltering in place going, generally?

LEVITT: Not too bad. I’m lucky I didn’t lose my job and I’m healthy. I don’t really like people that much in the first place so I don’t mind being isolated. So I know other people are really suffering, but I’ve been super lucky.

DUBNER: So let me ask you this: How useful would you say that economists have been so far during this pandemic?

LEVITT: I think economists didn’t really have a very big role in the beginning and the middle, in the sense that it was really more like a medical issue or a policy issue. But I think on the exit from quarantine, economists can be really important because the tradeoffs we’re talking about here are the kind of tradeoffs that regular people don’t think about very much, like the tradeoff between life and death versus economic activity. I think there’s also just a lot of room for economists here to be sensible guides as we think about what will work and what won’t work.

Levitt, like everyone we’ve already heard from, agrees that an exit from quarantine won’t work without a lot more testing.

LEVITT: I think there’s been an enormous failure on the part of the government in not getting testing in place. That any sensible plan we have now requires millions and millions of tests per day, far more than the capability we have, and really some of the plans suggest 20 million tests a day.

The U.S. is now performing around 150,000 tests a day.

Zack COOPER: The economy’s losing $16 to $19 billion a day, half a trillion, nearly, a month. It would just seem like the right thing to do would be to just dramatically scale up the investment.

And that is Zack Cooper, a healthcare economist at Yale. He’s part of a group of economists who routinely collaborate with policymakers.

COOPER: Yeah, so this is reaching out to folks on the Hill, in the Senate and the House, folks in the executive branch, at the White House, at H.H.S.

Cooper, like Levitt, was quickly convinced that lack of testing was a huge problem.

COOPER: So I think right now, we’re in the fog of war, where we just don’t even know how widespread Covid is across the population.

If you’ve been keeping up with the news, you’ve probably heard about several studies that do claim to measure the spread of Covid-19. But most of these studies aren’t very reliable. They don’t measure a truly random sampling, like the studies that use Facebook to solicit people — people who may already be feeling sick. Or the studies that test people who are shopping at a grocery store — people who may be less isolated than the average person.

COOPER: So I think the best studies we actually have, are some of the studies that look at the prevalence of Covid among pregnant moms.

That is, women in hospitals — New York, in this case — who are having babies.

COOPER: That’s probably the most reliable estimate of the prevalence of Covid in the population, because there is a group of folks who are very, very health-conscious, were probably avoiding going out, whereas if you start testing shoppers, that group just looks different than the folks who are sitting at home.

And what was the Covid incidence among these women?

COOPER: You’re seeing in New York that those numbers are on the order of like 15 percent.

New York, keep in mind, has been the Covid epicenter. Does that mean the numbers elsewhere are much lower? No one really knows yet. That’s why a pair of Dartmouth researchers — the mathematician Daniel Rockmore and the political scientist Michael Herron — have proposed a truly random testing of just 10,000 Americans that they claim would predict how many people are infected. Another way to know, of course, would be to have much higher testing capacity.

How will this happen? Let’s first talk about what Covid tests are and what they can do. There are two kinds of tests: a molecular, diagnostic test, usually taken with a nasal swab, that looks for the virus itself; and a blood test that looks for antibodies, which signals that a person has already been fighting the coronavirus. The idea — the hope — is that a positive antibody test means that you’ve got immunity. Germany, for instance, is considering immunity certificates for people who test positive for antibodies. But former C.D.C. official Julie Gerberding says that science isn’t clear yet.

GERBERDING: First of all, many of the tests that are now becoming available for antibody testing are not performing very well. And by that I mean they are giving false positives and false negatives. So it’s hard to interpret unless your test is one of those that has been done by a laboratory in a major medical center that’s undergone this sophisticated approval testing, or has come out of the F.D.A. as an emergency-use evaluation test.

Second problem is that we don’t know what the antibody result means. You might have an antibody, which means you’ve been exposed to the virus, but it doesn’t necessarily mean you’re not going to get it again because we don’t know if the antibodies are protective or not. I hope they will be. Usually, after infectious diseases, you do see the antibodies confer some protection, but not always. I think some people have the misunderstanding that if we could know someone has an antibody that would be a return-to-work ticket. That’s just not really the case. And if you think about H.I.V., for example, everybody with H.I.V. infection has antibodies, but nobody is cured or protected because of those antibodies. So we have to know the answer to the meaning of the antibody tests before we can really decide who should be tested and when.

The F.D.A. has granted emergency-use authorization for more than 60 versions of the Covid test from multiple manufacturers. Most of these tests are diagnostic, but a few are antibody tests. The first such authorization went to the C.D.C. on February 4th.

COOPER: I think there was a recognition that initially there was way too much regulation of testing and that that regulation was really choking off production. And they loosened the reins quite a bit, which allowed a lot of manufacturers to get expedited review and approval of their testing.

But, as we’ve been hearing, there’s still not nearly enough testing available. Why not? One reason is that the U.S. medical-supply chain, much of which runs through China, has been significantly disrupted. But Cooper says that’s only part of the answer.

COOPER: So I think there are two market failures. The first is just the sheer scale of the externalities associated with testing, meaning that we are literally paying way too little per test we perform.

