Beware Of The Life Insurance Bait And Switch Tactic

3:04 AMNow that I’m a father, one of the first things I did was call up my life insurance provider to review how much life insurance I have and go through the various term life insurance options.

I was reminded of an existing $1,000,000 term life policy that’s expiring in five years. It was taken out 10 years ago when I was thinking of getting married. I figured, given I had about $1,200,000 in mortgage debt from buying a single family house, it was best to cover such liability so my future wife wouldn’t be financially burdened if I passed.

Now I’ve got 22 years to consider before my son graduates from college. Therefore, I decided to get a quote for a $2,000,000, 25 year term life insurance policy that came out to $181/month with my existing provider. Better to lock down a quote now before anything unhealthy happens, causing my premiums to skyrocket.

Unfortunately, because of the size of the policy, I was required to get my blood drawn, piss in a cup, and do an EKG. I hate getting blood drawn. It’s frankly one of the main reasons why I didn’t want to get a $1,000,000+ policy in the first place. But life insurance isn’t for me, it’s for my family, so I proceeded.

Life Insurance Test Results

The lab technician came to my house and did her thing within 40 minutes. I filled out some forms and checked a box to know whether my blood comes back as HIV positive. What fun it is to wait for potentially life-changing results.

I totally forgot about the life insurance application process for a couple weeks until I got a call from my insurance provider to give me the results. Here’s what he said in a nutshell:

We got your test results back and I wanted to say congratulations for doing so great! You were top rated for 19 out of 20 categories we assess for. For the one category where you were slightly below top rated, your cholesterol came in at 4.6 versus <4.0. You were so close, but due to the results, we cannot give you the Preferred ULTRA rate that we initially quoted, but the Preferred PLUS rate instead. The cost of the Preferred PLUS rate for a 25Y/$2M policy is $226/month.

Damn Gina! Because of not being top rated on 1 out of 20 categories (5%), I have to pay a 25% PREMIUM on my original quote? This seems outrageous. I told them I wasn’t happy with this new price, and then they told me this:

We can do a full body check up in two years, and if your cholesterol goes down to below 4.0, we will honor the original $181/month price. But in order to do so, you must sign up for the policy today at $226/month. Further, we will be contacting your general practitioner to get your medical records for the past several years.

Great, another blood test in two years. Hmm, why do I feel completely unsatisfied with the answer? It’s almost as if I was scammed because I had to go through the uncomfortable process of giving blood. If I didn’t have to go through the process and just got a phone call a week later saying the price had increased due to their background check, I wouldn’t be too annoyed. Then the agent went on:

We will beat any and all providers. Thanks for your time and we’ll be in touch after we have received all your health records.

Don’t Expect To Get The Best Life Insurance Quote

Just like how car dealers advertise the lowest price on a car to lure you in, life insurance providers will quote you the lowest life insurance premium price to get you to commit to the application process.

If my insurance provider said a 25 year/$2M policy cost $226/month, I may not have bothered with the blood work or mostly likely have gone with a smaller policy to get the figure under $200/month. $226/month = $2,712 a year = $67,800 in life insurance premiums I’ll end up paying over 25 years.

Here are some quotes I got for smaller policies from my existing provider. They said I can always lower my amount and pay less in the future, but I can’t increase my amount. With their new quote, they are basically charging me for the price of a $2.5M, 25 year term policy.

Amount: $1M

Cost: 25 term years – $92/month, 20 years – $62/month

Amount: $1.5M

Cost: 25 years – $136/month, 20 years – $91/month

Amount: $2M

Cost: 25 years – $180/month, 20 years $120/month

Amount: $2.5M

Cost: 25 years – $224/month, 20 years – $149/month

Amount: $3M

Cost: 25 years – $269/month, 20 years $179/month

If you’re looking for life insurance, just expect the premium you are quoted to be higher by 20% – 40% after you do the blood work, if need. If the premium doesn’t rise, consider yourself lucky.

