How The SECURE Act Changes Your Retirement Planning

2:32 AM

The Setting Every Community Up For Retirement (SECURE) Act recently passed and it will go into effect for all Americans in 2020.

The goal of the SECURE Act is to make it easier for Americans to save for retirement and live comfortably in retirement. Based on the data, we know that the median and average American is severely lacking in retirement funds.

At the same time, we also know that the average American is truly living the good life by spending $61,224 a year of their $78,635 income. When you’ve got Social Security, a belief that the government will save you, and a YOLO mentality, it’s logical to live it up with your one and only life.

Just the other day, I decided to order a sangria at my favorite tapas restaurant instead of a plain lemon water because I was feeling the YOLO in my veins.

How The SECURE Act Changes Retirement Planning

The problem with new bills is that you’re never quite sure what the changes are and whether the changes will last long enough to matter. You could be doing the right thing for decades and then the government decides to move the goalpost. As a result, the fundamentals of saving for retirement should never change:

- Max out your tax-advantageous retirement accounts e.g. 401(k), IRA, 403(b), Roth IRA, SEP IRA, Solo 401(k)

- Save at least 20% of your after-tax and after tax-advantageous retirement account maximum contribution

- Generate extra income beyond your day job

- Get in the mindset of never expecting the government, your parents, or your rich aunt to save you

- Always have at least disaster insurance

No matter what happens with retirement laws in the U.S., so long as you do the above five things, you’ll probably be fine.

The SECURE Act changes your retirement planning strategy at the margin. Here are the five things to be aware of.

1) Required Minimum Distribution Starts at Age 72 from 70.5

For those of you who have followed my advice of building a healthy taxable retirement portfolio, good news! You can now wait until you’re 72 years old before being forced to withdraw money from your traditional retirement accounts.

Given our population as a whole is living longer, extending the RMD from 70.5 to 72 makes sense. We should be allowed to have our investments compound tax-free for a longer period to pay for our longer lives.

Those who turn 70½ on or after Jan. 1, 2020, are subject to the new rules and will have an extra year and a half before they need to start withdrawals.

Your goal: Amass a large enough taxable retirement portfolio so that you can wait until 72 to withdraw from your retirement funds. You want your retirement funds to compound tax-free for as long as possible. Once you start withdrawing from your retirement funds, withdraw the minimum amount necessary to keep your taxable income in the lowest tax bracket possible. Finally, live as long past 72 as possible.

2) Contributions Can Be Made To Your Traditional IRA After Age 70.5

If you are fortunate enough to still have the energy, ability, and desire to still have W2 income after age 70.5, you’ll now be allowed to contribute to a traditional IRA. Working beyond the traditional retirement age of 65 is one of the best ways to solidify your finances.

