The Hardest Mortgage Refinance Ever: Key Takeaways

12:21 PM

Praise be to all that’s good in this world! After four months and one week, I finally was able to refinance my primary residence mortgage!

My original loan was a 5/1 ARM at 2.5% that began on August 1, 2014, and reset to 4.5% on August 1, 2019. The loan amount was $990,000 and the payment was $3,920 a month.

My new loan is a 7/1 ARM at 2.625%. The loan amount is $700,711, and the new monthly payment is $2,814.41. There was no cost to do this refinance. In fact, I was paid a $220 credit.

A $1,105.59 monthly cash flow improvement helps counteract new preschool and healthcare costs. But it’s not enough, which is why I need to find new ways to save and make money.

My ultimate plan is to pay off our primary residence by October 1, 2026, and never get another mortgage again. Mortgage rates would have to drop another 0.5% for me to even consider going through another refinance.

This refinance was my hardest mortgage refinance ever due to the time it took, the various curve balls faced, a self-inflicted wound, and my general frustration with an unfamiliar lender.

But it’s over now and I wanted to share some takeaways to potentially help you make a better refinance decision.

Low Interest Rates Make A Big Difference

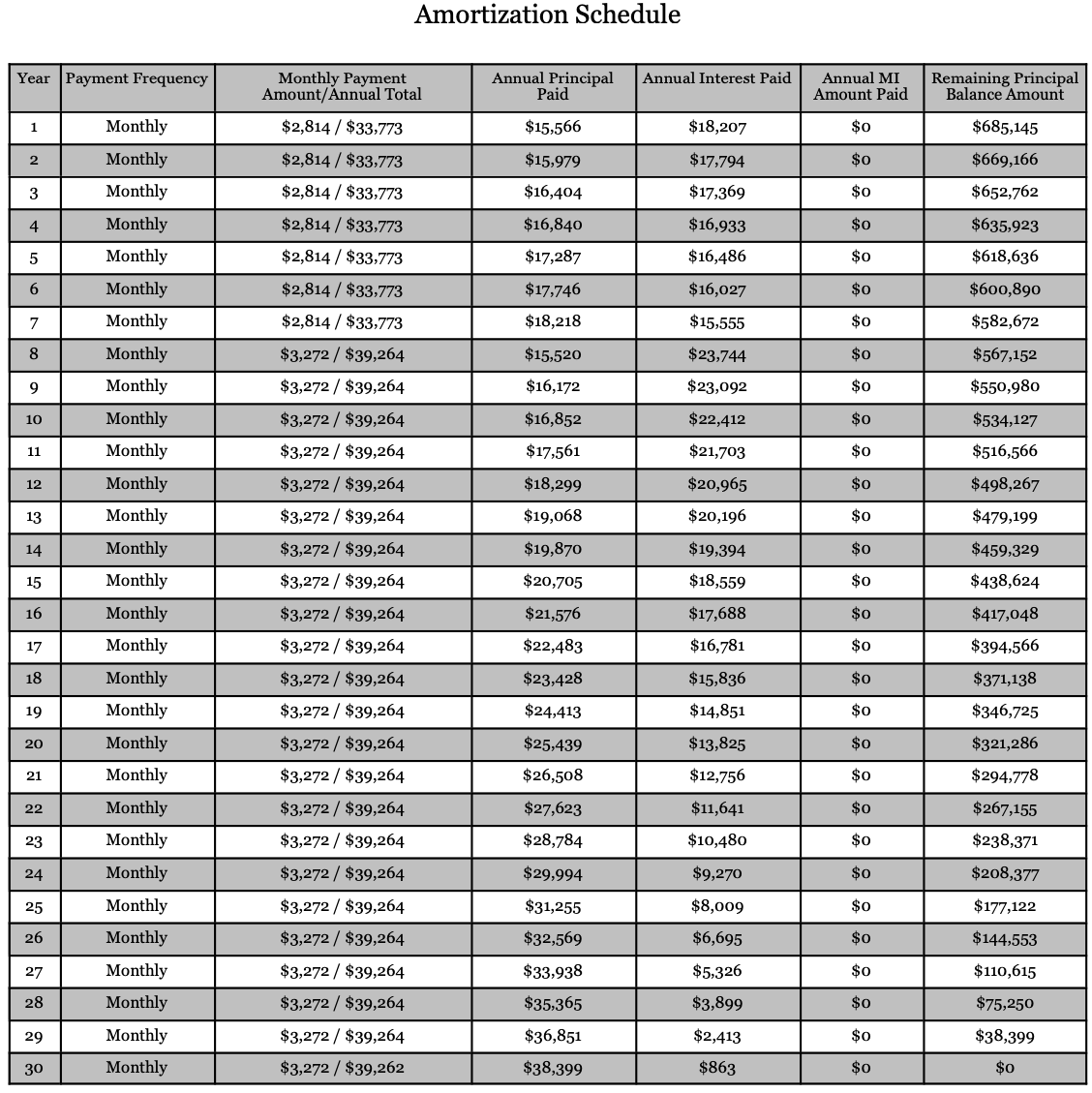

When you refinance a mortgage, you often reset the 30-year amortization schedule back to zero. Therefore, if you want to pay off your mortgage based on your previous amortization schedule, you’ll need to pay extra principal on top of your normal monthly payments.

What you’ll notice from my amortization schedule below is that despite the reset, 46% of my payment goes to paying down principal. Not bad. This is interesting because you always hear that during the initial years, most of your mortgage payment goes towards paying interest.

In fact, by year four, the split between principal and interest reaches parity. And by year five, a greater percentage of the mortgage payment goes to paying down principal than it does to interest.

If my mortgage rate was at 4.5%, my monthly payment would be $3,550 instead of $2,814.41. But $2,628 of the $3,550, or 74% of the payment would go towards interest. By historical standards, 4.5% is not considered a high mortgage rate.

In other words, refinancing now when rates are so low not only improves your monthly cash flow, but also significantly boosts the percentage of your payment going towards principal. It’s like getting a two-for-one special.

Once you’ve successfully closed on your mortgage refinance, request your amortization schedule to crunch your own numbers. I plan to pay down $80,000 a year in extra principal to have a zero balance by 2026.