The silver lining about the process is that I didn’t have to leave my home, I got free blood work done, and I know I’m in top shape for 19 out of 20 health criteria they look for (they wouldn’t tell me the categories). Now I can focus on lowering my cholesterol to live a healthier life.

Shop Your Quote Around

Because I shop for life insurance once in a blue moon, I don’t know whether $226/month is a good or bad price. All I know is that it’s 25% higher than what I was originally quoted. Because I’ve been with USAA for almost 20 years, I just trusted them to give me the best quote possible. After all, members have either served their country in the military or are children of those who have served.

To find out whether my USAA quote was competitive, I went onto PolicyGenius to get various 25 year/$2M quotes and compare the results to my original $181/month quote. PolicyGenius is a life insurance marketplace that uses technology to get you the most custom quotes based on all your variables in one place. I’ve met both their founders multiple times and really like the pricing discovery they are providing for their consumers in an incredibly opaque industry.

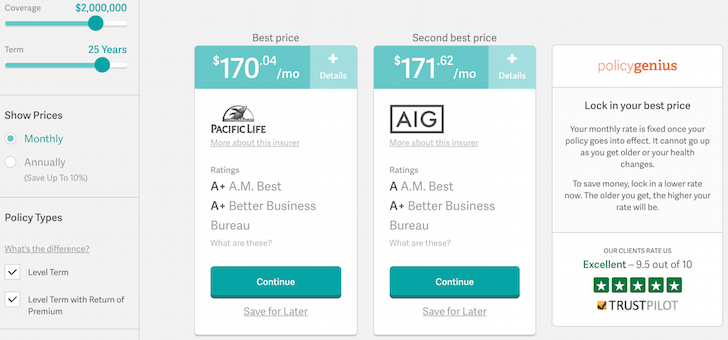

The process on PolicyGenius took two minutes, but it may take a couple minutes longer if you have a lot of health problems. They came back with 8 quotes, with the following two as the lowest and most appropriate: $170.04/month from Pacific Life and $172.62/month from AIG.

I’m glad that my original $181/month quote wasn’t too far out of line. Now I plan to either go with one of these two providers or use the quotes to have my current provider lower their price since they did say they will beat any price.

One Last Life Insurance Twist

There’s one good thing about being born before the internet was born. It’s hard for life insurance companies to know everything about you.

When I was living in Taipei in the early 1980s, I suffered from asthma. The air was terrible back then, and it still is now. One day I woke up with red spots all over my body and I couldn’t breath. I was rushed to the hospital, given an IV, and stayed there for at least one night. When I woke up the next morning, my entire body had turned red!

Not being able to breathe is a scary feeling, and I’m fortunate I haven’t had an asthma attack for over 30 years. A stronger immune system and a cleaner environment must have everything to do with it. Therefore, I would say I no longer have asthma, and will never get asthma again. But just in case, I do have an inhaler in my home.

I was curious to know how my life insurance premium would change if I said I had asthma 31 years ago with no asthma attacks since. Here is the second set of results from PolicyGenius:

Suddenly, my $226/month life insurance policy doesn’t look so bad! I assume USAA did all the due diligence they could to find the lowest price possible while still being able to make a profit. They wouldn’t tell me what the other 19 variables were they were checking for so I’m wondering whether I’m supposed to tell them about my asthma attack from when I was 9 years old.

I’m always going to believe that getting life insurance is the right thing to do if you start a family. Just make sure you get the appropriate amount of life insurance for the right price. The internet has helped create better pricing discovery so we don’t get ripped off. Stay healthy my friends! I’ll be making a decision about my new life insurance policy this week.

Readers, what are some other examples of bait and switch you’ve experienced when attempting to buy something? Should vendors be more clear? Why do you think life insurers are so opaque when it comes to their underwriting criteria? We know that for getting a mortgage, income, debt, equity, credit score, and a bunch of other things count to help folks prepare. Should we disclose more health information if the insurance providers do not ask?

The post Beware Of The Life Insurance Bait And Switch Tactic appeared first on Financial Samurai.

from Financial Samurai

via Finance Xpress

0 comments