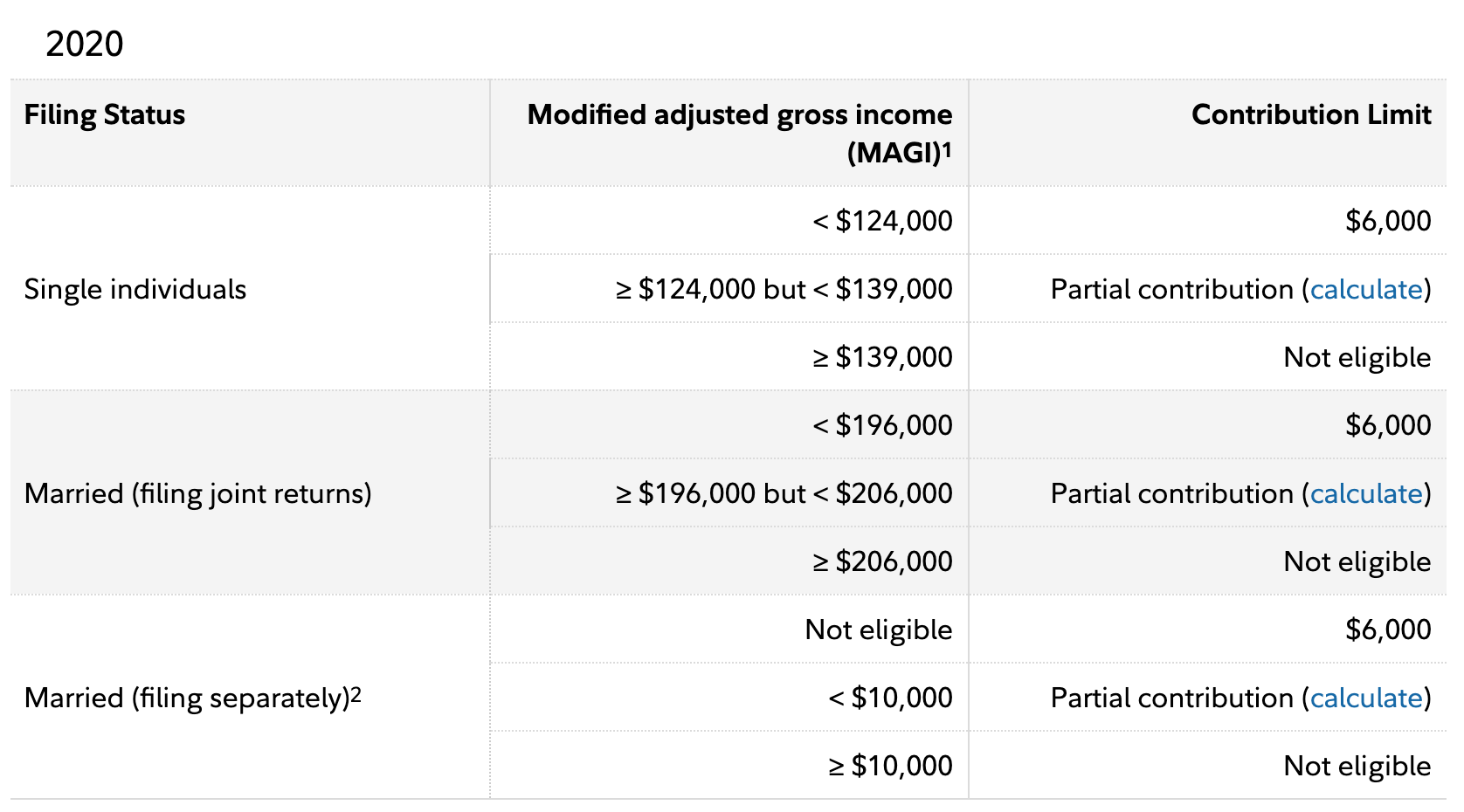

The maximum IRA contrition for 2020 is $6,000, the same as in 2019. The IRA catch-up contribution limit will remain $1,000 for those age 50 and older for a maximum possible IRA contribution of $7,000 in 2020.

Unfortunately, the government still doesn’t allow all Americans to contribute to a traditional IRA. For some reason, it believes that once a single individual makes over $139,000 a year in 2020, they no longer want or need to save for retirement.

It befuddles me that the government believes a 25-year-old making $150,000 in a high-cost city with tremendous student loan debt doesn’t have the same retirement benefits as everybody else.

It also makes no sense that once a married couple makes over $206,000, they aren’t eligible to contribute to a traditional IRA as well. $139,000 + $139,000 = $278,000, not $206,000. The government is either bad at math or doesn’t believe in equality.

Your goal: Save so much in your taxable and pre-tax retirement accounts that you don’t need a job after 70.5 to fund a traditional IRA. If you want to work in your 70s, that’s fine. But do so as a freelancer where you can set your own hours and rules.

3) No More Stretch IRA

A stretch IRA was an estate planning strategy that extended the tax-deferred status of an inherited IRA when it is passed to a non-spouse beneficiary. Theoretically, an IRA could be passed on from generation to generation while beneficiaries enjoyed tax-deferred and/or tax-free growth. That’s now gone thanks to the passage of the SECURE Act.

Under the new law, most beneficiaries will have to withdraw all the distributions from their inherited account and pay taxes on it within 10 years. Exceptions are made for spouses and the chronically ill or disabled.

For those who inherit an IRA after January 1, 2020, the stretch IRA is no more. For those who inherited an IRA before January 1, 2020, you can defer your tax liability as usual.

Your goal: Talk to an estate planning lawyer. He or she will tell you things that you probably have not considered before, like the GRAT. Set up a revocable living trust if you have children. At the very least, have a clearly written will. Estate planning is an act of kindness for your beneficiaries.

