What To Do When Stock Market Volatility Returns

7:36 AM Every so often, the stock market will take a dive when you least expect it. When we sense danger, the natural tendency is to run the other way, preferably in a herd for survival. As a result, sell-offs often intensify as computer algorithms now join us humans in rushing out of positions.

Every so often, the stock market will take a dive when you least expect it. When we sense danger, the natural tendency is to run the other way, preferably in a herd for survival. As a result, sell-offs often intensify as computer algorithms now join us humans in rushing out of positions.

As I’ve gotten older, despite much larger absolute dollar swings, I’ve become more sanguine in times of stock market volatility.

Here are some things you can do to reduce your fear and not sell or buy at inopportune times.

During Times Of Stock Market Volatility

1) Review your financial objectives. There is no point saving and investing money if it doesn’t have a purpose. Once you crystallize the reasons why you’re working so hard and taking risk, you’ll be able to make more rational decisions. You’ll also re-motivate yourself to do what’s financially best for you and your family.

Here are some common financial objectives:

* Save enough in after-tax investments to give yourself optionality to do something new.

* Return at least 2X the risk-free rate of return each year.

* Save enough to make your child a 529 plan millionaire so she can graduate an independent woman after college all thanks to you.

* Save enough to cover any long-term care costs for aging parents.

* Max out your 401(k) every year without fail since few get pensions anymore.

Our key objective: Because we tried for so long to have a child and were finally blessed with one in 2017, my key objective is to enable my wife and me to be stay at home parents for the first five or six years of his life before he goes to kindergarten. Once he goes to kindergarten, one or both of us get to stop sacrificing our careers and income to go back to work since he’ll be busy most of the day. Whether we go back to work or not, is a different matter. It’s just nice to have the option to have more adult interaction again.

2) Determine your risk tolerance to the best of your ability. To determine your risk tolerance, simply ask yourself how much you’re willing to lose in your investments before needing to sell. If you never plan to sell because you know stocks and bonds have generally gone up and to the right for decades, perhaps you have a high risk tolerance. If you plan to take profits if the stock market is down 20% or more, perhaps you have a medium risk tolerance. If you’re freaked out by a 10% correction, then perhaps your risk tolerance is very low.

Just know that whatever you think your risk tolerance is, you’re likely overestimating it by at least 10%. When people started losing big money during the 2008-2009 financial crisis, there was mass panic because they were also losing value in their houses, which are usually owned with debt. Meanwhile, when your company is going through its third or fourth round of mass layoffs, the desire to raise cash becomes almost impossible to prevent, especially if you have a family to support.

Our risk tolerance: When we left work at 34 respectively, our risk tolerance was medium-to-high since we only had to provide for ourselves. Further, it took a lot of guts to truncate promising careers so young. But due to our current #1 objective of being stay at home parents for at least five or six years, our risk tolerance is now medium-to-low. We would feel uncomfortable losing more than 20% of our after-tax investments, which cover 100% of our living expenses.