That is, there should be stronger financial incentives to produce test kits, given how valuable testing is to society.

COOPER: The second is we’re looking to scale up huge numbers of tests on a scale that we’ve never done before, for a problem that’s going to dissipate pretty dramatically in 18 to 24 months. You’re asking all of these firms to put out more than they ever have, and bear the cost of doing so, without the ability to recoup those costs the way we normally think about costs being recouped over fairly long periods.

In other words, if this were your company, would you invest a lot of money in ramping up to make millions of a product now for which there may not be much demand in a year or two? If there’s a Covid-19 vaccine, there won’t be nearly as much need for a Covid-19 diagnostic test.

COOPER: So the solution to that is just paying them a ton to do that now.

And just how much is a ton?

COOPER: There just aren’t that many production issues that $250 billion can’t solve.

That is precisely ten times what Congress just directed toward coronavirus testing in the latest relief package. But as Cooper points out: if the economy is losing between $16 and $19 billion a day, and if greater testing capacity could help restart the economy 30 days earlier, that’s a savings of roughly $500 billion. Which makes $250 billion for testing look pretty affordable. Cooper has a plan to ramp up production. The first thing to do is get prices aligned.

COOPER: We basically need the federal government to set a payment rate for Covid tests that applies to all parties in the healthcare system. Right now, you’ve got Medicare paying a different rate from Medicaid, which is paying a different rate from each private insurer. That needs to change because it just drives contracting frictions.

As you likely know, economists aren’t typically in favor of fixing prices — at least under normal market conditions. But plainly, these aren’t those. So that’s one solution: a single price.

COOPER: The second is, that payment rate really needs to be quite high, sort of on proportion to the social value of testing. I think in many ways, it would be almost impossible to underspend on testing right now.

At the outset, the Centers for Medicare and Medicaid Services, C.M.S., was paying between $30 and $50 per Covid test. It has since raised payments to $100 per test.

COOPER: Now, I actually think they should be paying dramatically more. I think if you’re paying $250 per test, that wouldn’t be crazy. Frankly, I think if you’re paying a $1,000 per test, given the scale of harm we’re facing, that itself wouldn’t be crazy either.

But price alone, Cooper says, won’t increase the supply of test kits.

COOPER: There are going to be supply-chain problems in the production of tests and in the material necessary to support testing. One of things that we’ve called for is using the Defense Production Act to guarantee the production of some of the inputs to testing, like re-agents and like swabs.

In case you haven’t been following the news lately and reading about the Defense Production Act:

COOPER: So the Defense Production Act broadly allows the federal government to steer the behavior of private firms to produce necessary supplies. And then there’s a mechanism for those firms to get reimbursed. So the crude way to think about it is we say to G.M., “Look, G.M., we are going to force you into the production of Covid-testing swabs.”

The Trump administration has already invoked the Defense Production Act to get several firms to make mechanical ventilators — although, as we discussed in a recent episode, ventilators haven’t been in as short a supply as predicted; nor do they help Covid-19 patients as much as was anticipated. But, again, in the fog of war decisions are made fast, with much uncertainty and no guarantees. The next logical step, according to Zack Cooper, and just about everyone else we’ve been speaking with, is to boost production of testing very substantially and very fast.

So let’s say that happens. Let’s say Congress gets the message that testing is vital enough to spend $250 billion on, and that there are suddenly millions upon millions of diagnostic and antibody tests available. What happens next? Where, when, and how does all this testing take place? With many hospital systems already under strain from Covid-19, policymakers are talking about building separate infrastructure to deliver testing. But what if that infrastructure already existed?

Steve CHEN: Ninety percent of Americans live within five miles of a pharmacy. And in urban areas, it’s less than 1.8 miles of a pharmacy.

That’s Steve Chen. He’s a practicing pharmacist and also:

CHEN: I’m the associate dean for clinical affairs at the University of Southern California’s School of Pharmacy.

There are roughly 67,000 pharmacies in the U.S., compared to 5,500 hospitals. And how does the training of a pharmacist compare to that of a physician?

CHEN: Pharmacists study to get a four-year doctorate degree after completing an undergraduate degree. So years of training are really no different than physicians and other healthcare professionals that get a formal degree. And then furthermore, when pharmacy students are out in experiential training, they’re training side-by-side with physicians, nurses, other members of the healthcare team. Pharmacists are always there, behind the scenes or sometimes upfront, managing complex, dangerous medications, dosing medications, making recommendations or treatment changes with antibiotics for infectious diseases.

So you might think that pharmacists would be considered “healthcare providers.” Due to a quirk of history, however, they are not.

CHEN: It really starts back with the Social Security Act. In the Social Security Act, healthcare providers are defined and there’s a long list of who is a healthcare provider — everyone, of course, from physicians, all the way down to nurses and chiropractors, nutritionists, psychologists. Pharmacists are not on that list.

The Social Security Act was written in 1935.

CHEN: And back then, pharmacies were thriving businesses. And they did very well with compounding medications. And it was felt to be a critical role. There wasn’t any push at that time to be recognized as a healthcare provider.

But today, that’s more of a problem for pharmacists.

