The Maximum 401(k) Contribution Limit For 2020 Goes Up By $500

2:29 AM

Good news! It just got a little bit easier for everyone 40 and under to become 401(k) millionaires by the time you turn 60.

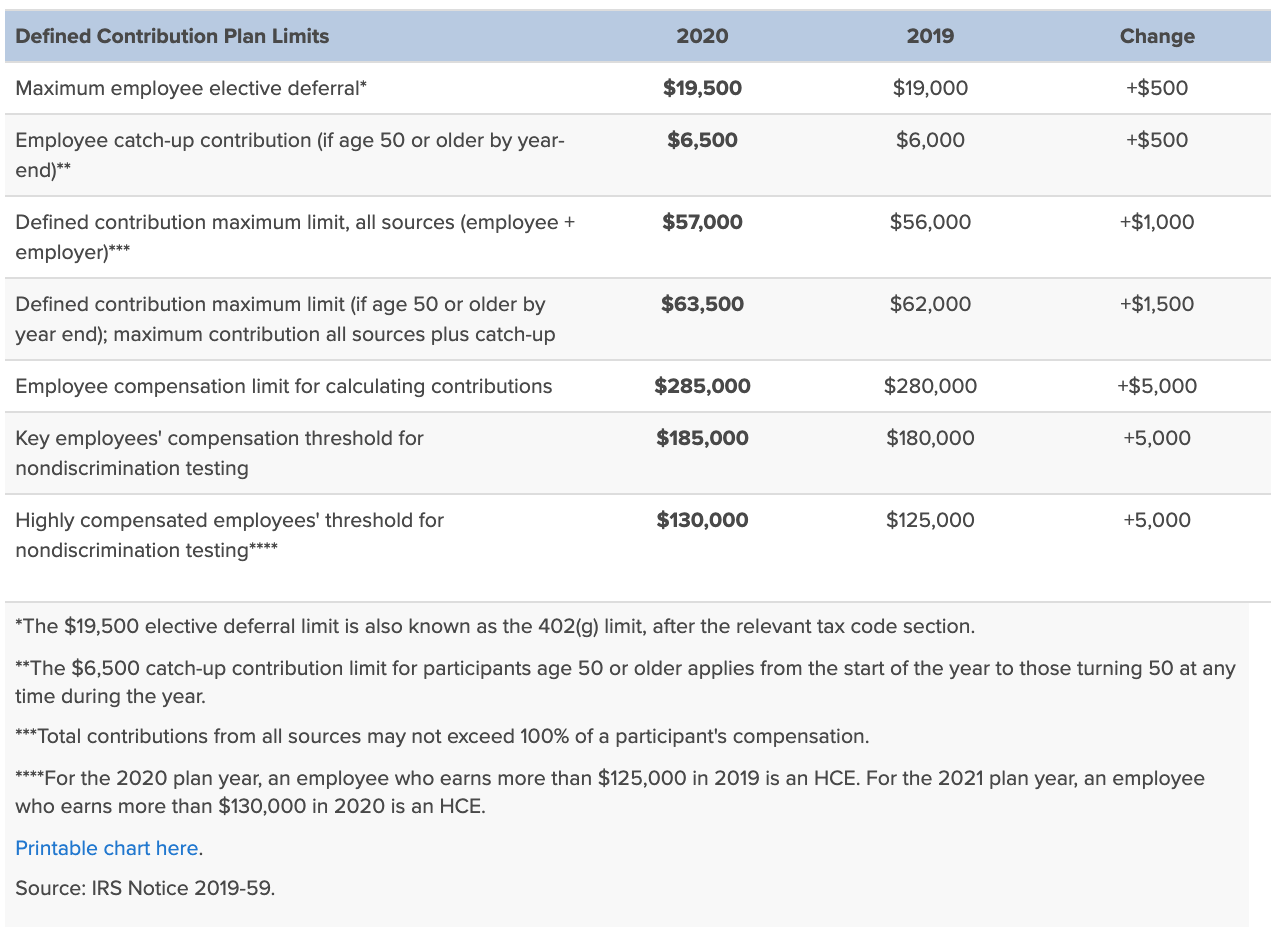

The maximum 401(k) contribution limit for 2020 goes up to $19,500 from $19,000 in 2019. Hooray!

Meanwhile, the combined employer and employee contribution limit rises by $1,000 to $57,000. In other words, your employer in 2020 can contribute up to $37,500 to your 401(k) in terms of a match or a profit share.

For participants ages 50 and over, the additional “catch-up” contribution limit will rise to $6,500, up by $500.