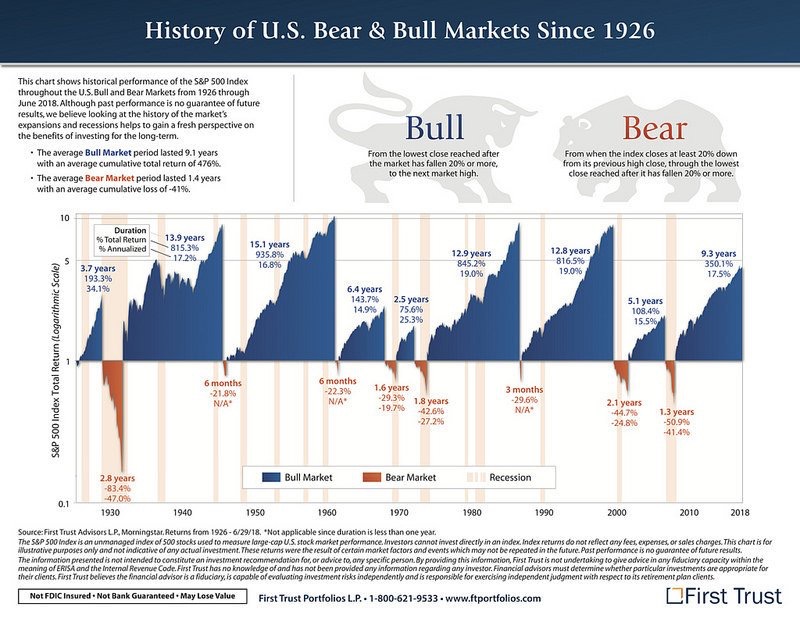

3) Understand the historical returns of different stock and bond portfolio weightings. Knowledge truly is your best friend when it comes to investing. There are no investment guarantees, but we do have historical data we can study to get an idea of how our investment portfolios will perform over time.

Given you’ve gone through your financial objectives and made a best guesstimate on your risk tolerance, you are rationally going to build an investment portfolio that meets your risk profile. Here are the historical returns between 1926 – 2016 according to research from the Vanguard Group.

A 0% weighting in stocks and a 100% weighting in bonds has provided an average annual return of 5.4% since 1926, beating inflation by roughly 3% a year.

A 20% weighting in stocks and an 80% weighting in bonds has provided an average annual return of 6.6%, with the worst year -10.1% and the best year 29.8%.

A 30% allocation to stocks and a 70% weighting in bonds has provided an average annual return of 7.2% a year, with the worst year -14.2% and the best year +28.4%.

A 40% weighting in stocks and a 60% weighting in bonds has provided an average annual return of 7.8%, with the worst year -18.4% and the best year +27.9%.

A 50% weighting in stocks and a 50% weighting in bonds has provided an average annual return of 8.3%, with the worst year -22.3% and the best year +32.3%.

A 60% weighting in stocks and a 40% weighting in bonds has provided an average annual return of 8.7%, with the worst year -26.6% and the best year +36.7%.

A 70% weighting in stocks and a 30% weighting in bonds has provided an average annual return of 9.1%, with the worst year -30.7% and the best year +41.1%.

A 80% weighting in stocks and a 20% weighting in bonds has provided an average annual return of 9.5%, with the worst year -34.9% and the best year +45.4%.

A 100% weighting in stocks and a 0% weighting in bonds has provided an average annual return of 10.2%, with the worst year -40.1% and best year +54.2%. We saw this sell-off happen in 2008-2009 when many investors sold at the absolute bottom.

My public investment portfolio weighting: I’ve gone from a 95% average equities weighting in my 20s, to an 80% average equities weighting in my 30s, to a now 60% average equities weighting in my early 40s. My objective is to earn 2X the risk-free rate of return, or now roughly 6% a year.

Based on historical returns, having a 30% stock / 70% bond weighting for my return objective would be more appropriate. However, given my financial background and passive income, I’m comfortable taking on more risk. After getting an MBA and spending my entire career in finance, it would be strange if I wasn’t comfortable with investing.

4) Make up for your losses with extra work. Whenever your investments lose money, a humbling way to look at your paper or realized loss is to figure out how many more months of work will be required to make up for your loss. This exercise will not only help you assess your true risk tolerance, but it will also motivate you to build extra income streams.

One of your goals on the road to financial independence is to never experience a decrease in your net worth each year. In the beginning, your income and aggressive savings should be enough to consistently grow your net worth. But once you start amassing a large investment portfolio, there will be a breakpoint where your investments may start generating a significant boost or drag to your net worth. This is one of the reasons why you should dial down risk the wealthier you get.

If your investments are losing money, get offended at your sensibilities. Then get motivated to do some consulting work or take on some gig economy jobs or my favorite, build a side hustle online. Only as a last resort should you be selling and drawing down principal to pay for life.

My hustle: When I started losing big bucks starting in 2008, I decided to finally start Financial Samurai in 2009. I knew it wouldn’t make a lot of money in the beginning, but I had to at least try in order to give me options in the future. If Uber or Lyft had been popular back then, I’m sure I would try and make extra money at night as well.