CHEN: You fast forward to today, now, reimbursement from Medicare, reimbursement from Medicaid, from health plans, it’s all tied to who is a provider, officially a provider, in the Social Security Act. So states use that to say, “Hey, we can’t pay pharmacists because they’re not officially healthcare providers.”

Chen and other pharmacist-researchers have done work showing that when pharmacists are actively involved in monitoring and adjusting medications, patient outcomes are considerably improved. But there’s no mechanism that allows them to be compensated for such work. I asked Chen what’s keeping that from happening.

CHEN: So physicians don’t necessarily want to see pharmacists carving into that limited source of funding for healthcare and being paid fee-for-service.

And this has left pharmacists, as Steve Chen describes it, overtrained and underutilized, especially during a crisis like Covid-19. Again, there are more than ten times as many pharmacies in the U.S. as there are hospitals, with 90 percent of Americans living within five miles of a pharmacy. So: would it maybe be a good idea to authorize pharmacists to administer Covid-19 tests? That’s exactly what the U.S. Department of Health and Human Services decided to do a couple weeks ago.

CHEN: I was pleasantly surprised that it got done because we’re often the forgotten stepchild.

DUBNER: How many Covid tests have been administered in California, where you are, by pharmacists now to date?

CHEN: Zero. Absolutely none.

DUBNER: Because?

CHEN: Any time any authorization occurs at any government level, there’s somewhat of a regulatory process that has to be established. There’s the authorization and there’s a translation of how it actually works and what can be done within each state. And in California that clarity was sought from the Department of Public Health. And the answer we got back is no, pharmacists are not allowed to do Covid testing in California.

That’s even though pharmacists in California can test for diabetes and high cholesterol. These regulations differ widely from state to state. Some states, for instance, allow a pharmacist to adjust medication doses, or even write prescriptions themselves. Other states don’t even allow a pharmacist to take a patient’s temperature. In New York State, governor Andrew Cuomo acted upon the H.H.S. guidance and just authorized the state’s roughly 5,000 pharmacies to conduct Covid-19 testing. As supplies permit, of course.

DUBNER: So pretend for a moment that I am Governor Newsom, governor of California, which has this ruling that forbids pharmacists from administering the Covid test, and you’ve got an audience with me. I say, “Steve Chen, you are a notable figure in the field of pharmacy. Give me your best reasons why it should happen and then tell me the biggest downside.”

CHEN: I would say that there needs to be an exception made because the number of tests for 40 million Californians that you need to get done every day is not going to get done in the current available outlets that you’re thinking of, whether hospitals or clinics or other similar locations. Pharmacists are healthcare professionals. They’re trained. They’ve been able to do this type of testing. And this is not going to be a difficult rollout if you empower pharmacists to be involved.

DUBNER: Well, Professor Chen, that sounds perfectly sensible, but my Department of Health would not have forbidden pharmacists from administering Covid tests were there not a really good reason. What are the reasons why my Department of Health is justified in not having you do these tests?

CHEN: Well, I would say that your Department of Health is reading the law as it’s written, and that’s the problem. You’ve said yourself that we need to make adjustments, be flexible, and allow every healthcare professional to practice at top of licensure in order to beat this infection. And that’s not happening. Pharmacists need to be involved in containing the Covid-19 infection in communities by offering screening, advice, self-management, self-care guidance, quarantine directions, and if needed, referral into the healthcare system, keeping patients from overwhelming emergency rooms and hospitals. And if pharmacists are not deployed in this widespread testing that’s required to lift all these mitigation measures we have out there, I don’t think it’s going to get done.

Okay, so let’s say that pharmacies across the country are enlisted to administer millions upon millions of Covid tests in the coming months, like Steve Chen would like to see. Let’s also say that the federal government comes up with $250 billion to create millions upon millions of Covid tests, like Zack Cooper would like to see. Does that solve the testing problem? Does that clear the way for a smooth and safe exit from quarantine? Not necessarily.

LEVITT: One of the pieces of exiting from the quarantine is that everybody agrees we need to do enormous amounts of tests.

That, again, is Steve Levitt.

LEVITT: What I’m struck by is that no one is talking about the fact that even if we had those tests available, the incentive problem of actually getting people to take those tests is a very difficult one. Somehow people are going to have to be compelled to do those tests. And I think in many cases, you’ll be tested every couple of weeks, even though you have no symptoms. The chances that we’re going be able to get people voluntarily to go down to their pharmacy or whatnot— so I think we have a real incentive problem.

What kind of incentive problem?

LEVITT: This is a classic case of what economists call a negative externality. The costs of me going out on the street when I’m asymptomatic are all borne by other people, right? I infect other people; they get sick. But if I don’t have symptoms— and sometimes the last thing I want to do is go get tested all the time, which is a hassle. Maybe I have to go stand by people who are sick to get tested. And then if I test positive, then I’m quarantined and maybe I lose my job if I’m quarantined. Maybe I can’t afford— you know, I have to pay the rent.

Okay, that does sound like a real incentive problem.

LEVITT: But luckily that’s the kind of problem that economists are really good at. So I think there’s an easy answer to the incentive problem that we can solve, no difficulty at all.

DUBNER: Okay, if the answer is so easy, why don’t you tell us?