Lenders Are Still Extremely Strict

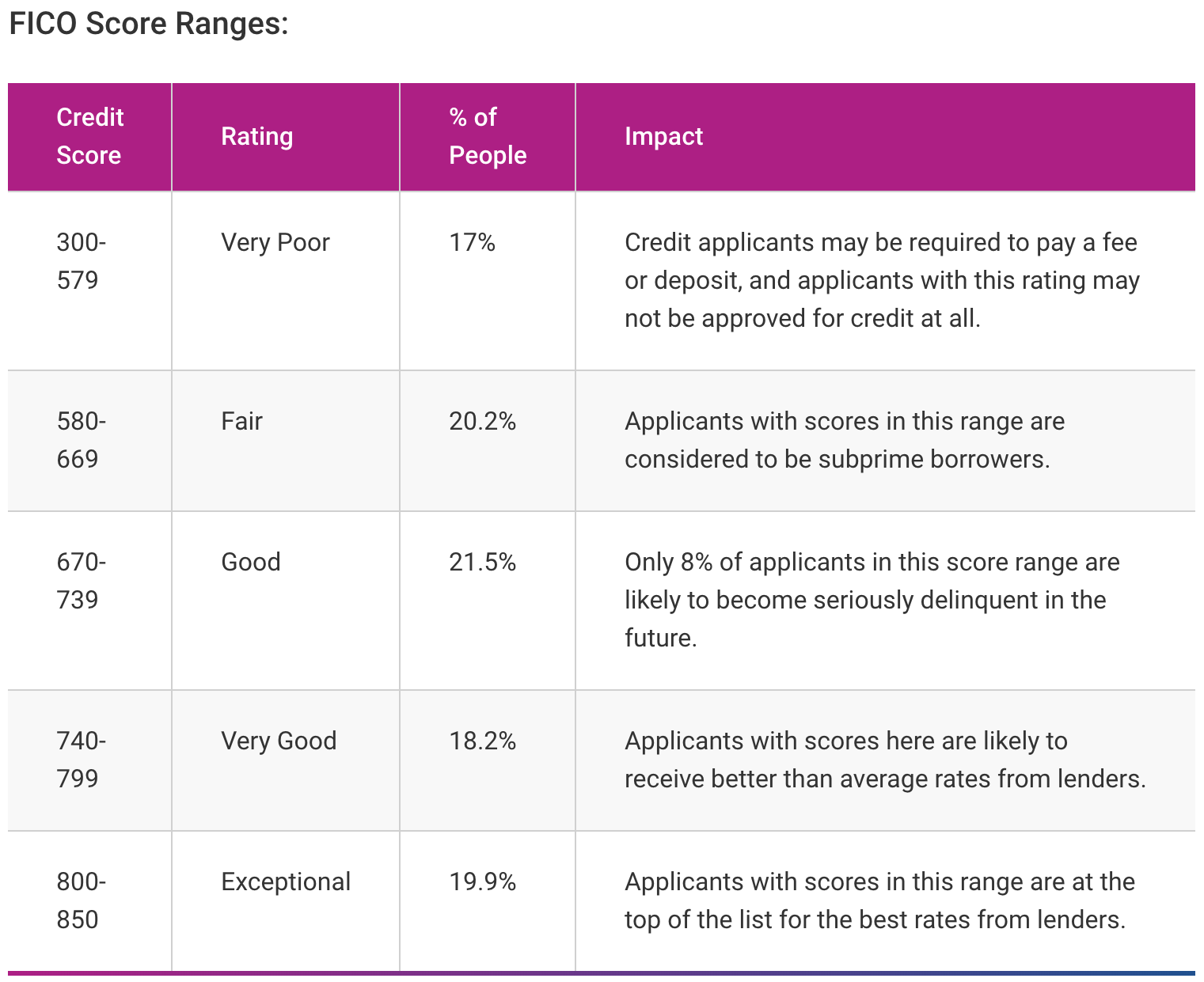

Both Citibank and Wells Fargo told me that in order to get their best mortgage rate, I would need an 800+ credit score.

When I got my last mortgage in 2014, Citibank said 760+ was good enough to get its best mortgage rate at the time.

I’ve always been generally aware that lenders had gotten stricter since the financial crisis. However, because of a huge bull run, I hadn’t expected my banks to be that stringent.

Even after squeaking by with an 804 credit score, both banks still put me through the wringer by requiring an enormous amount of documentation.

I say both banks because I initially spent two months trying to refinance through Citibank. However, after Citibank made it clear it wouldn’t be giving me the lower rate it originally promised, I cancelled 10 days before closing with no penalty.

This is the self-inflicted wound I mentioned. But it was done out of principle and a little bit of stubbornness.

In other words, my entire mortgage refinance process really took over six months to complete!

Although I was still vetted like a suspected spy in FBI custody, it felt good knowing that both banks had been extremely thorough with my finances. If banks were this thorough with me, then they must also be extremely thorough with other mortgage applicants as well.

We know from the latest New York Fed data that the average credit score for approved mortgages is ~760. Based on my latest refinance saga, I absolutely believe it.

Given the stringent standards used to qualify someone for a mortgage between 2010 – 2019, during the next downturn, I just don’t see the same amount of carnage for the housing market. Sure, we might see 10 – 20% corrections, but not the 30% – 50%+ corrections we witnessed during the last financial crisis.

