The Average Cost Of Family Health Insurance Is Now Outrageously High

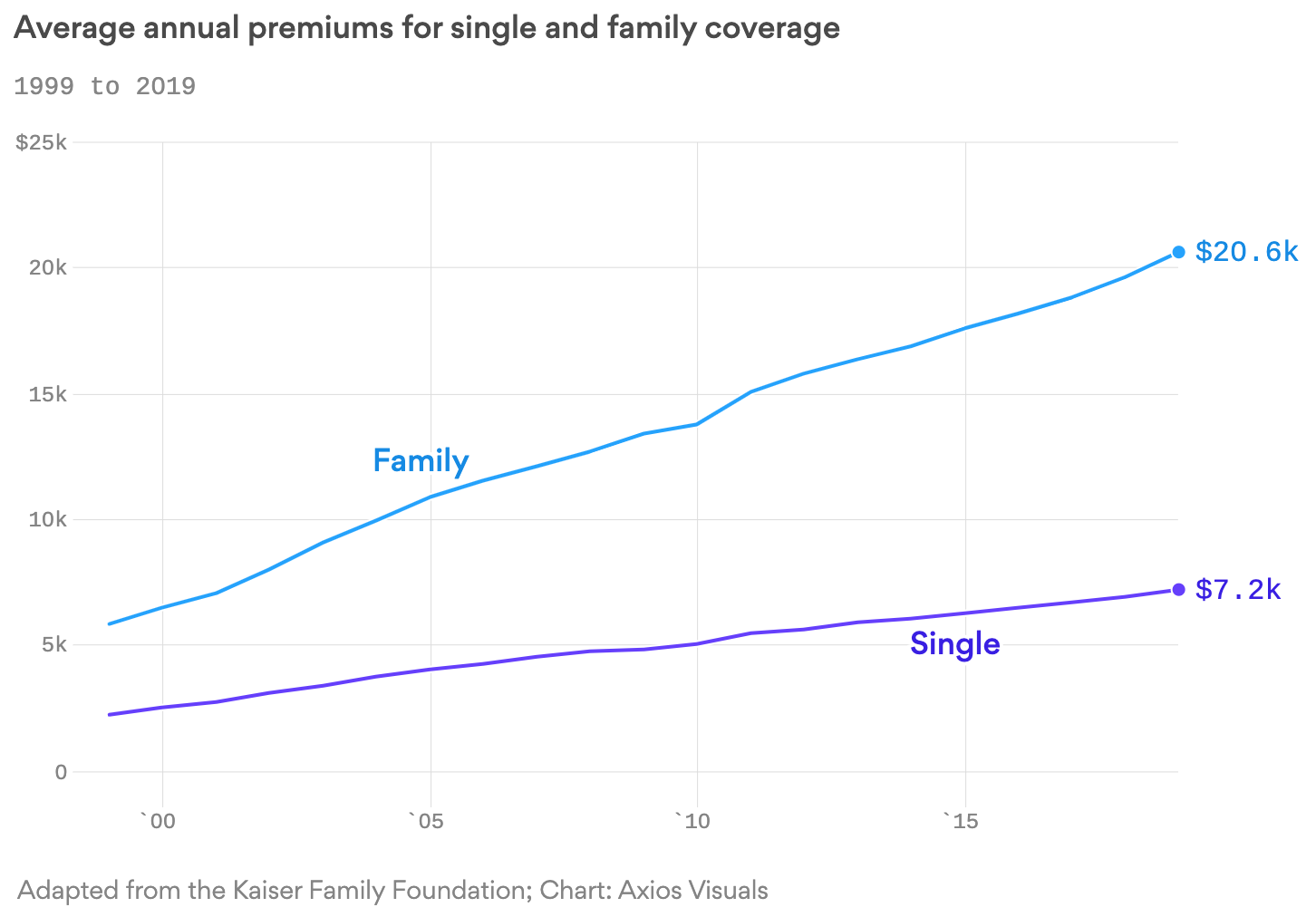

10:14 AMAccording to the Kaiser Family Foundation, the average cost of family health insurance offered by companies is now a whopping $20,576 a year, or $1,714.66 a month. Employers paid for 71% of that cost on average.

Meanwhile, the average premium for single workers was $7,188 a year, or $599 a month. Employers covered 83% of that cost on average.

The KFF surveyed over 2,000 companies.

