Income Limit For Maximum Social Security Tax 2020

2:26 AM

I’ve got some good news and I’ve got some bad news.

For those of you who believe the government is efficient and benevolent, the good news is that the income limit for maximum Social Security tax rises to $137,700 in 2020.

Raising the income limit for Social Security tax from $132,900 in 2019 to $137,700 in 2020 brings in more funds, thereby increasing the viability of our national pension system.

It is estimated that Social Security’s long-term unfunded liability is now $43 trillion, up from $34 trillion last year. The fiscal gap equates to an estimated 33 percent underfunding. In its current form, citizens eligible for Social Security will only be able to collect ~70% of what is promised on their statements.

For those of you who believe you can manage your money better than the government, the bad news about raising the income limit for Social Security tax is that we might be throwing good money after bad. Raising the income limit by $4,800 or 3.5% should be concerning.

Just compare the 3.5% income limit increase to the 1.6% Cost of Living increase (benefits received) for Social Security recipients. The spread helps the solvency of Social Security, but it is clear we’re all at risk when it’s time for us to collect.

The best way to view Social Security is to never expect it to ever payout. The new three-legged stool for retirement dictates you must only depend on you (pre-tax savings), you (taxable investments), and you (extra work).

Explaining Social Security Tax

The Social Security tax is a federal tax imposed on employers, employees and self-employed individuals. It is used to pay the cost of benefits for elderly recipients, survivors of recipients, and disabled individuals (OASDI Insurance). OASDI stands for old age, survivors, and disability insurance tax.