Curiously, the limit on annual contributions to an IRA remains unchanged at $6,000. The additional catch-up contribution limit to an IRA for individuals age 50 and over remains $1,000.

Overview Of The Maximum 401(k) Contribution Limit For 2020

Below is an overview of the 401(k) contribution plan limits for 2020 compared to 2019.

According to Fidelity Investments, one of the largest administers of 401(k) plans in America, employees’ average 401(k) contribution rate is now 8.8 percent of their pay, nearly a full percentage point higher than 10 years ago.

If we use the median household income of roughly $63,000, that equates to $5,544 in annual 401(k) contribution per household. Add on an average 3 percent salary match, and we’re talking another $1,890 employer 401(k) contribution for a total of $7,434.

Contributing between $5,000 – $8,000 a year in a household’s 401(k) is not bad. However, I encourage folks to force yourself to contribute the maximum amount allowed to your 401(k) each month.

Although maxing out your 401(k) might be painful, depending on your income, you will learn to live on less and figure out new ways to make more money if necessary.

Contributing the maximum to your 401(k) should be a default automatic assumption so you can then aggressively build your critical after-tax retirement portfolio for passive income.

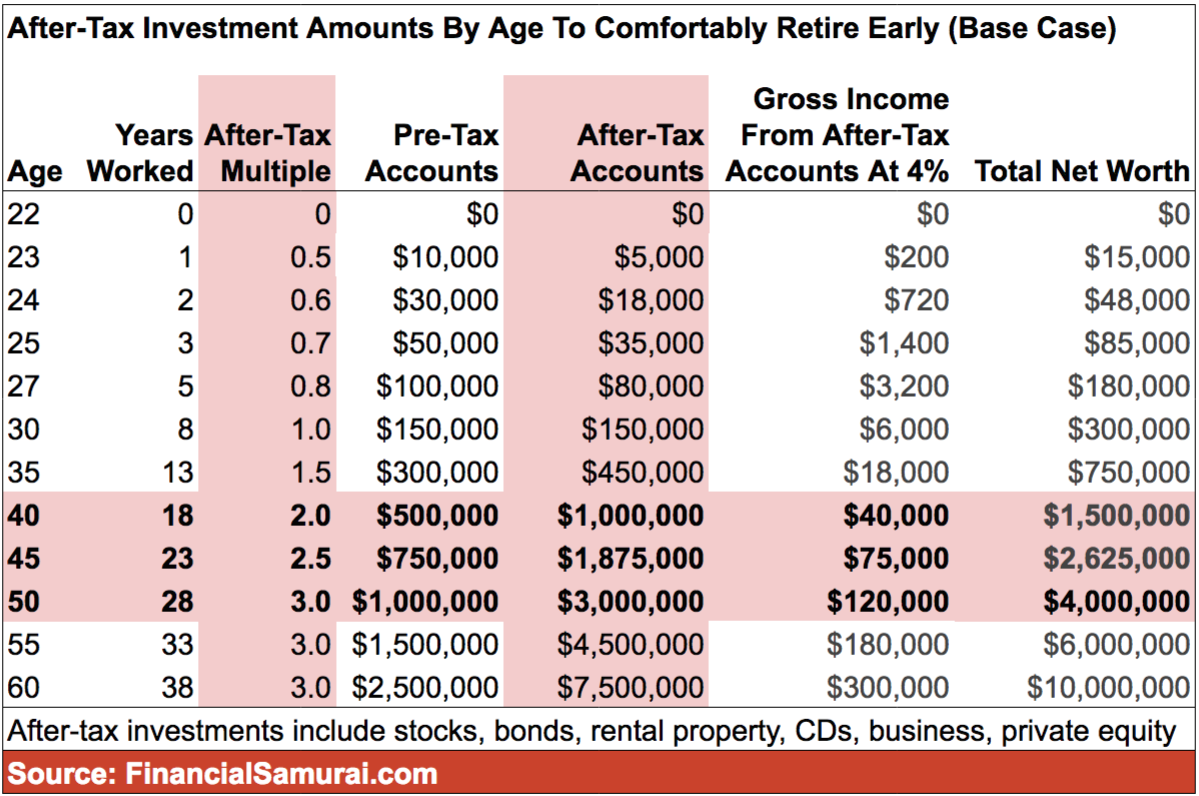

Pre-Tax And After-Tax Retirement Portfolio Overview

Below is my base case guide for how much you should accumulate in your pre-tax accounts (401(k), IRA, etc) and after-tax accounts by age if you want to comfortably retire early.

Your after-tax accounts can include your online brokerage account, rental property, venture debt, private equity, royalty income, side business income, real estate crowdfunding, royalty income and more.