LEVITT: Well, I think the answer is: you’ve got to make it worth people’s while to take this test. It’s what economists call “internalizing the externality.” So we’re going to need a lot of apparently healthy people, people without symptoms, to take this test. So I think we should pay them, and a sensible way to do that might be in the form of a really big lottery. So you might even call it, like, Pandemillions, or something like that. So you could imagine we could put something like $500 million, $1 billion a week into this lottery. And in order to get a lottery ticket, you’d have to go and get tested for Covid. And the social benefit would so swamp the costs of doing this. A billion dollars a week or something, it’s peanuts compared to even the existing CARES Act and almost vanishingly small compared to the costs overall of this disease.

DUBNER: What’s the difference if you test positive or negative, though? Do you get more chances at the lottery if you test positive because we want to incentivize people then to stay home for an additional two weeks or whatnot?

LEVITT: So I think if you test positive, it maybe gets simpler because you’re talking about a smaller group of people. I would simply just pay people to stay at home. I would pay a big enough number that even if you don’t feel sick, you’d want to stay home. So if something like, I don’t know, $2,000 per week, and you get paid that as long as you’re testing positive. I would pay handsomely for people to stay at home. I really think if the incentive plans that I’m pushing get put into place, our problem will not be getting people to stay home or to take the test. Our problem will be that people are going to cheat like crazy to try to get certain results and get into the lottery and whatnot. I’d much rather have the problem of people too eager to get tested and faking Covid than the problem we have, which is a pandemic in which people are out and about doing things and we don’t know how to stop it.

How would you respond to Steve Levitt’s Pandemillions idea? Let us know, at radio@freakonomics.com. And if you really like the idea, let your governor know, or someone else in a position to make it happen. Also: remember to subscribe to No Stupid Questions, our new spinoff podcast with Angela Duckworth.

* * *

Freakonomics Radio is produced by Stitcher and Dubner Productions. This episode was produced by Zack Lapinski, with help from Matt Hickey. Our staff also includes Alison Craiglow, Greg Rippin, Daphne Chen, Harry Huggins, and Corinne Wallace; our intern is Isabel O’Brien. We had help this week from James Foster. Our theme song is “Mr. Fortune,” by the Hitchhikers; all the other music was composed by Luis Guerra. You can subscribe to Freakonomics Radio on Apple Podcasts, Stitcher, or wherever you get your podcasts.

Here’s where you can learn more about the people and ideas in this episode:

SOURCES

- Gina Raimondo, governor of Rhode Island

- Dr. Julie Gerberding, former director of the C.D.C. and current chief patient officer for Merck.

- Chris Murray, director of the Institute for Health Metrics and Evaluation.

- Steve Levitt, Freakonomics co-author and economist at the University of Chicago

- Zack Cooper, healthcare economist at Yale University.

- Steve Chen, practicing pharmacist and associate dean at the University of Southern California’s School of Pharmacy.

RESOURCES

- “In New York City, 1 in 7 Expectant Mothers Test Positive for Coronavirus,” by Dena Goffman and Desmond Sutton (Columbia University Irving Medical Center, 2020).

- “Want to know how many people have the coronavirus? Test randomly,” by Daniel N. Rockmore and Michael Herron (The Conversation, 2020).

- “U.S. pharmacists can now test for coronavirus – they could do more if government allowed it,” by Steven W. Chen (The Conversation, 2020).

- “Estimating the cost of vaccine development against epidemic infectious diseases: a cost minimization study,” by Dimitrios Gouglas, Tung Thanh Le, Klara Henderson, Aristidis Kaloudis, Trygve Danielsen, Nicholas Caspersen Hammersland, et al. (Lancet Global Health, 2018).

- “History of 1918 Flu Pandemic,” (Centers For Disease Control and Prevention).

The post How Do You Reopen a Country? (Ep. 416) appeared first on Freakonomics.

via Finance Xpress

Investing isn’t just for the wealthy. In fact, all you need is a few bucks to get started. Here are 6 ways you can begin investing with just $100.

If you’re new to investing, the idea of getting started can be daunting. After all, you probably don’t have tens of thousands of dollars lying around to build a portfolio. Luckily, though, you can start your investment journey for a lot less–even if you only have $100 to begin. The most important part of investing is getting started as early as possible. Rather than waiting until you have a large amount of cash saved up, you can get started today. Before you know it, you’ll be well on your way to building a healthy portfolio that earns you interest and sets you up for financial success… for as little as $100. Let’s look at a few fun (and low-cost) ways that anyone can start building an investment portfolio today. Related: Masterworks Review – Invest in Art for as Little as $20

If you’re new to investing, the idea of getting started can be daunting. After all, you probably don’t have tens of thousands of dollars lying around to build a portfolio. Luckily, though, you can start your investment journey for a lot less–even if you only have $100 to begin. The most important part of investing is getting started as early as possible. Rather than waiting until you have a large amount of cash saved up, you can get started today. Before you know it, you’ll be well on your way to building a healthy portfolio that earns you interest and sets you up for financial success… for as little as $100. Let’s look at a few fun (and low-cost) ways that anyone can start building an investment portfolio today. Related: Masterworks Review – Invest in Art for as Little as $20