Finally, both Citibank and Wells Fargo required me to have an 80% loan-to-value ratio or lower. In other words, I needed to have at least 20% equity in my home after independent appraisers did their evaluations.

My Title Officer Just Shipped It In

The weekend before I was scheduled to sign all the documents, I discovered the title company was expecting me to pay $9,662.43 at closing. Just looking at the number didn’t make sense because my monthly mortgage payment, including principal and interest, was $3,970 at the new reset rate.

I first had the mortgage officer explain the big number in a huge email. Then I had the title officer basically rehash what the mortgage officer wrote. Both of them stuck by the numbers.

Luckily, I did the math and made them realize they had double-counted one month’s worth of mortgage interest which I had already paid. They also were using an old payoff statement which had a higher balance.

This frustrating incident made me realize that some lenders and title company officers aren’t aware of their own errors or really don’t care. So long as you pay them more at closing, that’s what matters. Further, this incident made me realize now handicapped borrowers are when it comes to understanding all the numbers.

I had to spend at least an hour researching the numbers and calculating why they were over-charging me by at least $4,551.26 at closing. And once I mathematically got to the bottom of the overage charge, they didn’t even apologize.

Instead, the title officer was actually annoyed she had to redo the final refinance statement and said, “I do not work weekends” even though she sent the initial final statement on a Friday afternoon and expected me to sign the documents by Monday morning.

If you don’t work weekends, don’t do this. The title officer was pressuring me to go through with the signing even though I was uncomfortable with the numbers.

If you do not understand the numbers, do not sign the documents! Ask for a clear explanation. You have a right to understand!