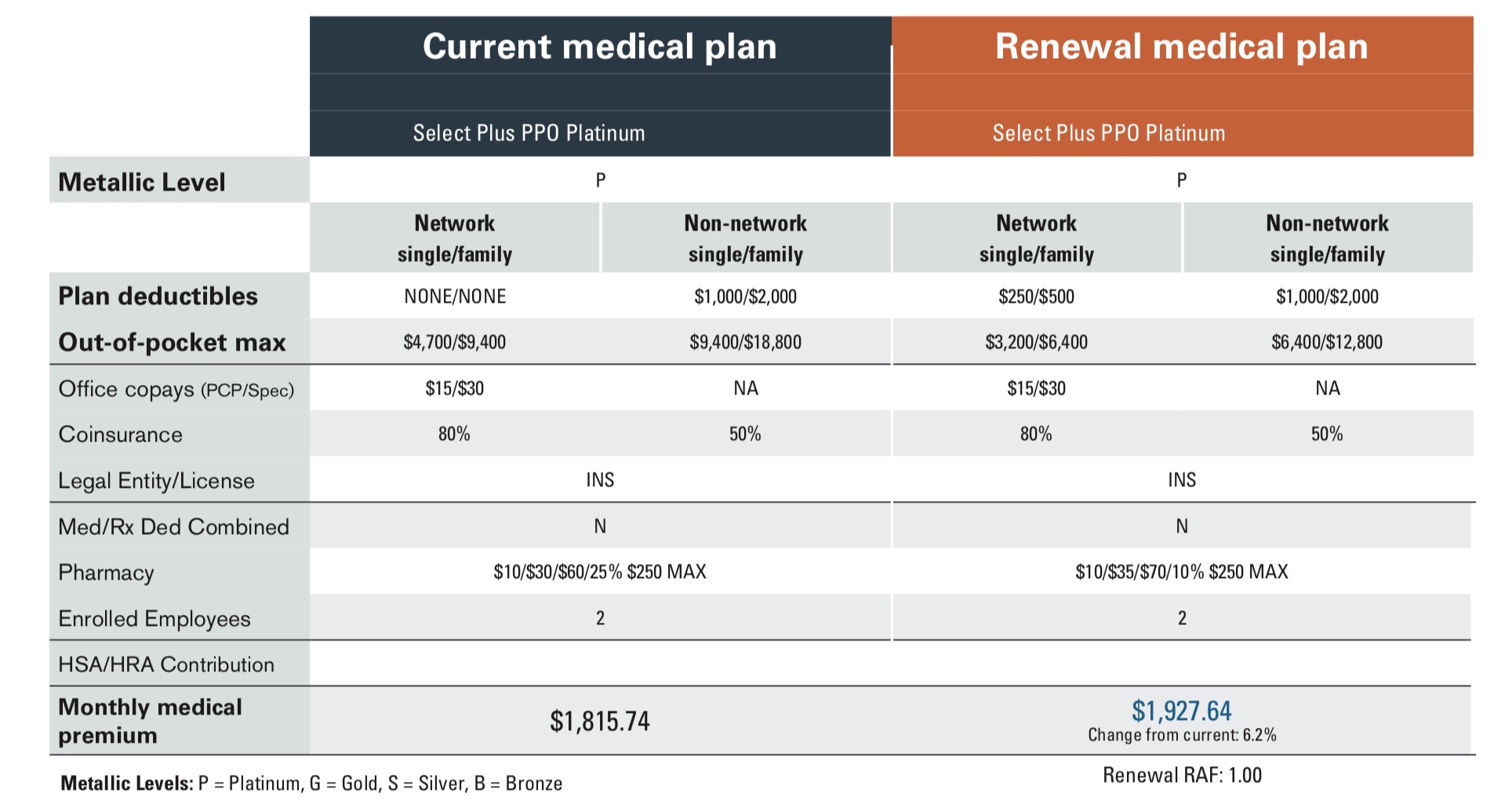

If they had asked us what we paid, we would have brought up the average because our health insurance cost is jumping by 7% to $23,131.38 a year, or $1,927.64 a month for a family of three! Previously, we were paying “only” $21,788.88 a year, or $1,815.74 a month.