1. Start with High-Interest Savings Accounts

The easiest, and most flexible, way to begin your investment adventure is actually to start saving your money in a high-yield savings account. While your return will be more limited than on the stock market, it will also be a safer investment–and you can withdraw your funds at any time without penalty. If you don’t already have a sufficient emergency savings account established (ideally, six months’ worth of expenses), this is a must. Even if you do have some money saved away, a savings account can be a great way to keep a smaller amount of funds safe and secure, yet accessible. The savings accounts of today won’t earn you as much as they would have ten or twenty years ago. However, there are some online banks offering as much as 1.75% on high-yield savings accounts right now, and the interest rate climbs every day. This makes them a great introduction to the world of interest-bearing funds. Want to see some of the best interest rates today and the banks offering them? Check out our list here.2. Earn with a CD

If you want your money to earn a bit more than it would with a high-yield savings account but still need the funds to be secure against market drops, then you can look into a certificate of deposit, or CD. These savings vehicles offer a guaranteed rate of return on your investment, in exchange for locking your money away for a specified period of time. As long as you leave the funds alone until the end of the CD term, you will receive your full investment amount plus the agreed-upon interest. It’s a safe, easy way to earn extra cash on your savings! CDs come in a number of different flavors. For instance, there are CDs ranging in term from as little as three months to as many as five or six years. The longer the term, the higher interest rate you’ll be offered. Right now, for instance, you can find rates as high as 2.80% for CDs. This is double the rate offered by many banks for high-yield savings accounts, which means you can earn quite a bit more for your investment. As long as you know for certain that you won’t need to withdraw your funds early (usually incurring a painful early-withdrawal penalty), putting cash into a CD is a safe and easy way to invest.3. Invest in Your Retirement Through Work

Interested in tax-advantaged retirement funds that will help you invest in your future? Then look into starting (and fully funding) an IRA, in addition to your 401(k), through your employer. If your employer offers to match contributions toward your 401(k), you should always take advantage of this. Even if you only contribute enough to collect the full employer match, that’s fine; failing to do so is essentially leaving free money on the table, though. Plus, your 401(k) contributions are tax-deductible and will grow over time, providing you with a healthy retirement nest egg for your future. IRAs are also excellent long-term investment vehicles, primarily for the tax benefits. If you open a traditional IRA, your contributions will be tax-deductible up to the annual maximum. If you qualify for a Roth IRA, your contributions won’t be tax-deductible now, but your withdrawals will be when the time comes to utilize those funds. (To learn more about which IRA best suits your needs, check out this article.) Saving for retirement is the second-most-important priority (behind establishing a healthy emergency savings account). Before worrying about building a stock market investment portfolio, be sure that you are setting your older self up for success.4. Utilize an Investment App (Stash)

Ready to dabble in the stock market, but don’t quite know where to start? Or maybe you don’t think that you have enough investable funds to warrant a stock brokerage? Well, then an investment app might be the perfect introduction for you and your money. There are a number of intro-to-investing apps on the market today, but one of our favorites is called Stash. After answering a few questions to determine your investment style (do you want to be super conservative with your money, or risk more in order to potentially make more?), Stash will curate the perfect recommendations for you. To start using Stash, you only need $5, making it one of the most flexible and affordable investment options around. Plus, if your account balance is below $5,000, your monthly service fee for using the app is a single dollar. Yep, for only $1, you can get curated investment options as well as a wealth of advice and resources. This makes Stash truly ideal for beginner investors who don’t really know where to start or aren’t ready for a financial advisor just yet. To read our complete review of Stash and learn more about the app, see our write-up here.5. Robo-Advisors Might Be the Answer

There are a number of robo-advisors on the market today, most of which offer you automated investment options for a reasonable (or even, cheap) price tag. This makes them a great option for beginner or hands-off investors who want their money to grow without constant oversight. Companies like Betterment and Wealthfront offer easy-to-use platforms that make investing as simple as using a savings account. Simply add the money you want to invest (as much or as little as you can afford each month) to your account and watch Betterment work its magic by investing your funds in ETFs (exchange traded funds). Robo-advisors will help you rebalance your portfolio over time, can reinvest your dividends, and will even help you with tax loss harvesting. The fees are a bit higher than you would find if you invested your funds directly with a company like Vanguard, but the added expense may be well-worth it to you for the convenience of a hands-off approach.6. Check Out Peer-to-Peer Lending

Looking for a quick return on your funds, whether you’re investing $25 or $2,500? Then look into peer-to-peer lending. Platforms like Lending Club and Prosper allow approved investors to put up funds in denominations as low as $25. You’ll be able to choose the peer loans that you’re most interested in, lending money directly to borrowers and enjoying return rates ranging from 5% to as high as 33% in some cases. Peer-to-peer (P2P) lending comes with additional risks, but with great risk comes great rewards–namely in the form of interest rates higher than you’re guaranteed to find elsewhere. Investing doesn’t only mean spending tens of thousands of dollars on stocks and building a Wall Street portfolio. It simply means making your money work for you, and you can get started for as little as a few bucks. There are plenty of options to begin building your first portfolio, letting your money earn interest and grow over time. Whether you choose a high-yield savings account or go the high-risk/high-return route of the stock market, the important thing is to start early. How will you start your investment journey, even if it’s only with $100?Investing isn't just for the wealthy. In fact, all you need is a few bucks to get started. Here are 6 ways you can begin investing with just $100.The post 6 Ways You Can Begin Investing with Just $100 appeared first on The Dough Roller.