4) Watch Out For Annuity Options In Your 401(k)

Annuities, like whole life insurance, is a very profitable product for financial companies. Annuities are insurance products that turn a lump sum investment into a lifetime of guaranteed income.

Besides the hidden cost of owning an annuity, one of the concerns companies had for offering them in a 401(k) plan was the viability of the annuity provider. What if it went bust? Think about other products you own such as life insurance, house insurance, and car insurance. If your insurance company got into financial trouble, as some did during the 2008-2009 financial crisis, they might not pay out.

The SECURE Act increases legal coverage for employers, just in case their employees sue them because their annuity provider goes out of business and does not pay.

If you are an employer, you’d be foolish to offer an annuity option in your 401(k) plan, despite the increased legal protection.

No employee is going to join an employer or stay at an employer because of its great annuity option in the 401(k). Instead, when it comes to retirement benefits, the #1 reason why an employee might stay is due to generous 401(k) matching and profit sharing.

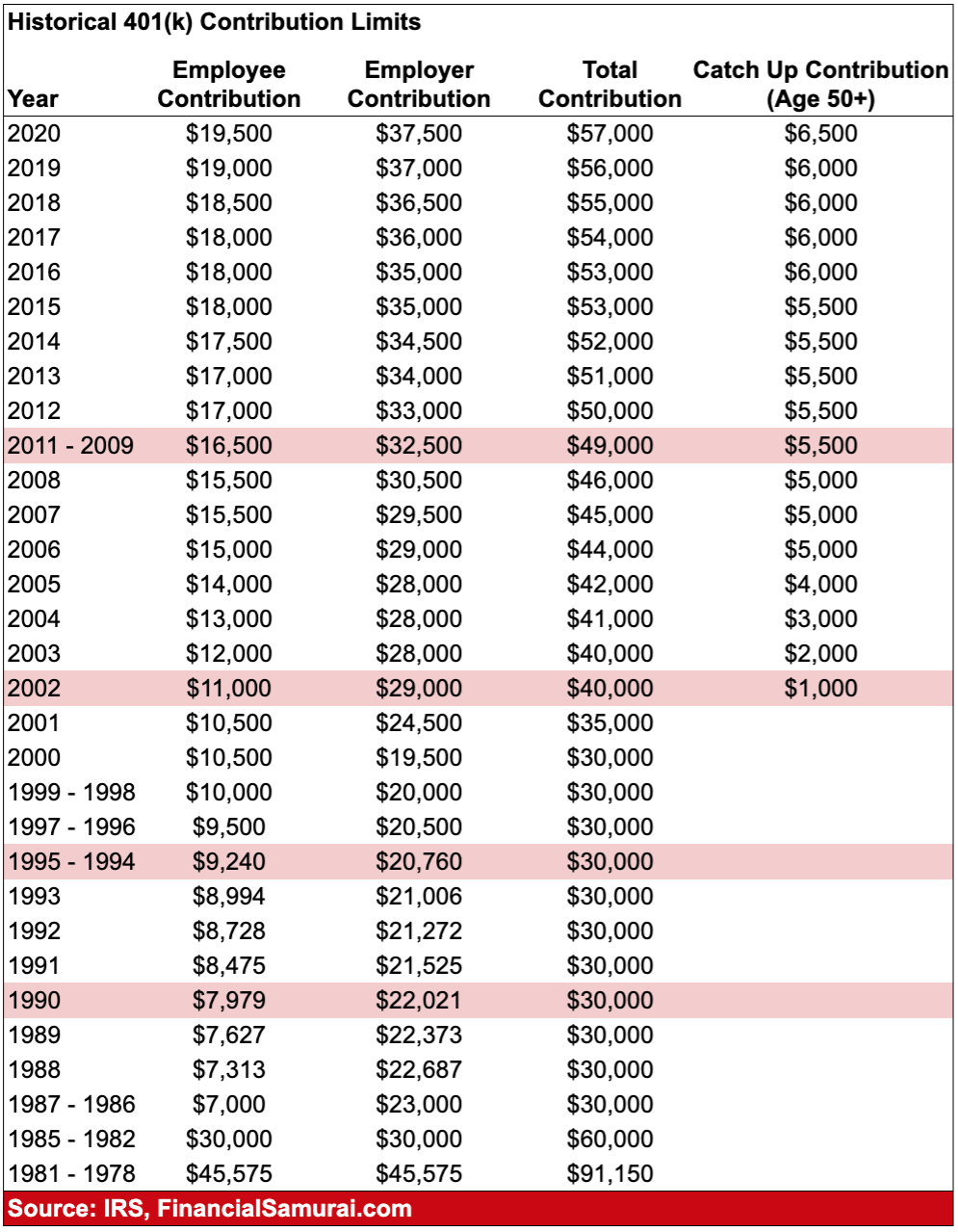

In 2020, the maximum 401(k) contribution is not only $19,500 by the employee. In 2020, the total maximum 401(k) contribution is $57,000 because the employer has the ability to contribute up to $37,500 to your 401(k) as well.

Your goal: Find an employer who will contribute the most money to your 401(k). If you want to work at a sexy startup, know that you are not only taking a salary cut for lottery tickets, you’re likely also giving up employer retirement contributions as well. Skip annuities because they are complicated to understand, cost more than they need to, and take away your liquidity and flexibility.

5) 401(k) Accounts May Become More Prevalent For Part-Time Workers Or Employees Of Small Businesses

The SECURE Act makes it easier for small businesses to offer retirement plans by reducing their cost of providing a 401(k) plan. The cost is reduced by allowing small businesses to band together to get something similar to a group discount. It’s similar to the idea of getting a group discount for health insurance or pooling your capital to buy commercial real estate.