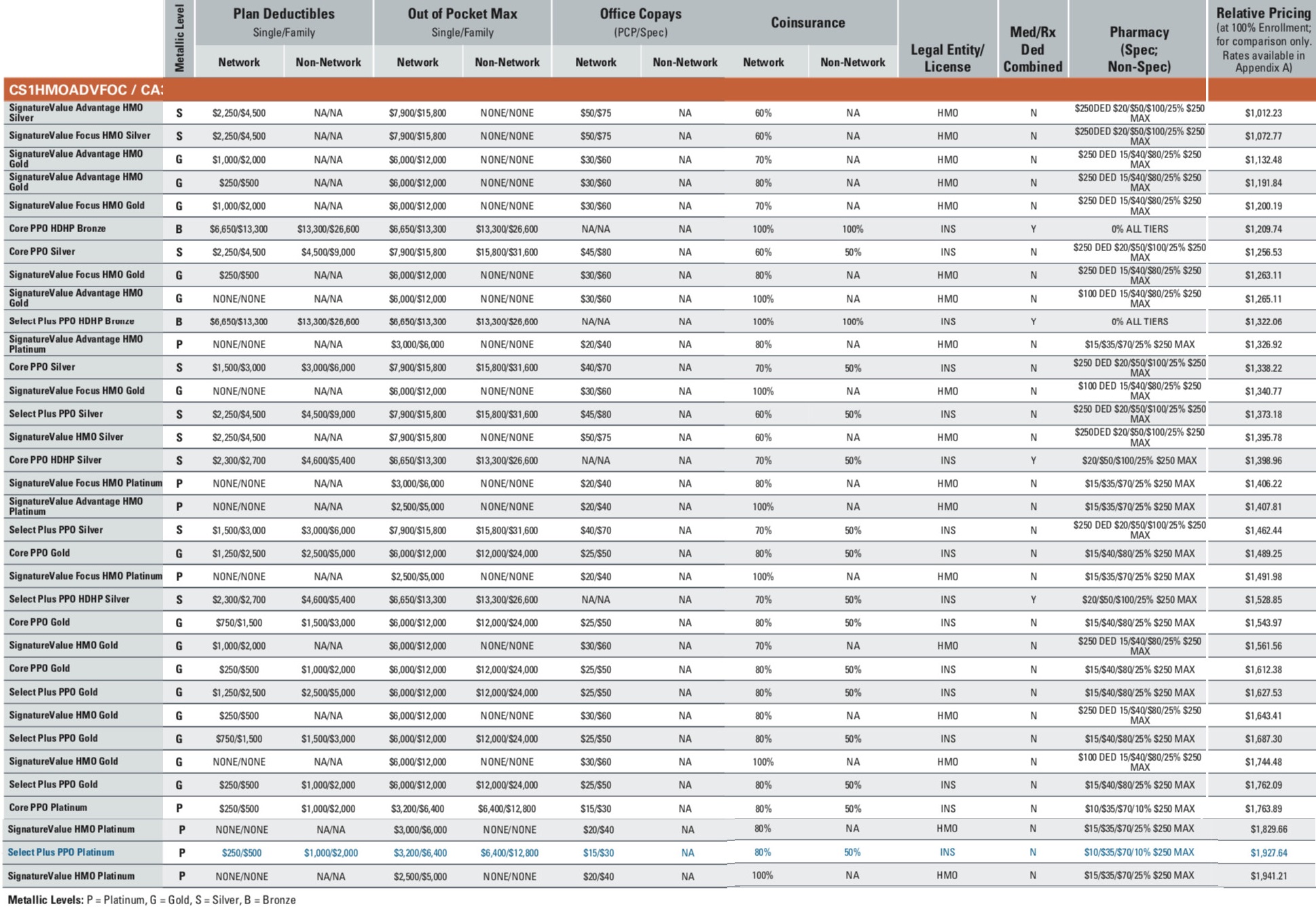

With one child we have a PPO Platinum plan with a $250/$500 deductible (single/family), a $3,200/$6,400 out-of-pocket max (single/family) and 80% co-pay insurance.