via Finance Xpress

Before you submit a real estate offer, you should be already preapproved for a mortgage. During good times, being a preapproved buyer improves your odds of beating out other competing offers. During bad times, like during a global pandemic where everyone craves certainty, being preapproved greatly improves your odds of getting a good deal. Let

The post How To Get Preapproved For A Mortgage And Why It’s So Important appeared first on Financial Samurai.

from Financial Samurai

via Finance Xpress

The post Are You a Bad Investor? appeared first on The Dough Roller.

via Finance Xpress

The post Here’s What You Should Do Instead of Panic-Selling appeared first on The Dough Roller.

via Finance Xpress

The post Weekly Market Recap – Week Ending April 24th, 2020 appeared first on The Dough Roller.

via Finance Xpress

Stephen Dubner, the host of Freakonomics Radio, and Angela Duckworth, the psychologist and author of Grit, explore the weird and wonderful ways in which humans behave. In each episode, they take turns asking each other questions, with conversations ranging from friendship and parenting to immortality and whether dogs are better than people. No Stupid Questions premieres May 18th.

Listen and subscribe at Apple Podcasts, Stitcher, or search “No Stupid Questions” in any podcast app.

The post Introducing <em>No Stupid Questions</em> appeared first on Freakonomics.

via Finance Xpress

For the moment, it looks like buying the S&P 500 below 2,400 was a shrewd move. The S&P 500 got down to about 2,237 before aggressively rebounding higher. Every investor can easily sell the stock they bought between 2,237 – 2,400 today for a 17% – 30% gain. Whether you do so or not is

The post Real Estate Buying Strategies During The COVID-19 Pandemic appeared first on Financial Samurai.

from Financial Samurai

via Finance Xpress

The post Here’s What Non-Filers Need to Do to Get Your Stimulus Check appeared first on The Dough Roller.

via Finance Xpress

Would you like to learn how to save for retirement?

Learning how to save for retirement is how you start preparing for your future. It’s necessary if you don’t want to work for the rest of your life or if you want to do amazing things after you quit working, like traveling or trying new hobbies.

Learning how to save for retirement is how you start preparing for your future. It’s necessary if you don’t want to work for the rest of your life or if you want to do amazing things after you quit working, like traveling or trying new hobbies.

I don’t plan on retiring anytime soon, but it’s something I’ve spent a lot of time thinking about and planning for. There are lots of reasons for why you should too, such as:

- You can retire sooner rather than later.

- You won’t have to keep working forever.

- You can lead a good life well after you finish working.

- Compound interest means the earlier you save the more you earn.

- You won’t have to rely on your children or others in order to survive.

But, many people are confused or overwhelmed when it comes to retirement savings and investing.

There are different kinds of retirement accounts, personal finance terms you might be unfamiliar with, and you might feel like you don’t have enough money to start saving.

But, you have to remember that everyone is new to this at some point. Anyone who has already started saving for retirement started where you are today – having a lot of questions about how to save for retirement.

You might even have a lot of questions that you are too embarrassed to ask anyone. However, you shouldn’t be embarrassed or feel bad about not knowing how to start saving for retirement.

Personal finance bloggers and retirement experts all started at the same point as you. No one was born knowing how!

Today, I’m going to try to take the stress out of learning how to save for retirement. I am going to explain some common retirement and investing terms – like what compound interest is, the difference in IRAs, and what a 401(k) is.

I’m also going to answer some of the most common questions about retirement savings. These include topics like how much you should save, and if you should save for retirement or help your kids pay for college.

If you are worried that you don’t have enough to start saving for retirement, I have some great tips to get started.

Learning the answers to these questions now is so important because it can help you live a better life in the future. By preparing now, you can prevent future financial stress, you can reach your goals, and pursue your passions.

And remember, it is never too late to learn how to save for retirement, and it’s very important to do if you don’t want to work for the rest of your life.

Related content on how to save for retirement:

- Why Investing for Retirement is So Important for Women (and How To Do It)

- How This Couple Retired In Their 30s and Now Travel Around The World

- How To Become Rich – It’s More Than Millions In The Bank

- How This Couple Retired at 38 and 41

- How My 401k Loan Cost Me $1 Million Dollars

Below are answers to common questions on how to save for retirement.

What is a 401(k)?

A 401(k) is a type of retirement account that you get through an employer.

It allows you to invest a portion of your paycheck before taxes are taken out, and the amount in your 401(k) can grow tax free until you withdraw. Once you reach retirement and take money out of your 401(k), the amount you withdraw from this account is taxed.

Your 401(k) is an account that holds investments, similar to how your bank account holds your money. You may choose to place investments such as stocks, mutual funds, and more in your 401(k).

What’s a company match? Or employer match?

You’ve probably heard the term “employer match” or “company match.” But, what do they mean?

A company or employer match is when your employer contributes to your 401(k).