Ideally, you want to accumulate an after-tax retirement portfolio that is 3X your pre-tax retirement portfolio. In other words, your after-tax accounts are much more important than your 401(k) for the purpose of generating livable passive income.

If you can ultimately generate a net worth of between $1,500,000 – $4,000,000 by the time you hit 50, you should be good to go for the rest of your life. The net worth spread accounts for various costs of living and lifestyles.

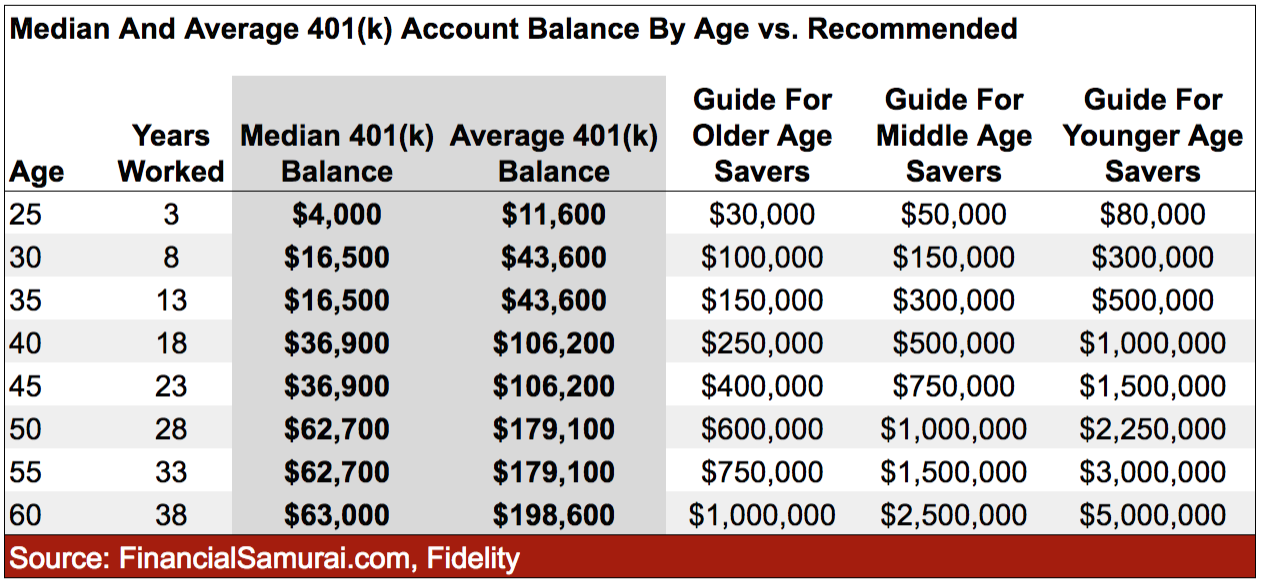

The Median And Average 401(k) Balances By Age

Perhaps you are thinking that becoming a 401(k) millionaire by 50 is a stretch, despite historical investment returns and maximum contribution increases. You would not be wrong if you compare yourself to the median and average person in America.

By age 50, the median 401(k) balance is $62,700 and the average 401(k) balance is $179,100 according to Fidelity.

By age 60, the median 401(k) balance only increases by $300 to $63,000 and the average 401(k) balance increases by $19,500 to $198,600.

The overall average 401(k) balance is $106,00 as of 2Q2019, up 2% from $104,000 in 2Q2018.

Why the median and average 401(k) balances hardly grows from age 50 to 60 is hard to say. Perhaps the reasons are due to increased medical expenses and skyrocketing educational expenses that reduce a family’s ability to save for retirement.

Whatever the case may be, if you only have about $200,000 in your 401(k) by 60, you’re kind of screwed, especially if you don’t have a larger after-tax investment account or pension.

You do not want to be the median or average American! Not only does the typical American have an underfunded retirement account, but the typical American is also quite unhealthy.

You can be broke and healthy or rich and unhealthy. But please don’t be broke and unhealthy!