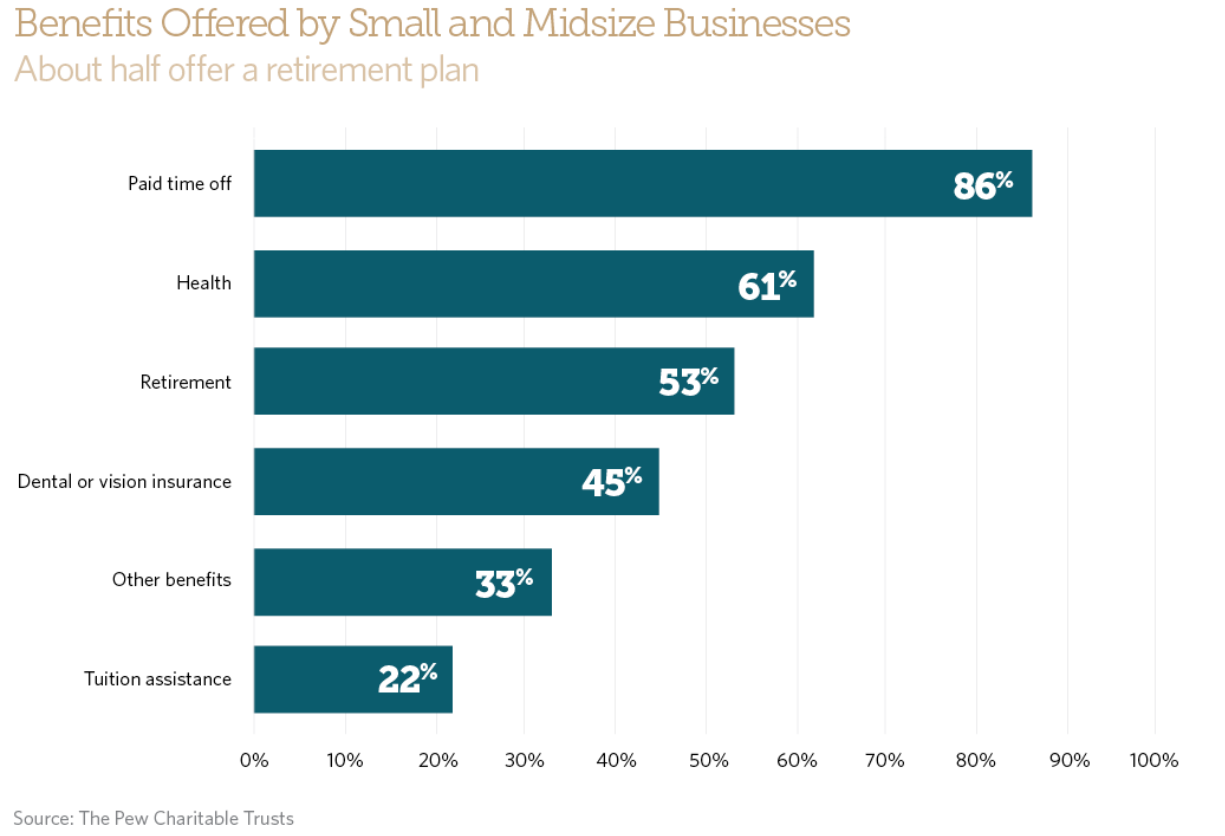

Below is some interesting research from the Pew Research Group about benefits businesses with 5 – 250 employees provide. As you can see, only 53 percent of small businesses provide retirement benefits. Employers that do not offer plans pointed to the financial cost (37 percent) and organizational resources (22 percent) needed to start a plan as barriers. One-sixth said they do not offer a plan because their employees are uninterested.

Perhaps the most exciting thing about the SECURE Act is that it now requires employers who offer 401(k)s to expand its access to part-time workers who work at least 500 hours a year for three consecutive years or 1,000 hours for one year.

To put these hours into perspective, a full-time worker who works 40 hours a week, will work 2,080 hours a year. Therefore, working 1,000 hours for one year is a piece of cake! We’re talking only an average 20-hour workweek.

At the margin, the offering of more 401(k) plans to part-time workers will probably further increase the rise of part-time and remote workers. As a result, I foresee a continued demographic shift towards lower cost areas. I’m pretty sure that by 2030, there will be more 1099 workers than W2 workers.

Your goal: Find part-time and remote work opportunities with employers who offer a 401(k) plan with a match. Because there is so much dead time working a full-time job with one employer, if you are reasonably efficient, you can make much more money working multiple part-time jobs.

6) 529 Plans Get More Flexible

After the Tax Cuts and Jobs Act passed in 2017, owners of a 529 plan could not only use the funds from the plan to pay for qualified college expenses, owners of the plan could also use up to $10,000 of the funds annually for K – 12 expenses.

With the passage of the SECURE Act, a 529 plan can now also be used for Apprenticeship Programs and qualified expenses including fees, books, supplies, and equipment. Further, 529 plan funds can be used to pay for principal and interest of qualified education loans as defined in IRC Section 221(d).

