The post How Young Investors are Cashing in on Coronavirus Volatility appeared first on The Dough Roller.

via Finance Xpress

The post The Thrifty Parent’s Guide to Crisis Budgeting appeared first on The Dough Roller.

via Finance Xpress

AcreTrader is a proud new sponsor of Financial Samurai. In my quest to continuously learn about new alternative assets and investment platforms, I’ve invited AcreTrader to write a guest post about farmland investing. During times of uncertainty and stock market volatility, it’s nice to invest in real assets. Mark Twain once said, “Buy land. They’re

The post AcreTrader Review: Unprecedented Access To An Overlooked Asset Class appeared first on Financial Samurai.

from Financial Samurai

via Finance Xpress

The post Money Moves to Make in Your 40s appeared first on The Dough Roller.

via Finance Xpress

The post M1 Finance vs. Betterment appeared first on The Dough Roller.

via Finance Xpress

Everyone agrees that massive deforestation is an environmental disaster. But most of the standard solutions — scolding the Brazilians, invoking universal morality — ignore the one solution that might actually work.

Listen and subscribe to our podcast at Apple Podcasts, Stitcher, or elsewhere. Below is a transcript of the episode, edited for readability. For more information on the people and ideas in the episode, see the links at the bottom of this post.

* * *

This is Steve Levitt. Dubner has taken the week off and handed the microphone over to me, and that gives me the chance to investigate something that’s really been troubling me. It seems like ages ago with all that has happened since, but do you remember the headlines back last summer?

ANCHOR: Fires are raging across Brazil’s Amazon rain forest.

ANCHOR: The world’s largest rain forest is being destroyed at an alarming rate.

ANCHOR: Much of the blame is being heaped on Brazil’s far-right President Jair Bolsanaro.

I’d never given much thought to the Amazon rain forest. All the media coverage, though, of the wildfires got me wondering. Is it really true that the Amazon rain forest is being destroyed? Should I be upset about that happening, or is it no big deal? If it is a big deal, is there some way we could save it? Ecologists, environmentalists, and politicians have strong opinions about the answers to those questions. The economics of the Amazon, however, are barely discussed in the public debate. As I soon came to realize, that is a huge mistake. On today’s episode, we will explore the simple economics fueling one of the world’s most dangerous ecological disasters:

Daniel NEPSTAD: It is a great example of a market failure.

The reasons for that failure:

Michael GREENSTONE: You know, you have to put yourself in the shoes of the Brazilians. It’s their forest.

And the remarkably straightforward solution that nobody seems to be talking about:

Gretchen DAILY: My worry is whether we can do this quickly enough.

* * *

The Amazon rain forest covers roughly one-third of South America, stretching across parts of nine different countries, but lying primarily in Brazil. It is by far the world’s largest forest, and it is the home to roughly 10 percent of all the species on the planet. The vast interior is relatively untouched, but deforestation has already shrunk the forest by almost 20 percent, primarily in the Brazilian Amazon, where the great majority of the 30 million people living near the Amazon reside. Daniel Nepstad is an ecologist who’s studied the Amazon rain forest for over 30 years, and has written more than 100 scholarly articles on the subject. I asked him what would happen to the global environment if we woke up tomorrow and the Amazon was gone.

NEPSTAD: The prospect of avoiding the more catastrophic dimensions of climate change would be virtually gone.

Nepstad runs the Earth Innovation Institute.

NEPSTAD: We’re a small nonprofit research and action group with offices in Brazil, Peru, Colombia, Indonesia, on the ground trying to move forward large-scale strategies to solve tropical deforestation as we deliver benefits for Indigenous people and other rural communities.

Nepstad has earned himself a nickname in the field of ecological research:

NEPSTAD: People call me the tree-killing ecologist.

In one experiment, he covered the forest floor with 6,000 plastic panels to find the drought threshold beyond which trees begin to die. In another experiment, he burned hundred-acre plots of forest at different intervals to ascertain the rain forest’s resilience. He is willing to kill some trees along the way because he knows how important preserving the Amazon is for fighting climate change.

NEPSTAD: If we take the 100 billion tons of carbon stored in the trees of the Amazon, that going into the atmosphere is about 400 billion tons of CO2. And that’s 10 years worth of global humanity-wide emissions of CO2.

Any economic discussion of the Amazon has to start with the fact that the amount of carbon stored in the Amazon is truly immense — over 70 times greater than the annual U.S. output of greenhouse gases. Destroying the Amazon and releasing that amount of extra carbon into the atmosphere would utterly swamp everything society has been doing to reduce emissions.

Although it didn’t attract much international attention, between 1970 and 2005, Brazil seemed to be doing everything it could to destroy the forest. Almost one-fifth of the Brazilian Amazon was deforested over that period. On average, an area of forest the size of the state of Connecticut disappeared each year. But in the 2000s, under the guidance of President Lula da Silva, things started to improve:

NEPSTAD: The Brazilian government is really a hero in terms of strategies for slowing deforestation. When President Lula was in his second year in office, he launched a program, a strategy that cut across more than a dozen ministries, including the Central Bank, to basically control deforestation.

The strategy that was implemented was very heavy on sticks and very light on carrots: Sting operations against illegal operators; hundreds of people put in jail, including government officials; fines levied; suspending access to public farm credit in counties that were on the blacklist because of their high deforestation rates. And that was put in place in 2005. By 2012, deforestation had declined almost 80 percent across the entire Brazilian Amazon. Phenomenal success.

A new Brazilian government led by Jair Bolsonaro took office in 2019. Facing an unemployment rate over 12 percent and sluggish economic growth, Bolsonaro made good on his campaign promises to scale back the Amazon protections and regulations put in place in 2005. Deforestation is now back on the rise.

NEPSTAD: This last year, there was a 30-percent increase over the prior year, we’re at about half of the historical average. And so, 20,000 square kilometers of forest tend to fall in pre-2005. We’re now at 10,000 and all signs are that it’s continuing to grow.

Indeed, the New York Times recently reported that deforestation between January and April 2020 was 55 percent greater than the same period in 2019. Covid-19 appears to be contributing to the increase, with law enforcement efforts hobbled by the pandemic. The international community has condemned the rollback of protections — and countries like Germany and Norway have even cut aid payments to Brazil.

It’s easy to understand the backlash, but it’s just as easy to understand why people cut down the forest. The regions in and around the Amazon are among the poorest in Brazil, a relatively poor country to begin with. Cleared land provides an immediate economic benefit to the owner. Land in the Amazon is deforested for a variety of uses, but one particular industry dominates.

NEPSTAD: Cattle ranching is really the way that people use the land. Seventy percent or so of the cleared land of the Amazon is in cattle pasture.

LEVITT: Now, there are 75 million cattle in the Amazon, but it’s really not that great a place to raise cattle from what I understand. Neither the soil, it’s also far away from places where people want to eat beef.

NEPSTAD: The productivity of cattle ranching in the Amazon is notoriously low.

LEVITT: Why are we raising cattle in the Amazon? There’s one Amazon and there’s a million places to raise cattle.

NEPSTAD: It is a great example of a market failure, I think, where converting a 300-ton forest that would have 200 tree species and tons of unknown other species for a weak cattle pasture that will give you maybe 30, 50 kilos of beef a year, is one of the worst tradeoffs, I think, in the world.

While the news coverage of the Amazon fires last summer seemed to suggest they were wild fires, a product of nature, that’s not what Nepstad says.

NEPSTAD: First of all, it wasn’t a severely dry year. So, most of the intact forests were not vulnerable to fire. Second, there were very few reports of fire getting into forests, mostly around the edges. What we were seeing is a big uptick in the amount of chainsaw-deforestation plots being burned.

Those are sections of the forest being first chopped down with chainsaws and then intentionally set on fire to clear land for cattle. For many, the natural reaction has been to protest, to moralize, to blame the Brazilian government. Those are all reasonable reactions. But, the fact is that the people doing the burning are mostly decent people trying to scratch out a living, responding to the incentives given to them. If we want to solve the problem, we need to change those incentives. And who better to think about that challenge than an economist?

GREENSTONE: I’m Michael Greenstone I was a chief economist for the Council of Economic Advisors in the first year of the Obama administration.