The Average Cost Of Health Insurance Is Unsustainable

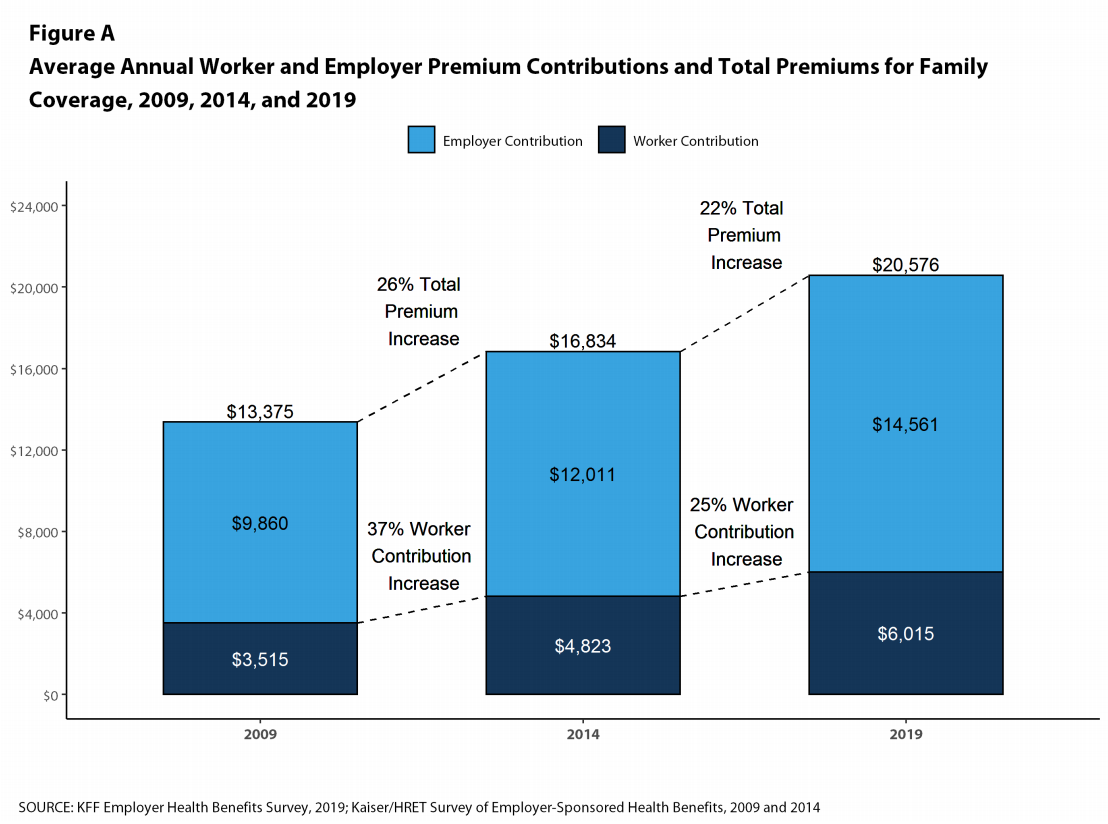

Despite workers’ earnings rising roughly 26% from 2009 to 2019, healthcare deductibles rose by 162% over the same time span. In other words, employees are getting squeezed. It is only logical that companies not pay employees as much if they have to pay for ever-increasing benefits.

Below is a list of other items that have inflated quite drastically over time. If you want to save on costs, then you should stay as healthy as possible, don’t go to college, don’t have kids, and be a homeowner.

Out of curiosity, I asked our healthcare agent how much our healthcare premiums would go up if we had a second child. He said adding a second dependent under age 15 to our PPO Platinum plan would cost an extra $440 a month for a total of $2,360 a month or $28,320 a year!

Using a 25% effective tax rate, our family needs to earn $37,760 a year just to pay for our healthcare premiums. Using a 4% return or withdrawal rate assumption, we would need to accumulate or allocate $944,000 in investments to cover our healthcare premiums if we continue to stay unemployed.

If you don’t think you need at least $2 million to retire early with kids, you are seriously fooling yourself. The math doesn’t lie folks. $1 million needs to be set aside for healthcare costs that are growing by 5% – 7% a year. The other million is used to pay for basic living expenses.

Healthcare costs are going to be your largest unavoidable expense. You can save on tuition by just going to public grade school and public university. Housing costs can be controlled if you pay off your mortgage or relocate to a lower cost area of the country. But there’s nothing you can do about runaway healthcare expenses unless you retire in or near poverty in order to get subsidized healthcare.

Analyzing Our Health Insurance

Given both my wife and I don’t have employers to subsidize our healthcare expenses and we earn more than 400% of the Federal Poverty Limit ($83,120) from our retirement portfolio, we do not qualify for goverment healthcare subsidies either.

Once my wife stopped working in 2015, we decided to just get the best plan possible so we could minimize health insurance headaches and rest easier knowing we can get the best possible care. However, healthcare costs are now starting to push the upper limits of our comfort zone.

One solution to lower our healthcare cost is to downgrade from a Select Plus PPO Platinum plan to a Select Plus PPO Gold plan to save roughly $160 a month in premiums. However, if we do so, our out-of-pocket max rises from $6,400 to $12,000.