Ultimately, I was able to reduce my payoff at closing to $5,111.17 from $9,662.43, a significant $4,551.26 difference.

A No-Cost Refinance Still Costs Money At Closing

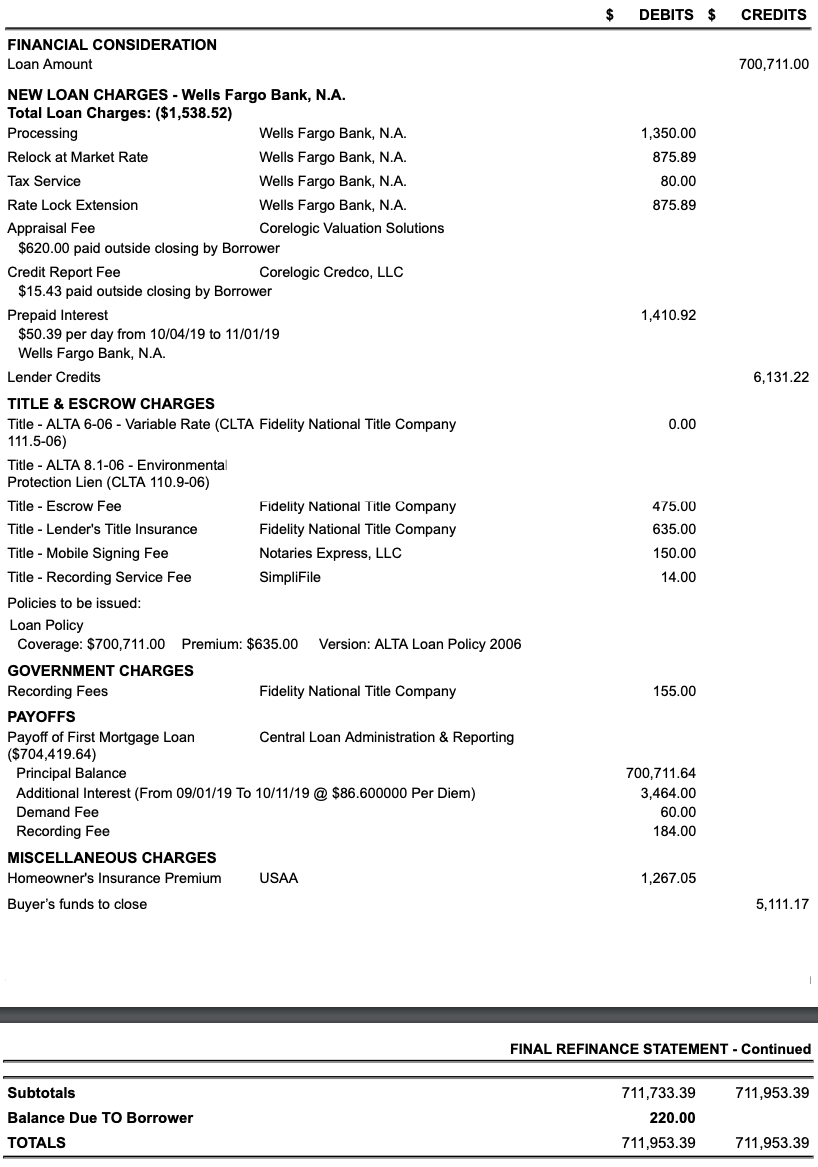

Although my mortgage refinance cost me no money, I still ended up writing my new lender a check for $5,111.17. Sounds like a lot for a no-cost refinance right?

So what is going on when a homeowner who finishes a no-cost refinance still has to pay thousands of dollars at closing? For the uninitiated, it may seem like the lender is trying to rip you off with some sneaky fees. Perhaps the lender is thinking that you’ll acquiesce since, after so many months, you’re so close to the finish line.

I had some similar concerns, especially when the title company wanted me to write a $9,662.43 check at closing. But rest assured, the lenders are not trying to rip you off, at least not directly. By law, the lender has to refund any overage to you within 30 days.

Let me demonstrate using the final fee schedule of my loan as an example so you can see all the refinance costs and credits for yourself.

As you can see from the final refinance statement, there are a lot of fees when it comes to refinancing a mortgage. The only fee that could have been avoided if the bank had been more efficient, is the $875.89 Rate Lock Extension fee.