Greenstone is now back as my colleague at the University of Chicago, but while he was in government, one of his jobs was coming up with environmental regulations.

GREENSTONE: And the trick of doing things through regulations is that they have to go through a cost-benefit analysis, and any regulation that reduces carbon is going to have some costs as can be measured in dollars. And it’s going to have some benefits, which are going to be measured in CO2. Dollars are always going to beat CO2 because people don’t know what CO2 is. And so my idea, which I started with my friend Cass Sunstein, was to come up with a unified number called the social cost of carbon for the U.S. government. And that was a way to monetize the damages of the release of an additional ton of CO2.

LEVITT: Before you went to create that number, how did the U.S. government think about the social cost of carbon?

GREENSTONE: It was completely incoherent. You had some agencies, let’s call them agencies that shall remain nameless but maybe think there should be more transportation in the world, thought that the cost should be effectively $1, $2 per ton of CO2. Yet other agencies who thought that the environment was their mission, and they thought it was basically infinity.

To determine where between $1 per ton and infinity the cost of carbon was, Greenstone relied on what economists call integrated assessment models, I.A.M.’s.

GREENSTONE: And they are very high-level models that basically go from a puff of CO2 into the air to how that’s going to affect the atmospheric concentrations of CO2, to how that’s going to affect temperature, to how that’s going to affect economic activity and human well-being. Those models were almost all developed in the 1990s when computers were not very good and we didn’t have access to a lot of data. And so they by necessity were very assumption-driven.

What has happened since then has been an explosion in computing power and an explosion in access to data. And we’re now beginning to be able to build an empirical foundation for what the damages of climate change might look like. I think probably the average outcome is that it’s going to be painful and cause damages and we’ll learn to adapt from them. But there’s a pretty wide set of unknowns, and buried in those unknowns are some things that would be much worse.

One key metric used by economists to measure the negative consequences of climate change is the number of “90-degree days” per year. A “90-degree day” is a day where the average of that day’s high and low temperature is at least 90 degrees. That is roughly the temperature level that turns out to be dangerous for both people and crops. But how dangerous? That depends on where you live:

GREENSTONE: If you’re sitting in the United States — higher temperatures, we’ve got really good systems in place to deal with them. India is really, like, ground zero for climate damages, I think, because it’s relatively poor, it’s not easy for them to protect themselves. Further temperature increases there would have big impacts on crop yields, big impacts on health. Some of my own research suggests that without adaptation, an extra “90-degree day” in India will kill 20 times as many people as it does in the U.S., precisely because they’re relatively poor and not well-equipped to handle it.

A key decision that Greenstone faced when trying to quantify the social cost of carbon was whether to consider only the impact on Americans or to take into account the global impact.

GREENSTONE: There’s something intuitively appealing about not counting damages that occur outside the United States. And many people have that reaction. My view, and ultimately our judgment was that since CO2, wherever it’s released, has impacts around the planet, we cared about other countries reducing emissions as well. And so that in a kind of international negotiation sense, every time we reduce a ton of CO2, we’re providing benefits for the Chinese and Indians. But every time they reduce a ton of CO2, they’re producing benefits for us. And so, the idea was by using a global value, you could induce reactions that would reduce emissions, that would benefit people in the U.S.

Taking all of these variables into account, Greenstone and his team concluded that the social cost of carbon is $50 per ton of CO2.

GREENSTONE: The average man, woman, and child in the United States emits about 16 metric tons of CO2 per year. So, you could think of yourself, or the average person, as doing about $800 of climate damages per year.

Greenstone’s hope was that putting a price on carbon, and ensuring that the price had legitimacy, would lead to more thoughtful policy, although this hasn’t been 100 percent successful.

GREENSTONE: In some sense, climate change is a super boring economics problem, in that it’s very easy to figure out what to do globally. That is, you should set a price on carbon, and then you should fund R&D in green energy. Super easy. Those turn out to be pretty politically challenging to do. And so effectively, in the U.S., what we’ve been doing are a bunch of kind of mandate-style policies that aim for reductions in particular places in the economy.

Regulations on auto emissions, for instance. Another politically popular policy is what’s known as an offset:

GREENSTONE: An offset is that I — the state of California, or some institution, U. Chicago, or Goldman Sachs — would like to reduce my carbon footprint. And I could do that by reducing my own carbon emissions. Or I could scour the planet and find someone, somewhere else, some person or some institution, who could reduce their carbon emissions by whatever amount I wanted to. And I would just pay them for that.

LEVITT: And how have offsets worked in practice, according to the research?

GREENSTONE: I think to date, the story of offsets has been very disappointing. And the reason is it’s been very difficult to monitor them and very difficult to verify that the claimed reductions in CO2 actually happened or that they were additional.

For economists, this disappointing result is pretty unsurprising. Imagine that I pay a cement manufacturer not to make cement. As long as the demand for cement remains unchanged, that production of cement just shifts to another manufacturer, and in the end, nothing has really changed. If the use of offsets hasn’t proven very effective, what about the strategy of just telling people they should use less carbon?

GREENSTONE: When you tell people you should just use less carbon, I think what you’re doing is, you’re sliding into making it a moral issue. And once it’s a moral issue, it’s very murky waters. One number that gets stuck in my head, as I do a lot of research in the state of Bihar, in India: per capita electricity consumption there on an annual basis is about 270 kilowatt hours per person per year. That’s like running two 60-watt bulbs six hours a day.

In the United States, it’s like 13,000 kilowatt hours per person per year. If you’re sitting in Bihar, it’s a totally unacceptable situation to have that level of electricity. And have to improve their lives and electricity allows them to do that. Trying to express this as a moral issue to them, the moral issue to them is that they are at 270 kilowatt hours per person. If you really want to talk about morals, think about Bihar.

Or think about Brazil. To the poor farmer in the Amazon it isn’t about morality, it is about survival. This is one particular case in which we don’t need moral arguments because the economic arguments are so, overwhelmingly persuasive. A hectare of Amazon land cleared for raising cattle — a hectare is just under two-and-a-half acres — sells for less than $1,000. With a social cost of carbon of $50 per ton of CO2 and the current best estimates of the carbon stored in the Amazon, each hectare of land preserved as forest is worth over $28,000 based on the carbon alone. That isn’t even putting a value on biodiversity or tourism. When land is worth almost 30 times more — to all of humankind — as forest, but instead people cut it down to grow cattle, that is the absolute definition of a market failure. A market failure with a very straightforward remedy.

GREENSTONE: There is a strong economic case for the world subsidizing the protection of the Amazon.

* * *

LEVITT: You, as an ecologist, become friends with economists and have learned to think in many ways like an economist, but that can’t be a very popular stance among ecologists more generally, is it?

DAILY: Well, things are changing.

That’s the ecologist Gretchen Daily:

DAILY: Initially, people thought teaming up with economists was sort of selling out. But now people are getting more sophisticated in their thinking on the science side of things and recognizing that economics has incredibly powerful ways of understanding why people make the choices they do.

Daily works at Stanford.

DAILY: I’m a professor in biology. And I’ve long been brainwashed by people in economics and feel there’s so much potential in working together to begin to capture the values of nature in our minds, on our balance sheets.

At Stanford, Daily is co-founder and director of the Natural Capital Project.

DAILY: Natural capital is a dry-sounding term, but it’s basically Earth’s lands, waters, and the biodiversity, all the life. We don’t think much about natural capital. We pay a lot of attention to financial capital that sort of keeps everything flowing.

LEVITT: And your point is that there’s other inputs into our economy. And one of those is nature. And the term natural capital is designed to integrate into our economic thinking the role that nature is playing in how the economy functions not only today, but also in the future.

DAILY: That’s exactly right. Basically, historically, we’ve recognized the scarcity often and value of these other forms of capital and the immense payoff from investing in them. And it’s just now that we’re starting to recognize the scarcity of natural capital.

The modern metric for calculating the health of a country’s economy is gross domestic product— and it’s traditionally been based solely on the market value of all the goods and services produced in a country over a period of time. Daily and her team want to extend that notion to encompass environmental factors, what they have termed gross ecosystem product, or G.E.P.