Given we have a 2.5-year-old, we still don’t know for sure how his overall health will be. So far he’s doing OK, but we won’t really know until maybe after he’s five years old what other health issues he may have.

Further, if we have a second child, having our current plan saves us more money given the lower out-of-pocket max and 80% co-insurance. You can’t just get a better plan to cover a big healthcare expense and then downgrade to save on premiums once that expense is covered the next month. These plans are year-long contracts.

We analyzed this comprehensive list of family healthcare plans arranged by price. You’ll have to zoom in on the graph to see the details. I’m curious to know which plan you’d choose and why if you are a relatively healthy family of three with no chronic illness or pre-existing conditions. Your child is 2.5-years-old and you may have a second child.

The Core PPO Platinum plan seemed like a great alternative, but our agent informed us it has a much smaller network of doctors which excludes some of our current doctors. We’d also have a similar problem of a smaller network of doctors if we switched to an HMO plan, and would require PCP referrals for specialist care, exams and tests.

How Do Retirees Afford Healthcare?

I’ve been scratching my head a lot, wondering how other early retirees / long-term unemployed afford healthcare insurance. Therefore, I went and asked a bunch of people and this is what they said:

1) Have you looked into Liberty Health Share? It’s a Christian based plan. It’s equivalent to a PPO with a $2250 deductible/ max out of pocket for only $499 a month for my family of four! I’ve had it for four years and love it.

2) I have Liberty Health Share as well. Last year we had our first child and paid only a 1,500 deductible. It was amazing. What impressed me from the very beginning was you could get a person on the phone right away and they actually cared and tried to help you with whatever you were calling about.

However over the past 6 months or so the service has gone downhill. They no longer try to pay claims within 60 days and sometimes it seems like it’s an absolute nightmare to get them to do their jobs. Still it’s better than I remember from Blue Cross Blue Shield so we are holding on and hoping things get better again.

Note: Dealing with insurance companies who may not pay the claims is the nightmare I’m trying to avoid by getting a better healthcare plan. I really don’t have the time or desire to deal with insurance BS.

3) My wife works and we are all on her company’s healthcare plan. We pay about $550/month for our family of three for a Gold-level plan. Our estimated net worth is $2.5 million.

4) Both of us are retired and live off about $38,000 a year from our $2 million investment portfolio and part-time work. We live in a very low cost area of the country where you can buy a house for $250,000. We are a family of five and qualify for tremendous healthcare subsidies given our income is only 130% of the Federal Poverty Limit. We pay less than $120 a month for a Bronze health plan under the ACA. Our deductible is $15,000.

5) We are a childless couple who live on about $28,000 a year. Our portfolio is about $1.1 million and we live in a middle-to-higher cost area of the country. My wife has a pre-existing condition that requires constant medical supervision. Our household income is at about 150% of FPL, so we only have to pay about $3,200 a year for our health insurance under ACA. We make an extra ~$10,000 a year in side income working online.

6) We started a business so that we can deduct our health insurance costs. Our business income comes from doing various consulting work online and offline. Last year we pulled in roughly $40,000 of consulting income and deducted $24,000 of health insurance expenses for the three of us. Effectively, we’ve lowered our health insurance expenses by roughly 20%. We also make roughly $90,000 a year from our various investments.

For most retirees, the solutions to comfortably afford healthcare insurance are to either get on your working spouse’s healthcare plan or earn 200% or less of the Federal Poverty limit to get tremendous subsidies from the government. Even earning between 300% – 400% of FPL, you’re only required to pay at most 9.86% of your gross annual income to healthcare premiums under the ACA.

The high cost of healthcare also makes me wonder whether more workers will be hesitant to retire early as well. I guess so long as you’re willing to earn less than 400% of FPL in retirement, healthcare is manageable.

Unless we want to incur a tremendous tax bill by selling our income-generating assets, the only way our family can immediately reduce our health insurance expense is if at least one of us goes back to work. If the new employer pays 71% of the annual cost, then we would be getting a healthcare subsidy of $16,423 a year or $1,368 a month.

It might very well be time to dust off the old resume!

Readers, how much do you pay for health insurance a month and how much does your employer pay? Do you think it’s morally OK to get healthcare subsidies if you are a millionaire? If you don’t work, how do you afford such egregious healthcare costs?

The post The Average Cost Of Family Health Insurance Is Now Outrageously High appeared first on Financial Samurai.

from Financial Samurai

via Finance Xpress

0 comments