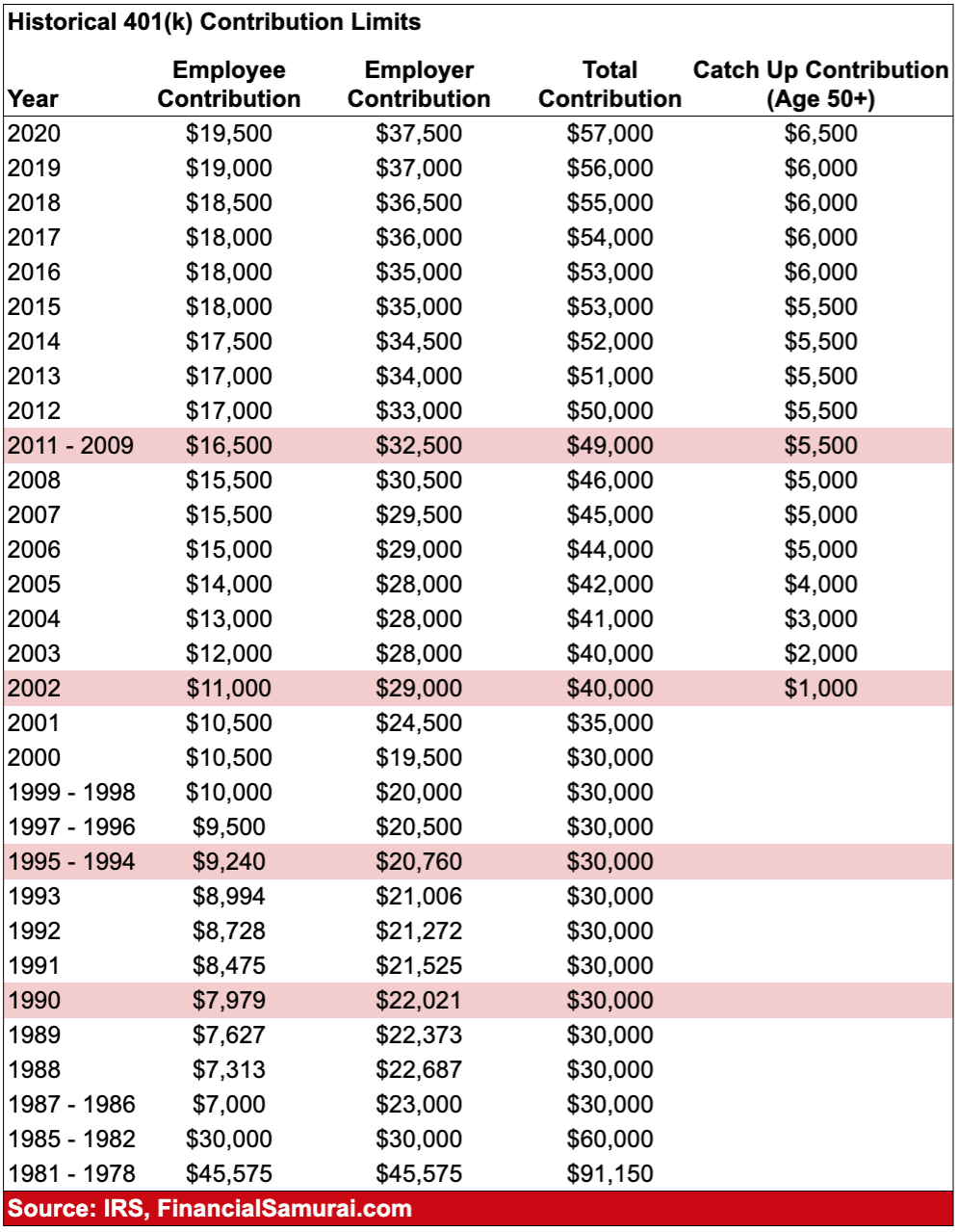

Historical 401(k) Maximum Contribution Limits

Finally, I want to leave you with the historical 401(k) contribution limits. It’s good to see the government has authorized steady increases to keep pace with inflation.

There’s no reason to think the government won’t continue to increase the 401(k) maximum contribution limit by $500 or more every year or two. By the year 2030, the employee 401(k) contribution limit will probably be around $25,000.

If you want to retire comfortably, please max out your 401(k) each year at the very least. After 10 years, you will be astounded at how much you’ve ended up accumulating.

Once you’ve developed an automatic maximum 401(k) contribution habit, focus all your energy on building your preferred passive income investments.

Your 401(k) really should be an afterthought, just like Social Security. If it’s there when you retire, great. If not, you never counted on it in retirement anyway.

As an old man now, I greatly prefer earning dividend income, tax-free municipal bond income, REIT income, and real estate crowdfunding income. My desire to own physical rental property has waned. However, there is one real estate opportunity I’m eyeing that may just be too good to pass up! Stay tuned.

Readers, if you’re not maxing out your 401(k) please share why not. How’s your path to 401(k) millionaire status coming along? Are you on tract to have a seven-figure 401(k) by age 60?

The post The Maximum 401(k) Contribution Limit For 2020 Goes Up By $500 appeared first on Financial Samurai.

from Financial Samurai

via Finance Xpress

0 comments