DAILY: What’s really motivated development of G.E.P. is recognition that we’re really in the great degradation of natural capital. It was during the Great Depression that G.D.P. was developed. And nowadays it’s the great degradation of natural capital that is driving development of G.E.P. So, G.E.P. was actually called for by leadership in China, where they recognized that even with all the success they’d had and highest G.D.P. growth rates in the world and lifting so many millions of people out of poverty more successfully than any other country has done, that actually it came at this devastating cost.

According to the E.P.A., China is responsible for 30 percent of the world’s CO2 emissions and is the world’s biggest source of CO2 by a wide margin. The U.S., at 15 percent, is No. 2. Air and water pollution are estimated to cause over 1.5 million premature deaths per year in China.

DAILY: One of the main catalysts for China was the biblical-scale flooding that happened in 1998. It was traced to dramatic deforestation that had occurred over some years before in the upper reaches of the Yangtze River system, and that deforestation made downstream people much more vulnerable to devastating flooding. And the reason is that forests are like a sponge. But in 1998, the deforestation had been really extensive. The rains were much heavier than usual and that just spelled disaster and millions of people were affected.

The total costs were estimated at a lower bound at about $35 billion. And rapidly — as China is noted for making rapid responses — the government called for all the evidence and a systematic understanding of the situation and said, “Okay, there’s only one way out of this. There’s no way we can substitute using physical infrastructure for all the flood-control services that the Yangtze River provides to hundreds of millions of people downstream. We have to restore that forest.” And they launched the biggest reforestation program that Earth has ever seen, paying about 120 million households to protect existing forest or restore forest and the payments over the past decade or so have amounted to about $150 billion.

China’s “Grain for Green” program has been ongoing since 1999.

DAILY: The payouts are relatively small on a per-capita basis. But for a small amount of money per capita, there’s been a massive increase in flood security.

The program has seen large successes: Daily found that a decade after the program was implemented and millions of hectares were reforested, there were improvements in soil retention, carbon sequestration, flood mitigation, and even sandstorm prevention. But China was not the first country to come to the conclusion that a cheap, effective way to preserve a threatened ecosystem was to simply make payouts:

DAILY: Costa Rica had a deforestation rate of over 4 percent per year through multilateral development banks, really incentivizing conversion of forest to farmland and pasture. So, recognizing all that, leaders in Costa Rica decided to put a price on rain forest.

That was in 1996.

DAILY: And it was basically the first time that was done in policy and finance. And what they launched was a payment system, the first ever at a country scale where they said if you protect or restore rain forest on your property, we’ll pay you. And the payments were pretty low, but it was amazing. They were about, I think, $50 per hectare or roughly $20 per acre per year. And that payment was enough to really slow and actually reverse deforestation rates.

So, what should we do about the Amazon? As you think about deforestation, especially if you are making moral arguments against it, you shouldn’t forget about the not-too-distant past. Daniel Nepstad again:

NEPSTAD: Every developed country in the world, maybe with the exception of the northern countries that have huge areas of boreal forest like Canada and Russia, has basically pushed their forest, whittled them down to very small areas, and then put boundaries around parks and protected areas.

Take the Northeastern U.S. as a small-scale example: At one point in our history, forest cover had shrunk by as much as 90 percent compared to pre-colonial times, though much of that has now been reforested.

NEPSTAD: And that is not lost at all on Brazilians. Some folks feel like no matter what Brazil does, there will always be international criticism. If you look at the Amazon, more than half of the remaining forests of the Amazon are in some form of protection — parks or reserves or Indigenous territories. You know, there’s a frustration that whatever Brazil does, it’s never enough.

GREENSTONE: I think an enormous off ramp for being effective in dealing with the climate change problem is veering onto the moral lane.

The economist Michael Greenstone, again:

GREENSTONE: And you have to put yourself in the shoes of the Brazilians. It’s their forest. It should be a good deal for them if they’re going to do it. And the moral part is just — the Brazilian morals about Brazil’s forest are very different than the Norwegians’ morals about Brazil’s forest. And I think that off ramp just goes nowhere in the end.

NEPSTAD: There is this concern in Brazil, and it’s not ubiquitous, that there is an international plot to take over the Amazon. And that resurfaces every now and then. You know, there was a document produced in the United States called “Farms Here, Forest There.”

It is easy to see how Brazilians could become paranoid. One passage from the document Nepstad mentioned reads: “The U.S. agriculture and forest-products industries stand to benefit financially from conservation of tropical forests through climate policy. Ending deforestation through incentives in the United States and international climate action would boost U.S. agricultural revenue by an estimated $190 to $270 billion between 2012 and 2030.” When Brazilian farmers stop farming, U.S. farmers benefit. That is supply and demand in action.

NEPSTAD: It was a well-intended document, but it fueled this conspiracy theory that’s attached to a sovereignty argument, a sovereignty concern. You know, if Brazil owns two-thirds of the Amazon forest, it’s up to Brazil to do what it wants with it. So, that’s one dimension of it. Another dimension really is it’s an amazingly inexpensive venture to think of paying off all of those landholders in Brazil for the foregone profits from converting forests to cattle. And the key would be to have a real financial proposition on the table that compensates Brazilian farmers and compensates Brazil.

Despite all the political bluster about infringement on its sovereignty, the Brazilian government has actually signaled its willingness to trade preservation of the Amazon for cash from other countries. In an interview with the Financial Times, Brazil’s Minister of the Environment Ricardo Salles said, “The opportunity cost must be paid by someone, and … someone means those who have the funds or the necessary sources of finance for that.” He estimated the cost to be $120 per hectare, or about $12 billion a year.

By my calculations, from a purely economic perspective, Brazil should be willing to stop deforestation for $1 to 2 billion per year. The rich nations of the world should be willing to pay up to $40 billion. That is a lot of room for bargaining, and the $12 billion number that the Brazilian minister threw out doesn’t seem crazy. The presumptive Democratic nominee for president, Joe Biden, brought up the idea in a debate with Bernie Sanders:

Joe BIDEN: I would be right now organizing the hemisphere and the world to provide $20 billion for the Amazon, for Brazil no longer to burn the Amazon.

However, Biden makes no mention of such a policy on his campaign site, nor does he propose a plan for how such a payment would work. One country, Norway, has already shown a willingness to pay to try to preserve the Amazon, providing roughly $100 million per year for more than a decade to support a non-profit dedicated to reducing Amazon deforestation. After the fires last summer, however, even Norway stopped contributing. I asked Gretchen Daily about the viability of other countries paying Brazil to stop deforestation.

DAILY: There is a big question as to whether these approaches to valuing nature and especially to paying people to protect or restore nature, whether they can be scaled up and implemented, especially across country boundaries. Countries worldwide should be investing. It would pay off economically to do so. But how realistic is that? I would say at one level, if we had ample time that this movement is going to keep going and growing. My worry is whether we can do this quickly enough. And I think that’s the general worry, that we’re really in a race. We don’t have very much time.

GREENSTONE: I may never go to the Arctic and see a polar bear and I may never go to the Amazon, but I feel good that they exist. And it’s not just that I feel good. I’d be willing to pay something for it. And that is like an adder to the instrumental value of the Amazon. The value of preserving the Amazon is large enough that it should be easy to pay off the ranchers and still preserve the Amazon.

* * *

Freakonomics Radio is produced by Stitcher and Dubner Productions. This episode was produced by Zack Lapinski. Our staff also includes Alison Craiglow, Greg Rippin, Matt Hickey, Corinne Wallace, Daphne Chen, and Mary Diduch. Our intern is Emma Tyrrell; we had help this week from James Foster. Our theme song is “Mr. Fortune,” by the Hitchhikers; all the other music was composed by Luis Guerra. You can subscribe to Freakonomics Radio on Apple Podcasts, Stitcher, or wherever you get your podcasts.

Here’s where you can learn more about the people and ideas in this episode:

SOURCES

- Steve Levitt, co-author of the Freakonomics series and economics professor at the University of Chicago.

- Daniel Nepstad, president and founder of the Earth Innovation Institute.