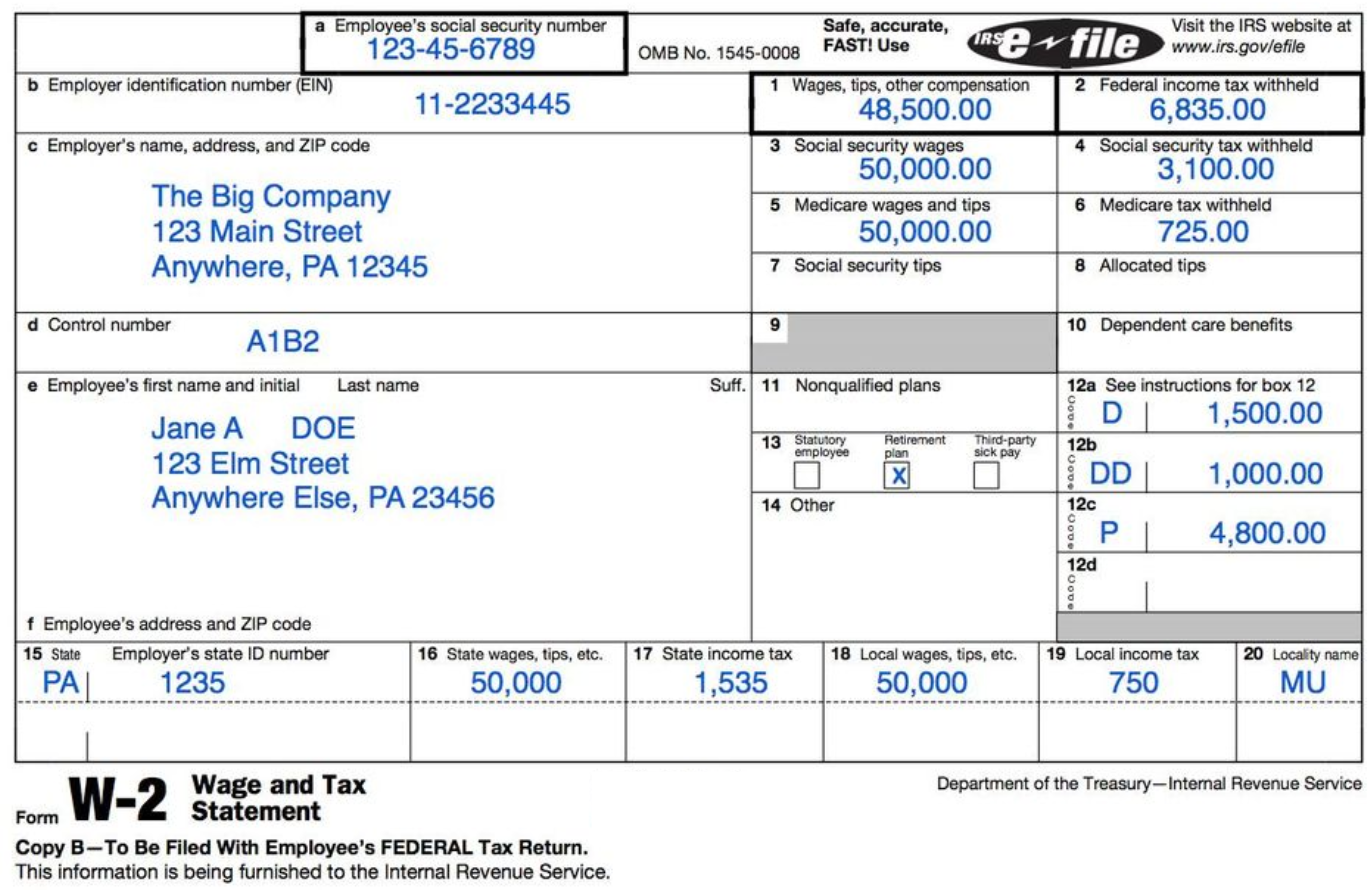

Social Security tax is a payroll tax that is automatically withheld on your wage and tax statement each pay cycle. Below is a typical Wage and Tax Statement that shows Social Security tax withheld in box 4 and Medicare tax withheld in box 6.

The Social Security tax rate is 12.4% – 6.2% withheld from the employer and 6.2% withheld from the employee.

The Medicare tax rate is 2.9% – 1.45% withheld from the employer and 1.45% withheld from the employee.

The total Social Security + Medicare (FICA) tax rate is 15.3%. If you are self-employed, you must pay the full 15.3%, but you can take a deduction for half this amount.

Unfortunately or fortunately, there is no maximum on Medicare tax, but there is an additional Medicare tax of 0.9% for high-income taxpayers with earned income of more than $200,000 ($250,000 for married couples filing jointly)

The Maximum Social Security Tax Amount And Benefits

Given the new income limit for Social Security tax is $137,700 for 2020 and the Social Security tax born by the employee is 6.2%, the maximum Social Security tax payable by an employee is $137,700 X 6.2% = $8,537.40.

The maximum Social Security benefit for someone retiring at full retirement age in 2019 is $2,861 and should go up 1.6% or so in 2020. The average Social Security benefit is closer to $1,450 a month. Receiving the average $17,400 a year in Social Security benefits is good supplemental income. But it’s not enough to live a comfortable retirement lifestyle in most parts of the country.

As a result, it’s vital that we all aggressively fund our tax-advantageous retirement plans and taxable investment portfolios.