For example, an employer may match 100% of your contribution, up to 5% of your salary. So, if you contribute 5% of your salary to your 401(k), then your employer will also match and put 5% in as well.

This is basically free money that will help you grow your retirement savings, and you should take advantage of it if you can!

What is an IRA?

An IRA (Individual Retirement Account) is a type of retirement account that anyone can open, without an employer.

If you do not work for someone else, or if the business you work for does not have a 401(k), then an IRA may be a good option for you.

This is a confusing term and topic for people who want to learn how to save for retirement because there are different types of IRAs, including:

- Traditional IRA – Contributions to this kind of IRA are tax deductible the year they are made.

- SEP IRA – This is a traditional IRA that offers tax breaks for those who are self-employed.

- Roth IRA – This account uses after-tax money, and your withdrawals in retirement are not taxed.

One way people decide between a Roth and traditional IRA is by what their tax rate (this is based on your income) will be like during retirement. If you will be at a higher tax rate, you may want to choose a Roth IRA. If you will be at a lower rate, a traditional IRA might be better.

What is compound interest?

This is a very important question to cover, because it’s something that may motivate you to start saving as much money as you can right now!

Learning how to save for retirement as soon as you can is a great thing, with one of the reasons being because of compound interest.

So, what is compound interest?

Compound interest is when your interest is earning interest. This can turn the amount of money you have saved into a much larger amount years later.

Compound interest is a crazy thing because $100 today will not be worth $100 in the future if you just let it sit under a mattress or in a basic, low interest checking account. However, if you invest through your retirement account, then you may be able to turn your $100 into something more.

When you invest, your money is working for you and growing your savings, and that’s because of compound interest.

For example: If you put $1,000 into a retirement account with an annual 8% return, 40 years later you will have $21,724. If you started with that same $1,000 and put an extra $1,000 in it for the next 40 years at an annual 8% return, that would then turn into $301,505. If you started with $10,000 and put an extra $10,000 in it for the next 40 years at an annual 8% return, that would grow into $3,015,055.

How much money do I need to retire? What percentage of your income should you save for retirement?

This isn’t an easy question to answer, as this will vary from person to person. It depends on your goals, when you want to retire, and what retirement means to you.

However, many people aren’t saving enough for retirement. According to the U.S. Bureau of Economic Analysis, the personal savings rate has averaged around 5% in the past year, and averaged 8.33% from 1959 until 2016.

I’ve talked to a lot of people who think that saving between 1% and 5% of their income is enough to be on track for retirement.

Sadly, saving 5% means it may take you a very long time to retire.

For the average person, I recommend saving at least 20% of your income.

However, there is no perfect percentage.

If you have a high income, then you should probably save more of your income so that you aren’t being wasteful with your money.

On the other hand, if 20% just seems like a crazy high percentage for you to save, then just start somewhere, anywhere! Saving something is better than saving nothing.

And, everyone has different financial goals. If you want to retire early, then you’ll most likely have to save more than 20% of your income.

How much money should you have saved by 30?

Many young people who are learning how to save for retirement ask me this question.

Some advisors recommend that you have an amount equal to your annual salary saved by 30, and others say that you should have half of your annual salary saved by 30.

I think those amounts are great to save by 30, but the problem with those guidelines is that if you haven’t started saving or are much older, you can easily feel like you will never be able to reach retirement.

Those recommendations may be very difficult for many people to follow. You have to be realistic with yourself, and start with small goals that you can build over time. Any amount helps, and it’s never too late to start saving!

What if I can’t save very much money for retirement?

You may be thinking “How much money should I save, if I don’t have much money?!”

Thinking about the above recommendations can be frustrating if you are already having a hard time paying your bills and/or living paycheck to paycheck.

However, I recommend saving as much money as you realistically can. This may be nowhere near 20% at first, heck, this might not even be 5%, but any little bit will help. If you are not able to save that much, just save something! Start with $25 a month if you have to – seriously, every little bit does help.

Even if it’s just $1 a day, set that amount aside and start saving it.

You may want to look into Acorns, which is a cell phone app that rounds up your credit card and debit card purchases, and then invests your spare change. Acorns automatically invests for you, and you can get started in under 5 minutes. This app is amazing!

So, no matter how you are doing right now, just start with something, no matter how small. Then, work your way up until you are saving a percentage of your income that you are happy with.

Start small and work your way towards your savings goal. And, if you are currently paying off debt, keep in mind that it counts too! Once your debt is paid off, you can use that amount towards your retirement savings.

Just keep moving in a positive direction and keep getting closer and closer to reaching your financial goals.

I understand that some people have financial situations in which they may not be able to save as much money as they would like. Living paycheck to paycheck, having lots of medical debt, or having a major unexpected expense can wreck a person’s financial situation and their goals, and I understand that.

However, you will need to find a way out of that if you want to learn how to save for retirement. To find a way out, you may want to find ways to cut your spending, make more money (learn ways to make extra money), and more. You will have to challenge yourself, and it may not be easy. However, it will all be worth it once you reach your financial goals!

By spending less money, you’ll decrease the amount of money you need for the future, including money for emergency funds, retirement, and more.