- Michael Greenstone, former chief economist for the Council of Economic Advisors and economics professor at the University of Chicago.

- Gretchen Daily, environmental science professor at Stanford University.

RESOURCES

- “The true cost of carbon pollution,” by the Environmental Defense Fund (Environmental Defense Fund, 2020).

- “CO₂ and Greenhouse Gas Emissions,” by Hannah Ritchie and Max Roser (Our World Data, 2019).

- “Impacts of China’s Grain for Green Program on Migration and Household Income,” by Paul Treacy, Pamela Jagger, Conghe Song, Qi Zhang, and Richard E Bilsborrow (Environ Manage, 2018).

- “China cuts smog but health damage already done: study,” by David Stanway (Reuters, 2018).

- “Farms Here, Forests There: Tropical Deforestation and U.S. Competitiveness in Agriculture and Timber,” by Shari Friedman, David Gardiner & Associates (2010).

- “Cattle Ranching in the Amazon Rainforest,” by J. B. Veiga, J.F. Tourrand, R. Poccard-Chapuis, and M.G. Piketty (XII World Forestry Congress, 2003).

EXTRA

- Changes in the Land: Indians, Colonists, and the Ecology of New England, by William Cronon.

The post The Simple Economics of Saving the Amazon Rain Forest (Ep. 428) appeared first on Freakonomics.

via Finance Xpress

The post Second Stimulus Update and What to Watch For This Week appeared first on The Dough Roller.

via Finance Xpress

The post How to Get a Deal on a Foreclosed Home appeared first on The Dough Roller.

via Finance Xpress

The best home buying rule I can offer you is my 30/30/3 home-buying rule. If you follow my home buying rule, you will have a greater chance of surviving any financial downturn. If you follow my 30/30/3 home-buying rule, you will also be able to enjoy your property more because you will be less stressed

The post The 30/30/3 Home-Buying Rule To Follow appeared first on Financial Samurai.

from Financial Samurai

via Finance Xpress

The post Best Fractional Share Investing Brokerages appeared first on The Dough Roller.

via Finance Xpress

As soon as your real estate offer gets accepted, you notify your lender with the relevant ratification documents and lock in a rate. The rate lock is usually for 30 days. However, sometimes things take longer than expected and you need to get a mortgage interest rate extension. A mortgage interest rate extension is also

The post Mortgage Interest Rate Extension: The Cost And Why You Might Need One appeared first on Financial Samurai.

from Financial Samurai

via Finance Xpress

Yotta Savings App Review – Win up to $10 million weekly by saving in an FDIC insured account

4:23 AMI recently came across an interesting new savings account, and I am excited to share it with you all today.

I think you’ll want to hear about this as it’s such an interesting and new concept.

Here’s a quick overview of the new savings app that gives you the opportunity to win $10,000,000 every single week.

Yotta Savings uses the psychology that drives Americans to play the lottery to instead motivate Americans to save money.

For every $25 that you save with Yotta, you have the chance to win $0.10 all the way up to $10,000,000, every week.

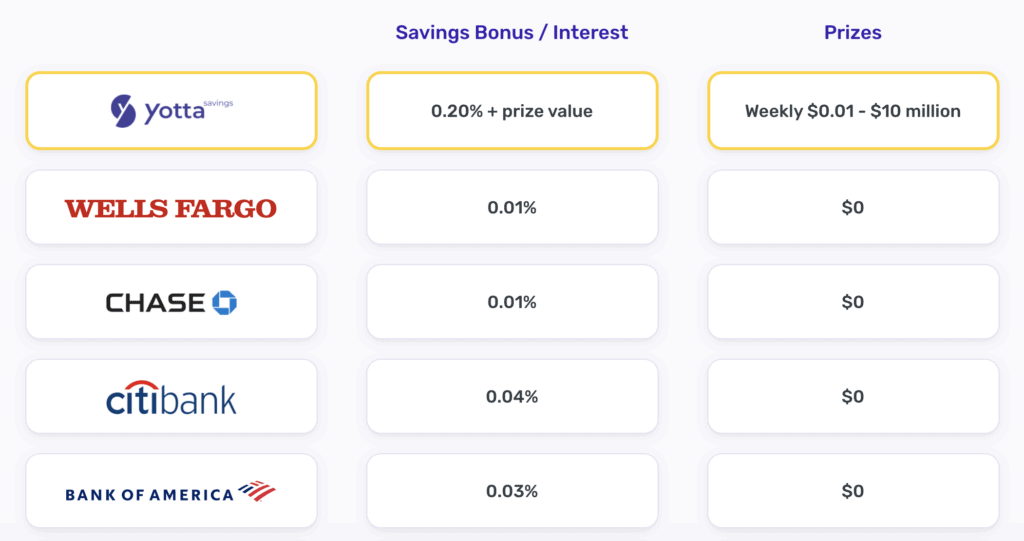

And, if you don’t win, your cash that you’ve saved still has a 0.20% savings rate, which is twice as high as the national average.

The creators of Yotta built this savings app to help Americans meet their savings goals. This is especially important because according to the Federal Reserve, 40% of Americans do not have $400 for an emergency. However, even though that is a crazy statistic, Americans still spend $80 billion on the lottery every year, which averages out to $640 per U.S. household.

This is a lot of money spent on the lottery, instead of saving money. But, I can understand the mindset. This is where Yotta comes in. Yotta makes saving fun and provides rewards for saving, which many people need the motivation for.

The creators of Yotta Savings were inspired by Premium Bonds in the UK, where 23,000,000 people use savings products to win prizes as well. It’s a similar product to Yotta Savings with over $100 billion in deposits.

You can click here to download Yotta.

If you use my code MICHELLE, then you will get 100 free tickets into the next week’s drawing.

Here’s my Yotta Savings review.

How does the Yotta Savings app work?

After reading all of the above about Yotta Savings, I’m sure you are interested in how exactly the savings app works.

Using Yotta is easy. You start by:

- Making a deposit. You select your bank to make a deposit from and for every $25 that you save, you get a ticket into weekly number draws. So, if you deposit $100, then you get 4 tickets every week for as long as you keep that $100 in your account without needing to make any new deposits.

- Every Monday, you pick 7 numbers for each of your tickets. If you don’t pick numbers, that’s fine as well – your ticket will be automatically picked if you don’t complete it in time.

- Contests are done weekly, with one number drawn every night at 9pm ET. On Sunday, the final number is drawn and winnings for the week are made.

- Finally, you can win up to $10,000,000. The more numbers you match, then the more money you win. If you match all 7 numbers with the numbers that are drawn, then you win the $10,000,000 jackpot.

What’s great about Yotta is that your savings still grow at a rate of 0.20%. If you include the value of prizes where they’re currently set, you get over 3% all-in on your savings, which is the highest rate that I have seen.

That is twice as much as traditional banks, plus you can set aside money in a separate account and play their contest with no risk.

Here’s an image that shows what savings accounts usually pay when it comes to interest.

Is Yotta Savings legit?

Yotta is completely free.

There are no minimums, no monthly fees, so there is no risk.

You can save money in their savings account, plus have the chance to win drawings.

Other positives of the Yotta Savings App:

- Your savings account is FDIC insured and held at Evolve Bank & Trust, a bank that has been around for over 90 years.

- FDIC insurance means your cash is fully guaranteed by the U.S government for up to $250,000.

- Your account is protected by bank-grade encryption and authentication.

How do I sign up for Yotta Savings?

Signing up is easy:

- You can click here to sign up for Yotta Savings, and all you need to sign up is your name and email address.

- If you use my Yotta referral code MICHELLE, then you will get 100 free tickets into the next week’s contest.

- To earn tickets to their weekly prize draws, you will have to connect a bank account and make a deposit.

Yotta Savings Reviews

I did a lot of research on Yotta Savings, and you can find reviews from real customers at:

The reviews were almost entirely positive (except for one person who had a small technical difficulty), so I would say that this savings app is definitely something more people should check out.

I know that I am personally excited to try it out. While I don’t play the lottery, it is easy to get tickets just due to keeping money in this savings account, which is super easy!

The Yotta Savings App definitely makes saving money more fun.

The Yotta Savings email address is support@withyotta.com in case you have any other questions.