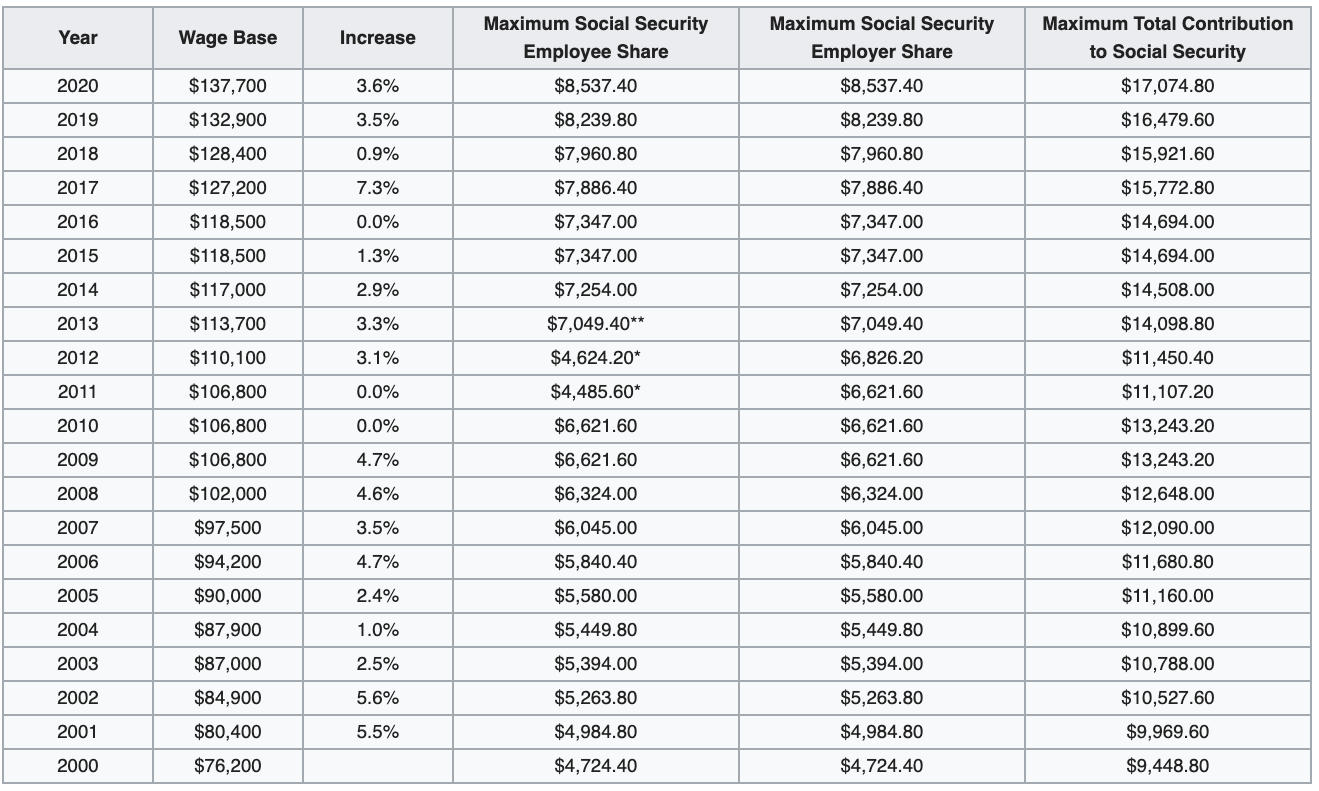

To get some perspective, here are the maximum wages subject to Social Security since 2000.

Based on the income limit increase trend, I expect the average increase per year to be around 3%, forever. By 2030, the income limit for Social Security tax will be $185,000 if we assume a 3% compound increase.

Self-Employment Tax Is Painful And Unfair

The fact that a self-employed person or small business owner has to pay the full 12.4% Social Security tax and the full 2.9% Medicare tax is a raw deal.

The self-employed person and small business owner are not getting double the Social Security or Medicare benefits. The extra 7.65% tax (6.2% + 1.45%) on operating profits is essentially a business expense. It is an extra cost of being self-employed or doing business, and is, therefore, deductible.

As an employee, you might feel happy about not having to pay the extra 7.65% tax. However, know that there’s no free lunch. If your employer didn’t have to pay Social Security and Medicare tax, you might have better benefits or a higher salary.

How To Pay Less Social Security Tax

As an employee, there really is no workaround to paying less Social Security tax. The only way you’ll feel better about paying Social Security tax is when your income surpasses the Social Security tax income limit for the year.

For example, let’s say you make $237,700 in taxable income for 2020 as an employee. $100,000 of your income will not be subject to Social Security tax. As a result, the after-tax income you receive on the $100,000 above $137,700 will increase by $7,650.

As an employer, the only way to reduce Social Security tax is to pay your employees less. Same thing as a self-employed person.

If you own an S-Corp, a common strategy was to pay yourself as low a wage as possible to pay less self-employment tax and pay as much of your profits in distributions as possible to avoid paying self-employment tax. But I think this strategy is going away with new tax reform.

If you want to reduce your chance of an audit, it’s probably best to pay yourself at least the maximum income limit for Social Security tax so the government knows it’s getting theirs. You can then figure out a way to reduce your taxable income with strategic business expenses, if you have the revenue and expenses to do so.

The best way to not pay Social Security and Medicare tax is to not earn W-2 or 1099 income. Instead, generate investment income. Investment income isn’t subject to Social Security withholding and it is taxed at a lower long-term capital gains tax rate.

Don’t Expect To Receive Social Security Benefits

Treat Social Security as an expense to help support older generations who paved the way for your success. If you end up receiving Social Security benefits, then wonderful. It will truly feel like bonus money.

If you don’t end up receiving Social Security benefits, then all the same. You helped your elders and never expected to receive any benefits in the first place.

Readers, are you for or against Social Security? Anybody currently receiving Social Security benefits who don’t need them? What are your suggestions for fixing Social Security so that everybody gets taken care of equitably?

The post Income Limit For Maximum Social Security Tax 2020 appeared first on Financial Samurai.

from Financial Samurai

via Finance Xpress

0 comments