5) Always have a comfortable cash hoard equal to 5% – 10% of your investable assets. When the stock market is falling apart, you will feel most helpless if you don’t have a cash cushion. By having a cash hoard, you will not only have a financial cushion, you will also have the firepower to take action during violent sell-offs.

Buying stocks during a downturn is a positive that counteracts the negative of losing money from your investments. Sometimes it feels like shooting a rifle at a fighter jet bombing your village, but at least you’re doing something about the siege. This helps your psyche.

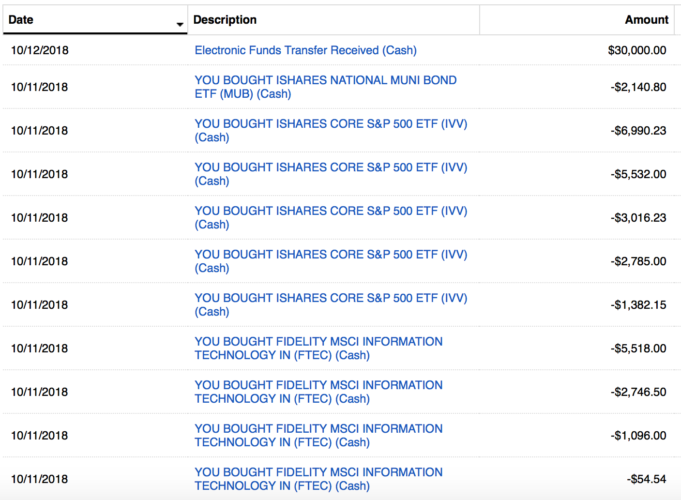

Bought $30K in my wife’s after-tax account on 10/11/2018 after the 6%+ correction

My cash: At any given moment, I’ve always got between 5% – 10% of my investable assets in cash, especially now that money market rates are paying over 2%. As a result, I never feel helpless during a stock market correction anymore. Instead, I feel excited to put some cash which I don’t need to work.

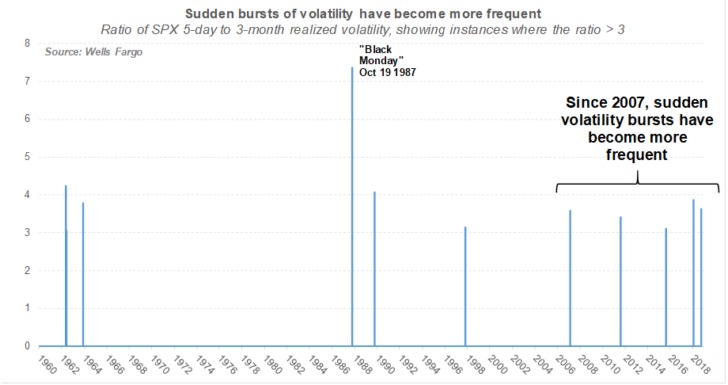

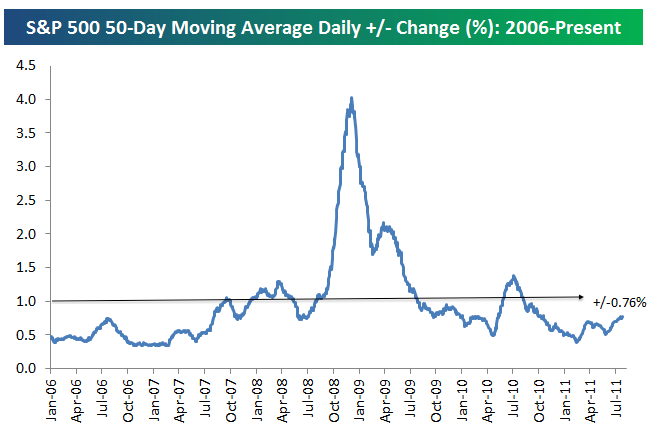

6) Have a concrete plan of action. Given you always have spare cash to take advantage of opportunity, you should always develop a plan whenever there are significant changes in the market. For example, we know that the S&P 500 moves +/0 ~0.76% a day on average. Therefore, if you are long term bullish, you should consider buying when the S&P 500 sells off 2X, 3X, 4X, or 5X greater than average with increasing amounts of capital.