What do you think of Yotta Savings? What questions do you have about Yotta Savings?

The post Yotta Savings App Review – Win up to $10 million weekly by saving in an FDIC insured account appeared first on Making Sense Of Cents.

from Making Sense Of Cents

via Finance Xpress

The post This is How Much Your Lifestyle Should Cost appeared first on The Dough Roller.

via Finance Xpress

Also: why do we habituate to life’s greatest pleasures?

* * *

Relevant References & Research

Question #1: Is it possible to be both self-interested and altruistic at the same time?

- Stephen references Jonas Salk as an example of someone who was both selfish and prosocial. Salk was a medical researcher who developed one of the first successful polio vaccines. The biography that Stephen mentions is Jonas Salk: A Life by Charlotte DeCroes Jacobs.

- Stephen and Angela discuss the work of Adam Smith — the founder of classical economics and author of the 1759 book The Theory of Moral Sentiments. Russ Roberts explores some of the misunderstood aspects of Smith’s philosophy in his book How Adam Smith Can Change Your Life.

- Stephen and Angela refer to the warm-glow theory of altruism — an economic theory about the emotional reward of charitable giving.

- Stephen mentions Hillel the Elder, the Jewish sage and namesake of Hillel International. You can read more about the life of Hillel in Joseph Telushkin’s book Hillel: If Not Now, When?

- Angela talks about her once-ongoing debate with psychologist and Wharton professor Adam Grant. You can learn more about Grant’s perspective on giving in his 2016 TED Talk. Grant was also featured in Freakonomics Radio Ep. 152 “Everybody Gossips (and That’s a Good Thing)” and Ep. 306 “How to Launch a Behavior-Change Revolution.”

- Angela brings up the psychologist Jerry Kagan and his research on the moral development of children. You can read more of his work on this topic here.

- Angela mentions the Schwartz Values Survey, a method of measuring human beliefs and principles based on Shalom H. Schwartz’s theory of basic values.

Question #2: Why do we habituate to life’s greatest pleasures?

- Angela and Stephen discuss Danny Kahneman’s famous study on colonoscopy-related pain perception. You can learn more about the study here.

- Angela references the “Three Good Things” exercise, a positive psychology technique designed to inspire gratitude.

- Angela discusses the origins of habituation literature — to learn more about how this theory was developed, we recommend checking out this article on the history of habituation research.

- Angela references the late psychologist Robert Rescorla, one of the world’s most distinguished scholars of psychology and animal learning.

The post Are Ambitious People Inherently Selfish? (NSQ Ep. 11) appeared first on Freakonomics.

via Finance Xpress

Right before the pandemic began, I did a fun podcast interview with Andy from Marriage Kids & Money, a work-from-home solopreneur. It was nice to connect with another father of two young children in the online world. Andy took a leap of faith at a very similar age as me in 2012. Although my main

The post Work-From-Home Solopreneur: How I Made The Leap As A Young Father appeared first on Financial Samurai.

from Financial Samurai

via Finance Xpress

In the good old days, several friends and I liked having beers after each softball game. We got to discussing what is the one ingredient necessary for achieving financial independence at a relatively early age. Here were some of their responses: Saving aggressively Investing in stocks Investing in real estate Earning side income Taking bigger risks

The post The One Ingredient Necessary For Achieving Financial Independence appeared first on Financial Samurai.

from Financial Samurai

via Finance Xpress

Hello! Here is a guest post from Melissa Brock about her decision on whether or not to pay off her mortgage. Melissa is the Money editor at Benzinga and founder of collegemoneytips.com. Enjoy!

My husband and I like to make excellent financial decisions. He says I’m obsessed with our finances — which is kind of true. I mean, I listen to the “Afford Anything” podcast and read every personal finance related piece of content I can get my scroll-happy finger on. I’m also the Money editor at Benzinga for my full-time job. (Okay, okay, he’s right.)

My husband and I like to make excellent financial decisions. He says I’m obsessed with our finances — which is kind of true. I mean, I listen to the “Afford Anything” podcast and read every personal finance related piece of content I can get my scroll-happy finger on. I’m also the Money editor at Benzinga for my full-time job. (Okay, okay, he’s right.)

Our mortgage is a source of well… pain, for me, if you want to know the truth. All the reading I do probably contributes to that. One day, I’ll read an expert post about how so-and-so plans to invest like crazy, pay the minimum on his mortgage, then run, giggling, toward retirement (early!) and revel in the spoils of compound interest.

This person might say, “Why would you pump money into a non-liquid asset?”

And so my mind goes, “Yeah! That makes sense.”

But then I get this nagging feeling — and I know what it is. It’s the oodles of money we’d save if we paid off our mortgage once and for all. Dozens of other experts tout, “There’s nothing wrong with getting out of debt forever… ever… ever…” (Added echoey reverb for fun.)

So I reach into my back pocket and pick up my phone to ask my parents’ advice, and that matters to me, too. I know which way they’d vote. I think my dad even made extra trips to the bank when he had any bit of extra money in his pocket — he wanted his mortgage gone. (This was actually smart because interest rates were sky-high in the 1980s.)

After lots and lots of discussions (sometimes I exhaust my husband), I’ll lay out what we decided to do.

Related content:

- How I Paid Off My $400,000 Mortgage In 7.5 Years, Before I Was 32

- How We Paid Off Our $223,000 House By The Time We Were 30 (Yes, We Have Kids!)

- How We Paid off $266,329.01 in 33 Months

- How Our Family of 5 Went from House Poor to Debt Free in 3 Years

Our story

My husband and I had our 10-year plan mapped out soon after we got married — we’re both firstborn planner-types. (Kind of annoying, if you really think about it.)

We put on paper exactly what we wanted to accomplish over the course of 10 years.

We added “save to build a house” to our list. I really, really wanted a brand-new home because it ensured we could get what we wanted the first time around. I wasn’t interested in knocking down walls to make a decent-sized living room, decimating wood paneling or ripping up old carpet. I didn’t want a fixer-upper — I wanted one that had bedrooms for our two kids and a guest bedroom for family and friends.

I’d bought a tiny split foyer house when I was 24, and I’m glad I did because it helped make our dream a reality. We welcomed a puppy to the Little House on Skenk Street (no, I’m not kidding, that was the name of our street!) and it had begun to feel too small by the time we added our daughter, son and a cat named Hank. We were outgrowing our home. So, the plan was good because we had to do something about our tightening quarters.

Thankfully, we’d put that plan into place and had been saving to build for eight years. We’d amassed a sizable nest egg, too — that was important because building a home is super expensive.

I insisted on real stone (my pick), a decorative wood-burning fireplace (my husband’s real love) — all set on three acres of land.

The bank said, “Sure!” — now, I know that just because a bank is willing to lend you a certain amount, that doesn’t mean it’s the amount you should borrow. In fact, I realize we arguably did the opposite of what every financial professional suggests. The experts crow, “Buy a modest home! Spend no more than 25% of your take-home income on your mortgage payment!”

I confess, I never did do an actual comparison of what our mortgage amount would be to our income. This was before I’d really solidified my personal investment philosophy. Would I have done some things differently?

Actually, in hindsight… no. I absolutely love this house! And fortunately, we live in the Midwest, which works in our favor. Had we lived in California or New York on our current salaries, we’d never have been able to afford it.

I wasn’t making much money at the time as an admission counselor at my alma mater. I talked to families daily about financial aid and paying for college, so when our mortgage amount doubled, I started freelancing. Writing is my first love, anyway, and I was able to side hustle my way toward some great opportunities. In a way, I’m so grateful for this Craftsman-style behemoth for helping me pursue some other avenues.

Anyway, the bank said, ”Yes!” and the builder built it and there we were, left with a new house in a muddy pit (do you even understand how long it takes for grass to grow?!?) and a new mortgage payment. We moved in on an icy day in December (I slipped going up the ramp to the moving trailer) and we kept on going with our lives.

The only real difference was the admiring look back we’d give our new house as we drove down the lane on our slightly longer commute to work. The best part of building it was that it gave us tons more room to move around.