Just think about it: If you are currently living a frugal lifestyle, then you will be used to living on less in the future. This means that your saved retirement amount doesn’t need to be as large, which means it may be easier to reach that savings goal.

Where do I invest for retirement?

Now we are getting into questions about how to save for retirement that focus on some specific investing questions. And there are two main ways to start investing your money.

Either invest your money yourself, such as through an online brokerage, or find an expert to manage your investment portfolio.

Part of learning how to start investing includes determining the company, platform, or person you will use to invest your first dollar.

There are many online brokers for you to choose from. My favorites include:

- Ally Invest – This is a full service discount broker that doesn’t have a minimum investment amount, so you can start investing with them right away.

- Betterment – Betterment offers an affordable way to invest your money. They have over 400,000 customers and over $14 billion has been invested through their platform. With Betterment, you can invest with as little money as you want each month, which is great for a new investor!

- Vanguard – I absolutely love Vanguard and use them personally, and I recommend that you check them out.

Also, if your employer has a retirement plan, then you will definitely want to look into that as well. If your company offers a retirement plan match, then this is where you will want to start as their retirement match is pretty much free money, as discussed earlier!

What do I invest in?

After you open your brokerage account, you will want to decide how exactly you will invest your money.

I think this might be one of the biggest hurdles for those wondering how to start investing. There are a lot of what ifs in the investment world, and a good brokerage or expert will help you navigate as you decide where to put your money as you learn how to save for retirement.

Basically, where you invest your money depends a lot on the level of risk you are willing to take and the time you have to watch your funds mature. A simple way of explaining this is that more time equals more risk and less time equals less risk.

For example: if you are in your 20’s, you may have many, many years worth of investing ahead of you. You will likely be able to make some riskier investments knowing that the market will bounce up and down over time. If you are closer to retirement, you may want your funds in something that you are confident will make small but steady gains.

Choosing the stocks you invest in is not the easiest thing because no one knows what will happen in the future. This is why it’s important to have a diverse portfolio.

When you are first learning how to save for retirement, you may want to consult an expert to help you determine your goals, your risk level, and how to diversify your investments in a way that will benefit you.

Even if you do have a professional helping you, it’s always important to do your own research on the types of investments available and which ones interest you.

Please remember that I am not an investment professional and that you should do your research when choosing who/what to invest in.

How often should I check on my investments in my retirement portfolio?

After you’ve started investing, you will want to regularly track your investments. This is important because you may eventually have to change where your money is invested, put more money towards your investments, and so on.

Now, the key here is to not go crazy. Checking on your portfolio can be an exciting thing when you first start investing. But, you do not want to become a person who checks their investments every hour of the day. That won’t help you at all. Your investments will make small changes throughout the day, and these likely won’t matter to you, especially if you are investing for your long-term future.

However, you do want to occasionally check your progress as things may change in the market, your investment interests may change, and you may even change your retirement and/or investing goals.

A free tool that I recommend using to monitor your investments is Personal Capital.

You can see your investment portfolio all in one place so that you can easily track your performance, see your investment allocations, and easily analyze everything related to your investments. The Personal Capital Retirement Planner will also tell you if you have saved enough for retirement, which is great when you’re learning how to save for retirement.

Should I risk my retirement and help my children pay for college?

If you are not currently saving enough money for retirement, and you are in jeopardy of not retiring, then I do not recommend risking your retirement to help your children pay for college.

I have personally heard too many real life stories of parents who have $200,000 in student loan debt for their children. These parents have found that these debts are causing them to struggle financially and that they’re unable to reach their retirement goals.

These parents just honestly want to help their children get through college, but they end up drowning in debt. What they don’t realize, though, is that there are other ways to help your kids graduate from college.

I recommend learning more at Parents Paying For College – Is This A Good Idea?

What are the best retirement and investing books?

There are many great investing and retirement books if you want even more about how to save for retirement. These books can clear up any other questions you have, as well as dive deeper into the many different ways to retire.

Here are some of the investing and retirement books that I recommend:

- Work Optional: Retire Early the Non-Penny-Pinching Way

- Broke Millennial Takes On Investing

- Quit Like A Millionaire

- The Simple Path To Wealth

- The Millionaire Next Door

There are many more out there, but these are great books to start with. I have read each of them, and they are all very helpful.

How do I actually start saving for retirement?

Actually getting started can be difficult, so in this section I wanted to list out the steps so you can learn exactly how to save for retirement.

- Start setting aside money for retirement. If you want to learn how to save for retirement, you need to start setting aside money specifically for it. The amount of money you save is entirely up to you, but in general, the more the better. You can take money out of each paycheck, set up direct deposit, etc.

- Research and learn more. I recommend learning more about investing and retirement if you are unsure about anything, such as by reading retirement books, websites, and so on. Sure, it can be easy just to hire someone to do it all for you – but how do you know that they are doing the correct thing to begin with? So, I recommend at the very least having a basic knowledge of everything yourself first.

- Choose a brokerage or someone to manage your investments. Like I said earlier, there are two main ways to invest your money – yourself through a brokerage or you can find someone to manage your investment portfolio for you. You will need to choose one of these options to actually start investing your money. Personally, I like to do everything myself through Vanguard.