What I’m doing: My goal is to maintain a roughly 60/40 stock/bonds split. When equities are selling off, my stock weighting naturally declines. Therefore, I will look to re-up my stock weighting whenever there is a 1.5% or greater decline in the S&P 500. Generally, I will deploy capital in three to five tranches over a 5% – 10% decline e.g. $20K when -1.5%, another $30K when -3%, another $40K when – 5%, etc. If the S&P 500 declines by greater than 10%, I will redeploy a set amount of capital for every 1.5% decline over three to five tranches again. Given I don’t plan to buy another property for a while, my goal is to invest 100% of my savings each month to generate passive income.

7) Extend the investment time horizon. We used to joke on Wall Street that whenever we made a bad investment we’d describe it as, “a long-term investment.” But if you can truly extend your investment timeframe into the decades, you’ll feel better about your paper losses.

The trick I’ve learned which helps me elongate my investment time horizon is to think in the future what my kid or younger relatives will think about asset prices today. Every one of us wishes we had purchased and held stocks and real estate 30 years ago. Therefore, think about what the children in our lives will think about the investment opportunities we have today.

My time horizon: I’m certain stocks and real estate will be higher by the time my kid enters the workforce circa 2039, therefore, I’m comfortably in the buy and hold mode. Whenever there are corrections in the S&P 500 index or in specific stocks I believe are long-term winners, I utilize my cash hoard to buy.

Then I imagine the day when my son graduates from college and ventures into the real world to be his own independent man. If he’s a good person with a kind heart, I will be that loving father who will one day say, “I’m so proud of all the struggles you’ve had to overcome. Let mom and dad help you with anything you need, because surprise! We invested in stocks and real estate when you were a baby, just in case you decided investing back then would have been a great idea.”

Of course if he’s mean and rotten, we’ll donate all the money to charity instead.

8) Keep busy doing something more pleasurable. It’s counterproductive to overly focus on your tanking investments when you’ve got objectives 1 – 7 down. Instead, go have some sangria with friends and loved ones. Go for a nice free long walk in the park. Exercise. Life is the same whether stocks are going up or down.

My activities: I always feel better after a good game of tennis or softball. The endorphins kick in, the body becomes nice and sore, and my mind feels like it got a nice massage. I also spend more time writing on Financial Samurai because writing is cathartic. It helps me work through logic and emotion to see things more clearly.

9) Earmark some profits to pay for a better life. Instead of having the market incinerate all your money, you should consider spending your profits on yourself, especially if you’ve hit your financial objectives. Otherwise, there’s really no point saving and investing. You want to consistently crystallize the value of your investments, which is why buying real assets that provide utility like a house feels so good. Alternatively, you can use your profits to buy experiences that tend to appreciate over time as well.

What I’ve spent money on: I’ve used some profits to buy a family car prior to our son’s birth. Sometimes I catch myself at a stop light feeling giddy the car was bought with the returns from my severance check. I also built an awesome deck facing the ocean off our master bathroom with some NASDAQ proceeds. Eventually, when our son turns five, we’ll take some profits to pay for an exciting international family vacation.

Although I could have made more money if I kept the money invested, it feels wonderful to actually see the investments be utilized for a better life. My biggest hope now is that my son’s 529 plan returns enough in the next 17 years to provide him one or two years of free college tuition.

Stock Market Corrections Will Happen

Accept that part of earning a reward is taking on risk. Over the long run, your risk should pay off if you have the proper asset allocation and time horizon.

The only people who lose are those who are too afraid to take any risk at all. These are the people who hoard most of their net worth in cash. These are also the people who stay at one job forever because they’re too afraid to move.

If you have a clear plan for how you will allocate capital, you will better conquer your fear of investing. If not, you can always just have a robo-advisor automatically invest for you once you’ve established your risk parameters.

If you believe in the bull market, then you should buy the dips. If you believe a bear market is imminent, then you should sell into strength. Given my investment horizon is at least 20 years, I plan on consistently generating enough cash flow to buy as many dips as possible.