Weighing the pros and cons of paying off our mortgage

At first, neither of us really spoke a word about the mortgage.

It was just there, whisking money from our bank accounts on the fifth day of every month. Whoosh! Gone. We went about our lives with no new 10-year plan. We’d pretty much gotten to the end of the 10-year plan after we’d accomplished what was in the original 10-year plan.

I definitely believe we were in a lull — a “What’s next in our lives?” lull. Then, suddenly, one day, I went on a question-seeking rampage.

“Where are we going in life? What do we want out of life? OHMYGOSH, where should we retire?” AND — “WHAT SHOULD WE DO ABOUT THE MORTGAGE?”

My poor husband.

He’s probably in a constant bewildered state. I frantically researched every expert’s advice. (They all provided conflicting advice.) I asked everyone I knew. (They all provided conflicting advice.)

I waffled back and forth on this for months — and for a short stint, I was absolutely convinced that for peace of mind, we should chuck everything we had at the mortgage. Then I changed my mind. Short of checking myself into therapy over this, we decided to weigh the pros and cons.

Pros to paying off the mortgage

Here’s our official list of pros in favor of committing all our extra money toward paying off the mortgage:

- We’d free up cash flow that would otherwise be used to make a mortgage payment each month.

- We’d be debt free. For life. From all debts. Forever. (Man, oh, man, there’s nothing wrong with being debt free.)

- It feels good. We’d achieve peace if we paid off the mortgage ahead of time, especially before retirement.

- We’d have the mortgage paid off before our kids headed off to college — so we could dole out money for that, right?

- The interest we’d save! Oh, my land! The zeroes never seemed to end. We would save thousands upon thousands of dollars in interest if we worked diligently to pay it off.

Related: Is Paying Off Your Debt Worth It?

Cons to paying off the mortgage

Next, we made a list of cons that would help us determine whether committing a full-on assault toward the mortgage would be a bad idea:

- Lots of cash would be tied up in the house — a non-liquid asset.

- Our interest rate is low — and the annualized return for the S&P 500 is roughly 10% over the last 90 years. We’d be missing out on higher returns if all of our efforts were put into paying off the house.

- We’d no longer be eligible for a mortgage interest tax deduction.

- We’re never planning to sell, but we realized that if the slim chance ever existed, it might be harder for us to sell quickly if we needed to get a very specific amount out of the home.

So, that was our list. I’m positive that there are more pros and cons that could be added to it, but those were the overarching themes that stood out to us and our personal situation.

Talking with the pros

My husband and I have largely been proactive about making our own decisions regarding money. That said, from time to time, we’ve reached out to a financial advisor for sparks of advice. I also got in contact with Vanguard about this very issue just to get another perspective on what an advisor from a huge firm would suggest.

Both professionals’ advice was the same: “Invest in the market!”

It probably reverberated for my husband right then and there. He was all for investing, saving for college for our kids and building up our liquid assets.

I was the roadblock.

I was still waffling because of some deep-seated need to be debt-free for life. (Probably due to the Recession and aftermath of COVID-19 and the possible “What-ifs.” What if one of us lost a job? What if both of us lost our jobs? We’d still have to pay the mortgage. There’s a reason a lot of individuals stated, post-Recession, that debt is still debt, whether it’s good debt or bad debt.

So, again, I was waffling. At one point, I even said, “Okay, let’s just invest.” And then I took back my words a week later. (I’m terribly indecisive.)

At this point, my husband was starting to feel a teensy bit frustrated. I knew I needed to stamp my foot in the ground and stand by a decision.

Our final decision

So what did we decide to do? Well, we actually opted for a hybrid approach. We decided to invest and pay an added amount each month — with the promise that we’d build up liquidity to pay off the mortgage in the future.

- We increased our mortgage payment amount and put it toward our principal. Now, this is key. Directing it toward the principal is the only way to see it decrease faster. We rounded our payment up to the nearest thousand. We are not dedicating all of our excess money toward the mortgage. The penny pincher in me doesn’t like the idea of losing so much through interest, so that’s why some extra will be allocated toward the principal.

- We invested in the stock market. We wanted to make sure our money wasn’t locked up. We have kids who need to go to college someday and retirement to save for. There are a lot of buckets and we knew we’d need to allocate as much as possible to every bucket.

- We have a plan for payoff — down the road. We’ll keep peeking at our liquid assets and determine when the time will be right to start paying off the mortgage in chunks (or in one fell swoop, which would be totally exciting!)

- In addition, we refinanced our mortgage to a rock-bottom rate. We took on a lower interest rate and shorter term. As soon as COVID-19 hit and interest rates tanked, I sprung into action and got on the phone with a lender.

Tips for deciding whether to pay off your own mortgage

I’m sharing my story because I hope I can save you from agonizing over your own mortgage. Here’s a conglomeration of things I learned along the way.

Tip #1: Consider your needs and wants. And your future needs and wants.

What’s your comfort level? Are you a person who needs to know that debts are paid off so when disaster hits, you’re in a good situation? Are you absolutely sure your job is stable? The thing is, we don’t know what’s going to happen (COVID-19 taught us that). Maybe you have life insurance, so if the worst does happen, you leave money for your family to pay off the mortgage. (That’s certainly something we took into consideration.)

On the other hand, you might take a look at the numbers and run straight for the stock market because you know you’re going to make more if you invest. Putting blinders on and sticking to the numbers is definitely one approach. Remember, there’s really no right or wrong answer. You are not your friends, your next-door neighbors, your sister, your parents — or to whomever you may be comparing yourself and your situation.

The point is, on some level, it’s a personal decision. Consider your own priorities.

Tip #2: Do the math.

Do you remember hearing the words “amortization schedule” when you closed on your home?

If not, that’s okay.

It’s a giant table that lists all the mortgage payments you’ll make over time and how each payment is applied toward both the principal balance and interest of your mortgage. Your bank probably has an amortization calculator that will help you understand what will happen if you “up” your payment, refinance or pay a giant lump sum toward your principal.

Also, some banks charge fees for paying off your loan early. Check into whether your bank will charge you extra. Many banks no longer do this but check to be sure that your bank doesn’t. The last thing you’d want is to be penalized for doing a good thing for yourself!

Tip #3: Make a decision. That doesn’t mean you can’t reevaluate later.

Sure, you can just pay the minimum on your mortgage for 15, 20 or 30 years — whatever your mortgage term is. But if this doesn’t sit well with you, do something about it. Take matters into your own hands.

Spend some time considering how you’d ultimately like to end your mortgage. Again, you can keep it for the full 30 years. Or you might have a 15-year mortgage and decide you want to pay it off in 8 years!

You as a couple, or you alone, are in charge of your financial future. Your financial advisor isn’t going to make the final call. Your friends, your family aren’t going to make those decisions for you, either.

Be the captain of your own ship!

This is not to say that your goals won’t change later. You might make a different decision 10 years into your mortgage. Your financial situation could completely change. For example, maybe you don’t have extra money to chuck at your 30-year term mortgage when you first buy or build your home, but then you get a better job later. You may switch gears and decide to focus on paying off your mortgage!

Final wrap-up: Do what’s best for you — confidently!

Are there days when I second-guess our decision?

Of course. (Remember, I’m incredibly indecisive.)

The reason I probably agonized for months (I know, too long!) is that we only have one life to live. The choices we make now dictate how we live down the road. I try to think about our decisions very intentionally so our future selves are satisfied. It’s a major thing for me.

Thoreau said, “Go confidently in the direction of your dreams. Live the life you have imagined.” And that’s really what it’s all about, right?

Do you want to pay off your mortgage early?

The post Pay off our mortgage or not? A glimpse into a couple’s final decision appeared first on Making Sense Of Cents.

from Making Sense Of Cents

via Finance Xpress

The post Money Moves to Make in Your 30s appeared first on The Dough Roller.

via Finance Xpress

I’ve got an efficiency idea that could do my community good. Provide subsidized housing to those who may need it the most. Given times are more difficult during a pandemic, being able to provide affordable housing may be very beneficial. The remodeling in my new home is almost done. I could move into my new

The post Solving The Housing Affordability Crisis By Providing Subsidized Housing appeared first on Financial Samurai.

from Financial Samurai

via Finance Xpress

The post Best Insurance Options for Gig Workers appeared first on The Dough Roller.

via Finance Xpress

Most Americans agree that racial discrimination has been, and remains, a big problem. But that is where the agreement ends.