Finally, an additional $10,000 may be distributed as a qualified education loan repayment to satisfy outstanding student debt for each of a 529 plan beneficiary’s siblings.

Your goal: While a college degree is getting devalued each year, it’s still worth opening up a 529 plan if you have children. Your contributions grow tax-free and if you don’t end up using all the funds, you can change the beneficiary over to someone else. When you’ve got to save for retirement and pay for your children’s future, you might as well take advantage of tax breaks to make doing both as efficiently as possible.

The SECURE Act Is A Net Positive For Retirement

Our do-little and highly discriminatory government has finally done something financially positive for millions of Americans. Let’s just hope the SECURE Act stays in place for a long time and we see further bills that make saving for retirement easier for all.

If I was President, I’d certainly propose to raise the traditional IRA income limit to at least $250,000 / $500,000 for single and married people. By doing so, more Americans who live in high-cost areas could also benefit.

Use the SECURE Act as motivation to always max out your 401(k) and traditional IRA if eligible. Then do your best to find a better way of working now that 401(k)s will be offered to more types of employees.

Even though the government has taken a small step to help us out, let us never rely on the government to save us. I have no doubt retirement rules will eventually change again.

Looking for a free retirement planning tool? Sign up for Personal Capital to track your net worth, analyze your portfolio for excessive fees, and make sure your retirement is on track with their Retirement Planner. I’ve used the free tool to track my finances since I retired in 2012. There is no rewind button in life. Make sure your finances are in order.

Readers, anything else in the SECURE Act you’ve found helpful to your retirement planning? What else should we be doing with the passage of the SECURE Act?

The post How The SECURE Act Changes Your Retirement Planning appeared first on Financial Samurai.

from Financial Samurai

via Finance Xpress

0 comments