Consider Real Estate If You Don’t Like Volatility

One of the main reasons why I prefer real estate over stocks is due to real estate’s less volatile nature. With real estate you have steadier rents and an asset the is tangible that provides utility. Real estate just doesn’t disappear overnight like stocks.

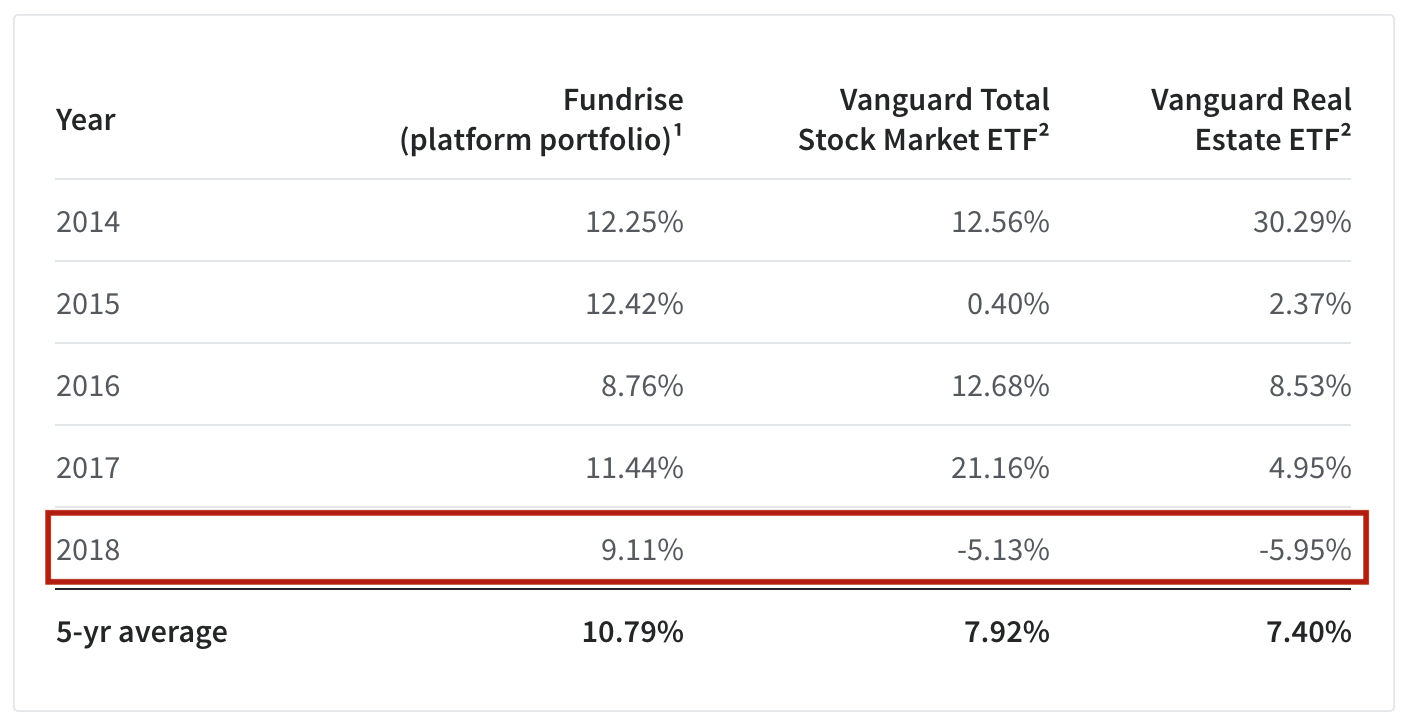

For example, take a look at Fundrise’s 5-year performance versus the S&P 500 and the Vanguard Real Estate ETF. When the S&P 500 took a tumble in 2018, Fundrise’s platform portfolio outperformed by a whopping 14%.

You can sign up for Fundrise for free and explore their offerings. I’ve personally invested $810,000 into real estate crowdfunding to take advantage of lower valuations and higher net rental yields in the heartland of America.

Updated for 2020 and beyond.

The post What To Do When Stock Market Volatility Returns appeared first on Financial Samurai.

from Financial Samurai

via Finance Xpress

0 comments