Listen and subscribe to our podcast at Apple Podcasts, Stitcher, or elsewhere. Below is a transcript of the episode, edited for readability. For more information on the people and ideas in the episode, see the links at the bottom of this post.

* * *

On last week’s episode, we started to pull on two threads that look quite different at first glance but, if you pull hard enough, they can lead you to similar conclusions. The first story began with the rise of women’s soccer in England, back in the 1920s:

Stefan SZYMANSKI: They attracted a crowd of 53,000 people, which was a complete sellout crowd.

And subsequently, a ban on women’s soccer, out of concern it might cut into the men’s game:

SZYMANSKI: I think if they hadn’t been banned, women’s soccer today would be a global phenomenon.

And whether something should be done to address this ancient infraction.

SZYMANSKI: Well, I believe that the right answer here is reparations. I think the soccer authorities that grew rich with men’s soccer should be diverting a significant amount of their resources into women’s soccer.

That was the soccer economist Stefan Szymanski, who teaches at the University of Michigan. Another economist, Darrick Hamilton of Ohio State University, argues in favor of reparations to address a much more complicated and painful economic disparity:

Darrick HAMILTON: The racial wealth gap is such that the typical Black family has about 10 cents on the dollar as a typical white family.

The origins of this Black-white wealth gap in America clearly date back to slavery:

HAMILTON: But that history of racial disparity as it relates to wealth-building certainly didn’t end with slavery. There was the Homestead Act. There was the G.I. Bill. There was a system of sharecropping. There’s a system of Jim Crow. There is a system of redlining. It was government-facilitated.

And because government actions helped create the wealth gap, Hamilton argues it’s up to government to address it. Democrats in Congress have for a few decades wanted to study and develop proposals for some kind of reparations. But what would reparations look like? What form would they take? How much would they cost? Who would be eligible? These are important questions that often get lost in the noise whenever the topic of reparations comes up in the public sphere. The very word has become so loaded as to be reduced to a slogan, or an anti-slogan, depending on your position.

Consider two recent polls that illustrate this friction. The first poll, by Monmouth University, found that 76 percent of Americans agree that racism and discrimination are, “a big problem.” And that included 71 percent of white Americans. This represents a huge increase over just the past few years. Granted, those numbers may be high because there’s been so much related news lately and attention paid lately. And talk is cheap: it’s easy to say you think something is a big problem; does that mean something gets done about it? And if so, what should be done about it?

Let’s look at the second poll, which was conducted by Reuters and Ipsos. It found that 50 percent of Black Americans support cash payouts to the descendants of slaves. And how many white Americans agree? Only 10 percent. So, how will this play out? The city of Asheville, N.C., may have just provided a good clue. Last week, its seven-member city council — with two Black members — unanimously passed a reparations resolution. It has two primary components. The first: a formal apology not only for the city’s role in slavery but for the subsequent decades of segregation and discrimination in housing, education, policing, labor, and so on.

The second component — the reparations — does not, however, include direct cash payments. It is essentially a holistic affirmative-action program, directing money and resources to affordable housing, business and career opportunities, education and health care, neighborhood safety, and more. The Asheville resolution also, “calls on the state of North Carolina and the federal government to initiate policymaking and provide funding for reparations at the state and national levels.” So, today on Freakonomics Radio: how likely is that to happen? What are the pros and cons of reparations? And just how slippery is this slope?

* * *

The Ohio State economist Darrick Hamilton, who is Black, is pro-reparations. But he takes care to not be too prescriptive when it comes to dollar figures or eligibility requirements. At least not yet. He prefers the process be started by a federal commission.

HAMILTON: First, we certainly need to have the commission to do the study to make all the evidence available of the atrocities that have taken place.

But other people have gone ahead and put dollar figures on reparations. The Duke economist William Darity, one of the elder statesmen of reparations research, took a look at what “40 acres and a mule” would be worth today. That was what freed slaves had been promised after the Civil War — a promise that President Andrew Johnson reversed shortly thereafter. Darity ran the numbers, based on the amount of land the freed slaves had stood to inherit, compounded at 6 percent interest since 1865. The total? Just over $3 trillion. And that’s just for the 40 acres and a mule they were never given.

Darity has also calculated what it would cost for a reparations program that would erase the Black-white wealth gap. That estimate comes to $10 to $12 trillion; another estimate, by the University of Connecticut political scientist Thomas Craemer, comes to $14 trillion, by including the cost of the slaves’ unpaid labor. Now, let’s say you agree in theory that Black Americans descended from slaves are entitled to reparations for both the moral injustice of slavery and the financial injustices from slavery onward. Even so, $14 trillion may strike you as an unrealistic amount of money. It represents nearly 70 percent of a full year of U.S. G.D.P.

HAMILTON: The arguments that are typically made are, “Can the government afford it?” The last financial crisis is indicative of our ability to generate resources. It was something in the order of $700 billion that was passed by Congress to address the last Great Recession.

More recently, Congress has been spending trillions of dollars on pandemic relief.

HAMILTON: Our ability to generate resources through public ways, I think has been dispelled by recent actions. So, we can certainly afford it and generate the resources if we desire.

This would require the federal government to take on even more debt than it has lately. That in and of itself will make any sort of large financial reparation proposal unpalatable to some people. Others may find it unpalatable for different reasons. Here’s how Senate Majority Leader Mitch McConnell put it: “I don’t think reparations for something that happened 150 years ago for whom none of us currently living are responsible is a good idea.”

HAMILTON: Other critiques about reparations include, “Well, won’t it be divisive? Won’t you be creating further divisions between Blacks and whites by making the point that you’re giving a handout to Blacks?” Well, if reparations is done correctly, we would have that reconciliation.

For Hamilton, reparations being done “correctly” begins with an acknowledgment of why they are necessary.

HAMILTON: Clear-throated, full acknowledgment of the atrocities that have taken place and the fact that these were atrocities that were committed with the will of the government, the complicity of the government, and sometimes actions of the government.

But also:

HAMILTON: We would need a moral shift in our American ethos in order to enact reparations. The fact that we don’t have it now isn’t reason not to do it. It’s even more reason to do it, because we need to cleanse our soul. We need to have a more perfect union. Not only because it will lead to greater equity, prosperity, and perhaps defuse some of the cleavages that exist in America today between us versus them. It is the right thing to do. It is the just, moral-compass thing to do. That in and of itself should be reason to do it.

Okay, so let’s say the moral shift does happen. And let’s say it leads to a reparations package that does include a cash payment of — just for argument’s sake — $100,000 to every eligible Black American.

Glenn LOURY: Let’s say $100,000, that’s a lot of money. That would make a real difference in people’s lives.

That’s Glenn Loury, an economist at Brown University. A few decades ago, he became the first Black tenured economics professor at Harvard.

LOURY: Every African-American person receiving a six-figure transfer would relieve a lot of people’s problems paying their rent. It would allow them to educate their children more effectively. They might move to different neighborhoods. They might be able to invest in their own education and personal development. They might be able to take better care of their elderly. They might be able to avail themselves of alternative education for their children than what they get from the public schools. They could retire their college debt. I mean, there’s no way around the fact that getting 100 grand is a good thing. You will not hear Glenn Loury say that that is not a good thing.

But you will also not hear Glenn Loury say that he is actually in favor of reparations.

LOURY: The basic fact is that whites have more wealth than Blacks, however you measure. Now, partly that’s a consequence of history and partly that’s a consequence of ongoing dynamics. People inherit wealth from their forebears, from their parents, and so on. So, part of that is a reflection of the past, but part of it is also a reflection of what’s going on in terms of the creation of wealth. A lot of people will have created the wealth that they possess through years of effort and entrepreneurship and so on.

Stephan DUBNER: So, if you have that complication to deal with, right, which is that it’s not all a consequence of history, how do you start thinking about the smartest ways to shave that Black-white gap in America today?