The credit of $6,131.22 covers all fees plus gives me a $220 balance due. The reason I had to come up with a $5,111.17 check at closing was due to:

- Having to pay the entire year’s homeowner’s insurance premium of $1,267.05.

- Having to pay $3,844.12 in mortgage interest at 4.5% from 9/1/19 – 10/11/19. The statement says I only owed $3,464, which is why I have a $220 balance due.

Therefore, the $5,111.17 is money I owed anyway. I had previously elected to pay my annual homeowner’s insurance premium in monthly installments at no extra charge. But in order to refinance, the law requires the annual homeowner’s insurance premium to be paid in full.

Where the refinance delay cost me was paying a 4.5% interest rate from 9/1/19 – 10/11/19 instead of a 2.625% interest rate. I ended up paying $36.14 more in interest a day for 41 days, which totals $1,481.74.

Not anticipating two rate extensions was a critical miscalculation on my part. I naively trusted the loan officer’s guidance of getting the refinance done within 2.5 months.

On the positive side, I still get 84 months at 2.625% on the back end starting on 10/11/2019.

If you have an ARM, the lesson is to try and complete your refinance a month before it resets rather than after it resets. Further, if you’re close to completing your refinance with one bank, like I was, calculate the potential overage charges before you decide to go with another bank.

You will most likely also have to come up with cash at closing for your no-cost refinance, so be prepared.

Don’t Make Any Large Financial Changes

During your refinance process, don’t make any sudden and large financial changes. These include:

- Big purchases

- Big deposits or withdrawals

- Credit inquiries

- Change your income

- Change jobs

- Lose your job

- Changes to your revocable trust

Expect every single financial move to be scrutinized during the normal refinance window. If you end up having to extend your rate lock, then you need to be extra careful.

With each extension, I had to send new bank statements and brokerage statements. After sending new statements, I was then asked to explain a number of transactions.

In one e-mail from the mortgage officer, he asked me to explain 36 transactions that occurred in my checking account and savings account. These transactions included credits from my 18 real estate crowdfunding investments, capital calls for a couple private equity and venture debt funds, expense reimbursement checks, and various credits that came in from dividends and asset sales.

My stress continued because I had to get another credit check because the original one’s validity expired after two months. This created unnecessary anxiety because I needed to get over an 800 again to keep my 2.625% rate. As some of you know, multiple credit inquiries in a short period of time can hurt your credit score. Luckily, my score came out the same at 804 again.

Refinance For Financial Flexibility

Several folks have asked why didn’t I just pay off the $700,711 mortgage since I transferred over $1,000,000 to Wells Fargo to get the relationship pricing rate. I’d still have $300,000 leftover to invest.

When I thought I could only refinance at 3%%, I strongly considered paying down the mortgage to $500,000. Once I was able to get the mortgage rate down to 2.625%, however, I felt the rate was too low to pay off, especially since the yield curve was inverted.

At one point during the refinance process, I was able to get a risk-free 2.5% on my cash by opening up an online savings account or buying a 3-month Treasury bond. Although the cash rates are lower now, the difference is so narrow it made aggressively paying down the mortgage a suboptimal move.

Besides, I didn’t have $700,711 in cash lying around, only about $200,000. I would have had to sell $500,000 worth of securities and pay taxes, which is always a downer.

I wanted to have more flexibility with my money by not sinking so much into our primary residence. If there is a recession on the horizon, I want to have enough cash to buy stocks, rental property, or commercial real estate somewhere in the heartland.

Finally, if I change my mind and want to aggressively pay down the mortgage I still can. Given the refinance didn’t cost me money, I was giving myself maximum flexibility.

Always Take Action To Save Money

Although my latest mortgage refinance was a real PITA, I’m glad I went through with it.

Not only was I able to write a series of educational posts to help readers make better mortgage refinance decisions, but I’m also going to end up saving over $90,000 in mortgage interest expense over seven years.

Refinance your mortgage. Refinance your student loans. Take advantage of 0% APR credit card offers if you need a reprieve. Avoid borrowing money for a car. As we face an uncertain economic future, now is the time to take advantage of lower rates to strengthen your cashflow.

Readers, I’d love to hear about your latest mortgage refinance experience. Did you catch any errors made by the lender that needed correcting? How long did your refi take from start to finish? Did you experience a rate extension or two?

The post The Hardest Mortgage Refinance Ever: Key Takeaways appeared first on Financial Samurai.

from Financial Samurai

via Finance Xpress

0 comments