LOURY: First of all, I would question whether or not that’s the right objective, okay? The issues that should concern us, I think, are largely issues that transcend the racial categorization. I would be thinking about people without wealth. I wouldn’t be thinking about people who are Black without wealth. There’s looking backwards and there’s looking forwards. So, we can look backward as many have done and attempt to calculate and calibrate what were the impact of redlining, of Jim Crow segregation, of slavery, of the failure to distribute 40 acres and a mule to the freedmen and so on, and we could try to do an estimate of what would wealth be but for that historical thing.

But the other thing is looking forward. Wealth is a stock. Income is a flow. So, the stock evolves over time under influence from the flow. We can shift wealth around at a point in time. But we may not change the steady-state wealth holdings if we don’t deal with the flow. So, that’s why I want to say the creation of wealth deserves to be a part of this conversation. Because, thinking simplistically, but I think the arithmetic works out, if I don’t change the flows, I’m going to end up back in the same situation after a while, no matter what I do.

Ideologically, Loury is hard to pigeonhole.

LOURY: Well, I have of late been saying I’m a man without a country. I call myself a centrist. I believe in markets. I think capitalism has been a force for good in the world overall. I think that the tendency toward planning and social control is mischievous.

Loury grew up on the South Side of Chicago. His mother was a secretary for the Veterans Administration and his father worked for the I.R.S.

LOURY: I was born in 1948. I can remember getting pulled over by police officers driving on the Dan Ryan Expressway as a kid 17, 18, 19 years old. And all the cops were Irish, mostly. They were belligerent. They were discriminatory. They were contemptuous. I mean, I remember the civil-rights movement and I remember that there were many people who opposed what Martin Luther King Jr. and company were trying to accomplish. You know, there were arguments about stuff that we take for granted right now. If you were to look at the statistics there’s a much bigger African-American middle class and so on. The penetration in occupations and institutions is quite different from what it had been and so on.

Despite this penetration, and progress, Loury has experienced plenty of racism.

LOURY: I’ll just tell you one. The year is 1982. I’m in the faculty club at Harvard University. I’m a newly tenured professor of economics and John Kenneth Galbraith — the great John Kenneth Galbraith — is engaged in a conversation in the faculty club. Do you know that he extends his hand to shake without turning his head to look me in the eye? He continued his conversation and he had his hand out like this for me to shake it. And I couldn’t believe what was happening to me.

DUBNER: So, when you hear someone use the phrase “systemic racism” — a phrase we’ve been hearing much more lately in the U.S. — your response to that phrase is what?

LOURY: I think you’re playing with words and avoiding the hard work of trying to discover complex historical causal chains. It’s a slogan. It’s a bludgeon. You’re saying, “Be for motherhood and apple pie.” Who’s not against “systemic racism”? But if it explains everything, well, then at the end of the day, it doesn’t explain anything at all, does it?

DUBNER: When you say “it dismisses the hard work of trying to understand those complex causal changes,” give me an example of what you mean by that. Give me an example of the difference between a causal explanation or mechanism and sloganeering.

LOURY: Well, let’s take the issue of school discipline. Suppose we were to discover on examination that the racial disparity in the rate of kids being suspended from school disfavored African-Americans, and we were to attribute that fact to systemic racism. But in fact, what might be happening in the schools is that for a variety of complicated social and historical, economic, and political reasons, the African-American kids on average are showing up with patterns of behavior that are disproportionately disruptive and that reflects itself in their being suspended at a higher rate.

Now, of course, it might be racism. It might be that the school discipline system is systemically biased, but it might not be. And the difference between those two states of the world where racism explains everything or where complex social and historical processes are at work is the difference between solving the problem and not solving it.

DUBNER: So, let me ask you this. Not long ago, Glenn, you said, “I think the reason that we’re talking about reparations now is because people are out of ideas. They don’t know what to say about racial disparities other than to point a finger and then try to create a kind of political issue.” Talk to me a little bit more about that, what you think are either economic or educational or tax policy programs that you think really would work better.

LOURY: Well, everything is not policy, and part of what I’m getting at there is that some of the problem has its roots in the dynamics internal to the African-American community, which we are responsible ourselves to address. And this is very difficult territory because it feels like blaming the victim to a lot of people. You know, if I observe that — take the cops and the problem that we have in the cities with order maintenance and profiling. So, this has now become kind of a trope. I mean, it’s now argued without any second thought. “You profiled me. That was racist.” I’m Black. I’ve got a Ph.D. from M.I.T. I’m a middle-class person, but I walk into a department store and I notice that the security person has his eye on me. I feel put upon.

Now, that’s true. It happens. A police officer asked me to open my trunk when I’m stopped and I’ve got a New York Times open on the front seat of a B.M.W. and I’m wearing a suit. What does he think? I’ve got a cache of drugs in my trunk? I’m offended by that. Of course, that happens. On the other hand I’m an economist and we believe in statistical decision theory as a reasonable model of how it is that uninformed individuals act under incomplete information. And one of the things that they do is they correlate unknown things with the known things and they use statistical frequencies. And the bottom line is my race is correlated with the behavior that they can’t observe. And so, they use my race’s information. I don’t know how you stop people from doing that.

I think you can legislate against it. You can administer against it. But at the end of the day, there’s something very cognitively fundamental about that, and it’s something that would affect the behavior of everybody, regardless of their race. Anyway, that’s a digression by way of saying if two-thirds of the kids born to a Black woman are born to a woman without her husband, and if amongst African-American adolescent males, I observe a high frequency of behavioral maladaptation, of aggression, of whatever, am I entitled at all to consider the possibility that the nature of African-American family dynamics might have a role to play in the behavior problems of some male adolescents, which then reflects itself in a lot of this drama that we see between the cops and African-American men on the streets of these cities?

I think there are issues that we African-Americans have to confront so that the underlying causal model, historical violation reflected, for example, in a wealth gap, leaves us with a contemporary problem, the remedy for which relies on public policy. That model is incomplete because the historical violation did not only deprive us of assets. It also created context within which the dynamics of social development and evolution left us with large numbers of violent young men in the cities. That’s a problem in and of itself. Read what’s going on in Chicago on a daily basis. It’s not letting white people off the hook or America off the hook for its historical crimes to observe that some of the stuff that’s holding us back is within our reach to be able to deal with and really can’t be effectively dealt with in any other way.

The indirect argument — “I’ll solve the problem of violence on the South Side of Chicago with more social spending, with more money for the schools, with more social workers, with midnight basketball, with whatever” — I don’t think the evidence is very strong that I can get all the way to where I want to go in that way. That’s the kind of thing that I’ve been feeling the need to call to people’s attention, that we African-Americans have some responsibility for how it is that we raise our children and organize our communities and so forth. I think that should be a part of the discussion.

DUBNER: So, if that’s the part of the discussion you want to raise, that gets me to the next level, which is how do you address that? Because it strikes me as you’re speaking that a lot of the more observable issues that people speak out against, whether it’s overt racism, whether it’s income gap, and so on — there are solutions, I’ll kind of put those in quotes, proposals for solutions that look pretty sensible and pretty mathematical. The problem you’re addressing, however, it’s harder to put it into numbers. And I appreciate that you bring up the fact that it’s difficult to even talk about in certain circles. And in fact, if you weren’t Black, you probably wouldn’t have brought up that point, am I right?

LOURY: Yeah, well, I’m not “not Black.” I am Black. Therefore, I don’t know what I would have done. But I expect that you would not have brought up that point or many others who are not Black, and I don’t blame them because nothing but grief would come of it.

DUBNER: So, considering that you do bring up the point and that it does concern these unobservables, do you have any ideas for how to address those?

LOURY: I do not, to be honest with you. I mean, I can gesture at some things. You know, I can talk about the role that intermediary institutions between the individual or the household and the state. So, this would be voluntary organizations, this would be churches and things of this kind. What about Big Brothers and Big Sisters? What about mentoring? You know, it’s not as if we are completely prostrate here without any capacity for self-actualization. How do we educate our children? So, this woke moment of heightened sensitivity about racism, which manifests itself as much amongst whites, I would reckon, on the left as it does amongst African-Americans, I think that bespeaks what’s actually possible.